Improved PMIs for the Eurozone, strong PMIs for the US showing accelerated activity

Previous week's events (week 20 - 24.05.2024)

US economy

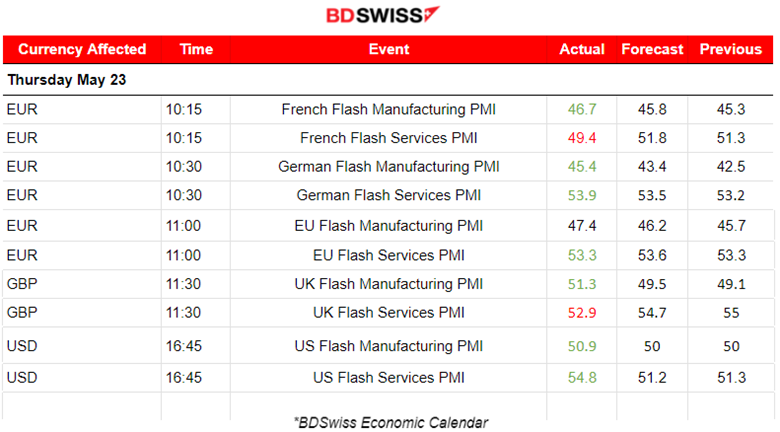

Flash Purchasing Managers Index (PMI) figures in the eurozone, the UK and the United States were reported and shook the markets as the figures showed improvements, stronger than expected. An improved performance this month with activity picking up in the United States. U.S. business activity accelerated to the highest level in just over two years in May, suggesting that economic growth picked up halfway through the second quarter.

Inflation

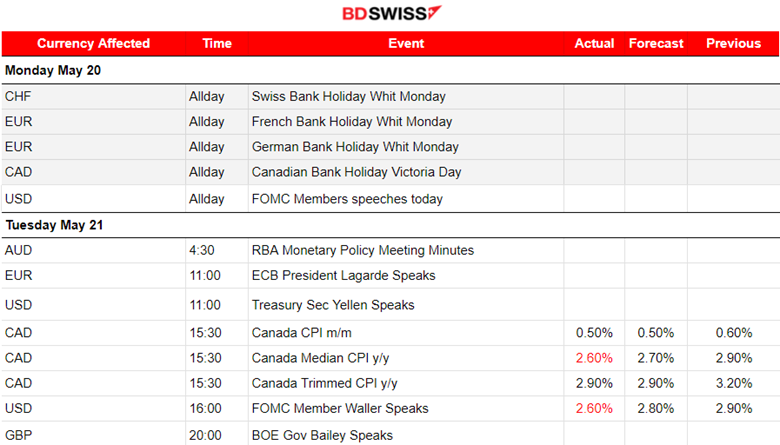

Canada CPI

Canada’s annual inflation rate slowed to a three-year low of 2.7% in April and core measures continued to ease. Month on month, the consumer price index rose 0.5% in April, also less than a forecast of a 0.6% gain.

The cooling was moderated by gasoline prices; excluding them, annual inflation slowed to 2.5% from 2.8% in March.

Another low inflation report adds to the probability of cuts happening soon.

UK CPI

U.K. Inflation eased less than expected and a key core measure of prices barely dropped, boosting expectations for a rate cut soon. The consumer price index (CPI) rose by 2.3% in the 12 months to April, down sharply from March’s 3.2% increase and its lowest since July 2021.

Service inflation was much higher than expected, and petrol prices rose. It inched down to 5.9% from 6.0% in March. Core inflation, which includes goods but not energy, food and tobacco, also reflected persistent price pressures, with the annual rate falling only to 3.9% from 4.2% in March.

Still, expectations for a rate cut from the BoE in June remain high.

Interest rates

The RBNZ decided to keep the Official Cash Rate at 5.50%. Its restrictive monetary policy has reduced capacity pressures in the New Zealand economy and lowered consumer price inflation. Annual consumer price inflation is expected to return to within the Committee’s 1 to 3% target range by the end of 2024.

