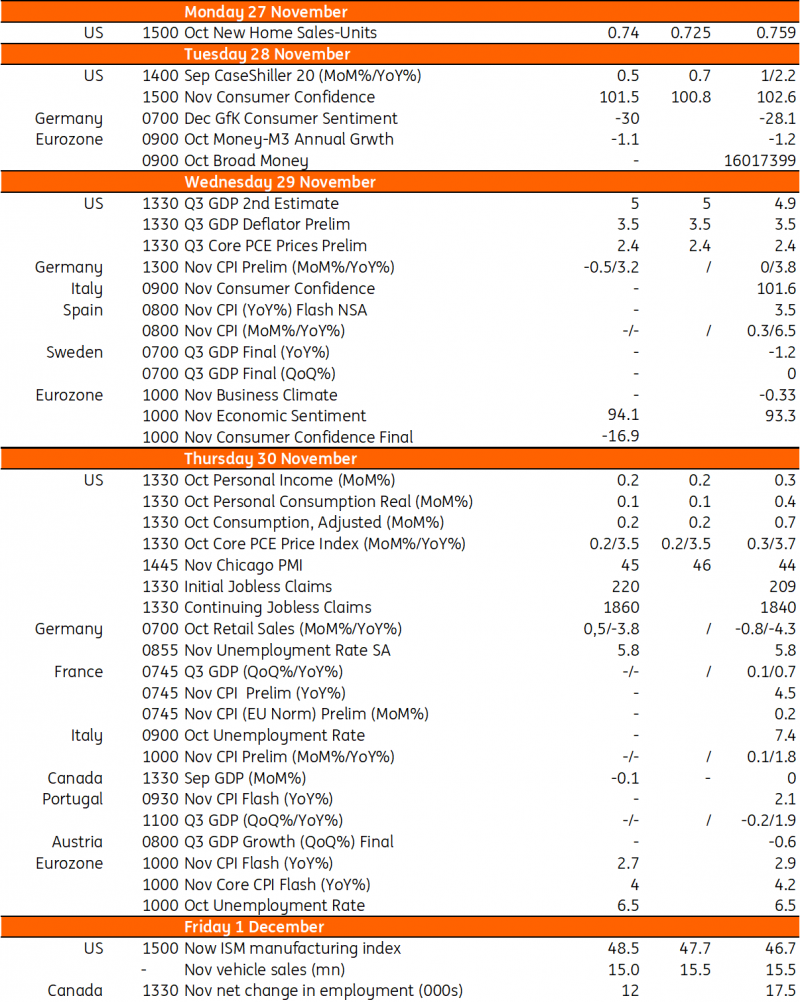

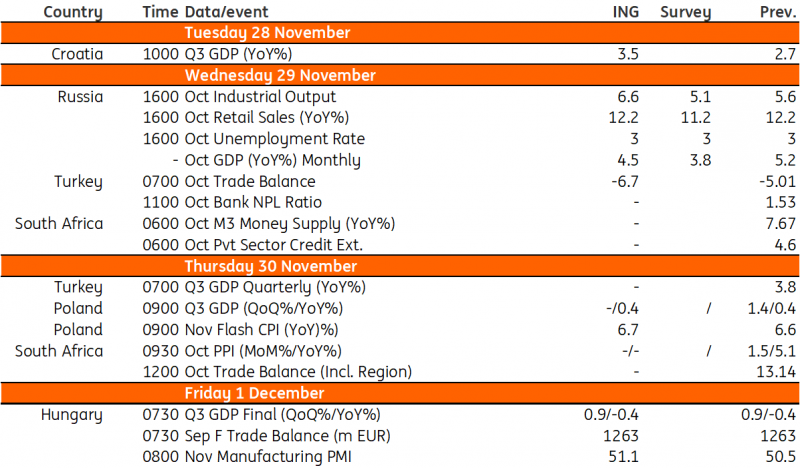

Key events in developed markets and EMEA next week

Next week in the US, we will be closely following the ISM manufacturing index and the Fed's favoured measure of inflation. All eyes will be on CPI releases in the eurozone, where we expect continued improvement and the core rate falling to 4%. Elsewhere, we expect to see positive third-quarter GDP releases in Hungary and Poland.

US: Closely following the ISM manufacturing index for any signs of a rebound

Markets have firmly bought into the view that the Federal Reserve won’t hike interest rates any further and that 2024 will see a series of interest rate cuts from the second quarter onwards. Around 90bp of cuts are currently priced, whereas we're forecasting 150bp for next year on the basis that consumer weakness is likely to be a key theme given subdued real household disposable income growth, fewer savings resources, and less borrowing as interest rates continue rising. This should allow inflation to slow more quickly, giving the Federal Reserve greater scope to loosen monetary policy.

Next week’s data flow includes the Fed’s favoured measure of inflation, which we expect to show a 0.2% month-on-month rate of price increases. This is broadly in line with what the central bank wants to see and, if repeated over time, would bring the annual rate of inflation as measured by the core personal consumer expenditure deflator back to 2%. We also get more housing numbers, which should signal healthy new home sales, but this is due to the lack of availability of existing homes for sale. Prices should continue rising in this environment, but with home builder sentiment having plunged in recent months, cracks are starting to form as the legacy of high borrowing costs bites more and more harshly. We will also be closely following the ISM manufacturing index for any signs of a rebound after having been in contraction territory for the past 12 months.

Eurozone: Core inflation to continue improving to 4%

Next week, we'll see new inflation numbers for the eurozone. Inflation dropped more than expected in September and October, and the question now is whether the low inflation trend will continue. We expect some continued improvement, with core inflation falling to 4% and headline inflation dropping to 2.7%. Still, there are signs of continued inflation pressures that shouldn’t be ignored after a few encouraging data releases. The November PMI showed that businesses still see increased input costs, resulting in more survey respondents indicating that selling price inflation ticked up. Thursday will tell us whether inflation has continued its rapid normalisation.

Poland: We forecast a further decline in core inflation

Flash CPI (Nov): 6.7% YoY

Our forecasts suggest that in November, CPI inflation inched up to 6.7% year-on-year from 6.6% YoY in October, marking the first increase since it peaked in February. We expect a further decline in core inflation, but it will be accompanied by less favourable developments in energy prices as gasoline prices bounced back after two months of declines.

GDP (3Q23): 0.4% YoY

We expect the flash estimate of 0.4% YoY to be confirmed by the final data. We will also learn the composition of third-quarter GDP. According to our forecasts, household consumption declined slightly (-0.2% YoY), while fixed investments continued expanding at a solid rate (7.5% YoY). At the same time, we project a smaller drag from a change in inventories and a lower contribution of net exports than observed in recent months. Monthly data suggests that economic recovery continued at the beginning of the fourth quarter as annual change in industrial output and retail sales turned positive in October.

Hungary: Novembers manufacturing PMI expected to remain in positive territory

The Statistical Office will release the details behind Hungary's strong GDP growth in the third quarter next week. We see positive contributions from industry, construction and agriculture. On the expenditure side, we think net exports were the main driver of the improvement, along with some early positive signs on consumption. November's manufacturing PMI could remain in positive territory, with export capacity still in good shape, reinforcing our view that year-on-year GDP growth could also return to positive territory in the fourth quarter.

Key events in developed markets next week

Source: Refinitiv, ING

Key events in EMEA next week

Source: Refinitiv, ING

Read the original analysis: Key events in developed markets and EMEA next week

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.