New Zealand’s labour market pressures have cooled. Wage growth and domestic spending are easing to levels more consistent with the inflation target.

Currency Markets Impact – Past Releases (Week 20 - 24.05.2024)

Server Time/Timezone EEST (UTC+02:00)

Currency markets impact

-

Minutes of the May 2024 Reserve Bank of Australia (RBA) meeting were released at 4:30. The Board agreed it was difficult to either rule in or rule out future changes in the cash rate. The market reacted with an AUD depreciation at that time. AUDUSD dropped near 25 pips before retracing to the intraday MA.

-

The CPI data for Canada on the 21st of May showed that inflation lowered significantly causing CAD depreciation and a jump of the USDCAD pair to around 60 pips. Retracement took place returning to the 30-period MA. The monthly figure was reported as 0.5% while the annual inflation rate cooled to 2.7% in April, likely giving the BoC ‘all clear’ for the June rate cut.

-

The RBNZ decided to keep interest rates steady. Annual consumer price inflation is expected to return to within the Committee’s 1 to 3 percent target range by the end of 2024. NZD was appreciated heavily at that time. NZDUSD jumped near 50 pips and retracement followed.

-

The Consumer Price Index (CPI) in the U.K. was reported lower on the 22nd of May but the figure was higher than expected. The U.K. which had the highest inflation peak of over 11% has managed to beat the U.S. (currently at 3.4%) by lowering it to 2.3% very close to the target level. The market reacted with GBP appreciation and the GBPUSD jumped 35 pips before retracing to the intraday MA.

-

While the FOMC’s latest Meeting Minutes didn’t rule out a September rate cut directly, investors are growing nervous. Uncertainty is in the air while inflation is still high in the U.S. while in the other economic regions, it has been cooling as expected.

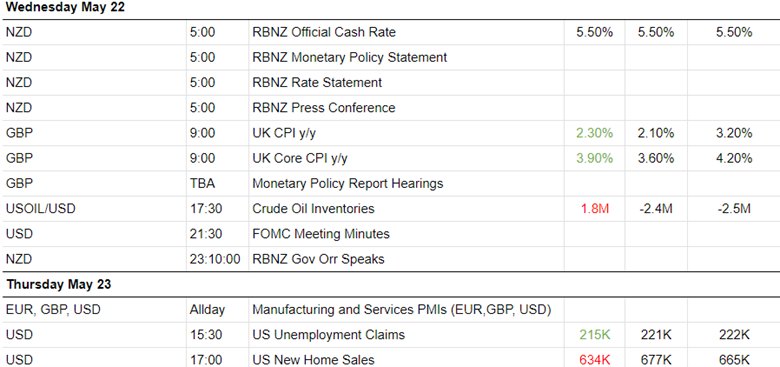

The PMI releases were as follows:

Eurozone PMIs:

In France, the PMI services sector PMI turned to contraction in May after returning to growth at the start of the second quarter.

Germany saw a boost in business activity for the second month and at a faster rate in May. Stronger growth in the service sector with stabilising manufacturing output. Stronger demand and greater optimism towards the outlook. Price pressures meanwhile eased across the eurozone’s largest economy mid-way through the second quarter. Services PMI was reported high at 53.9 points, the highest since June 2023.

In the Eurozone economic recovery gained momentum in May. a. Faster increases in business activity, new orders and employment were all recorded midway through the second quarter. Tates of inflation of both input costs and output prices softened from April but remained above pre-pandemic averages in each case.

UK PMIs:

The U.K. PMIs remain in expansion with the services PMI to be reported way worse than expected though. Overall the U.K. registered a solid expansion in May. A resurgence in manufacturing production supplemented a further, albeit slower, upturn in services output.

US PMIs

U.S. business activity growth accelerated sharply to its fastest for just over two years in May—obviously an improved economic performance midway through the second quarter. The service sector led the upturn, reporting the largest output rise for a year, but manufacturing also showed stronger growth.

- The Unemployment claims figure on the 23rd of May was reported lower at 215K showing that the labour market can potentially get hotter again. Unemployment Claims are down and PMIs are up. Remember that the market responded quite significantly with USD strengthening yesterday at the time of the U.S. PMI data release at 16:45. Latest data are showing improved figures for business in the U.S. so let’s see what the next week brings to the table as the Fed is betting on cooling inflation upon next release.

Forex markets monitor

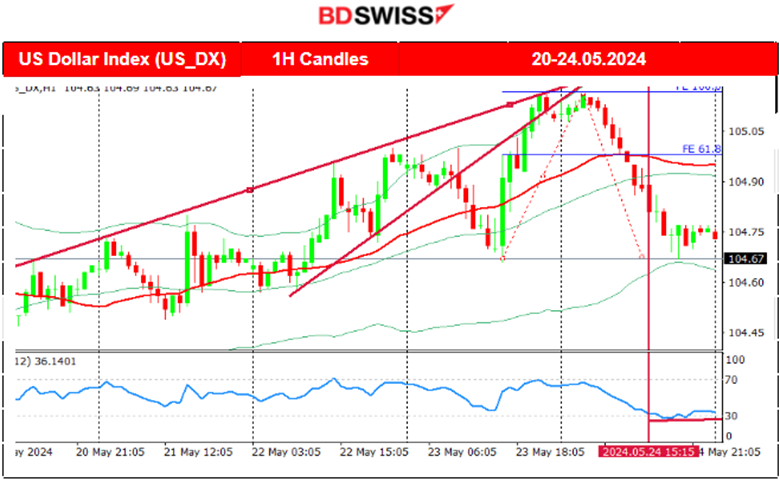

Dollar Index (US_DX)

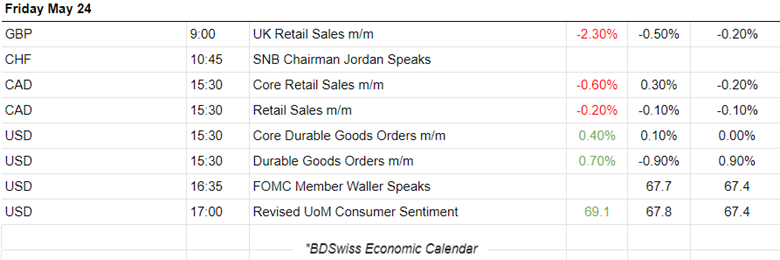

The U.S. dollar last week climbed overall to high levels and it is quite clear that volatility was really high with several reversals taking place. On the 23rd there was a jump to the upside with 105.16 serving as a strong resistance before a reversal to the downside took place. This U.S. dollar recent appreciation could be a result of expectations towards future appreciation of the currency due to the fact that major central banks are experiencing lower inflation very close to the target level (2%) while the Fed is not. The U.S. does not experience significant inflation cooling, with inflation remaining over 3%, while the labour market data are currently indicating hot signals again. Non-Fed central banks could start interest rate cuts sooner than the Fed. An anticipated high interest rate differential due to different interest rate policies could explain the recent dollar strengthening. The weakening though on the 24th of May is surprisingly high.

EUR/USD

This pair moved to the downside overall and the path is obviously driven by the USD. The EUR is not really affected by the news. The recent data regarding the Eurozone show a turn to improved business conditions, especially in Germany. This keeps the EUR from depreciating significantly. Inflation in the eurozone is lowering as well keeping expectations of cutting interest rates next month steady. The U.S. dollar saw high PMI figures, a rise in durable goods orders and lower unemployment claims, all pointing to U.S> dollar appreciation thus explaining the downward path of EURUSD.

USD/JPY

The pair moved steadily to the upside on an upward trend since the 21st of May. On the 24th of May, it found resistance and started a retracement. The USD obviously was the main reason for the overall upward path, but the JPY occasionally experiences high depreciation as well. For example on the 24th, the USDJPY remained high while USD was depreciating against a basket of currencies. The JPY depreciated significantly not only that day but very frequently with most pairs (with JPY as Quote currency) moving upwards (GBPJPY, EURJPY etc.).

Crypto markets monitor

BTC/USD

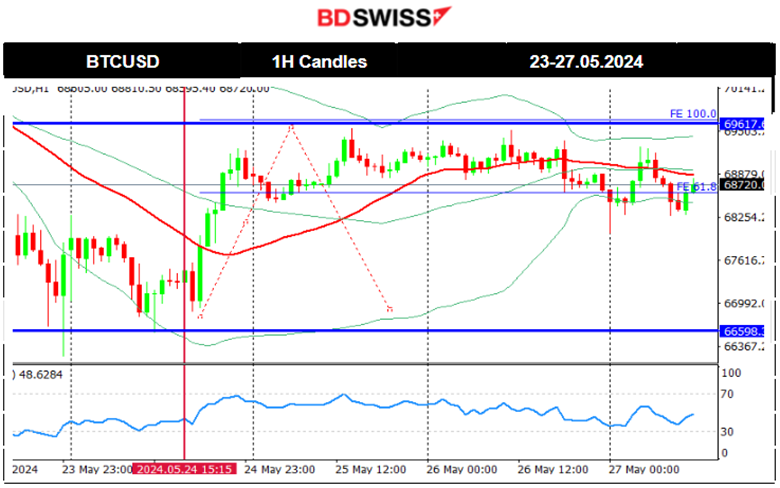

Bitcoin settled near 70K USD on the 22nd of May. That changed later with Bitcoin moving rapidly to the downside on the 23rd after 16:00. Many assets including stocks and commodities got affected negatively after that time. The price returned back and settled near the 67K USD level wiping out the gains since the jump on the 20th of May.

The price eventually jumped on the 24th of May and continued its upward movement until the resistance at near 69,600 USD. It retraced during the weekend when volatility levels lowered.

This week's events (week 27 - 31.05.2024)

Coming up:

Preliminary U.S. GDP figure release for the quarter.

Inflation-related figure releases:

-

CPI Flash estimates for the Eurozone

-

CPI for Australia.

-

CPI for Tokyo.

-

U.S. Core PCE Price index figure release.

Currency markets impact

-

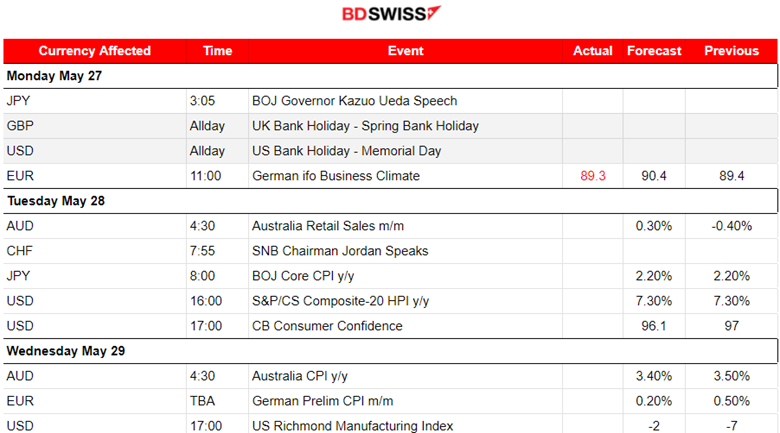

On the 28th of May, the Retail sales for Australia will be released and their report is expected to show growth. It is true that inflation is not decreasing further in that region as we see mixed data for the labour market with unemployment rising and positive employment change. AUD pairs could be affected by a moderate intraday shock.

-

The Core CPI will be released at 8:00. The BOJ usually pays more attention to the Core data. The figure is expected to remain stable, however any surprises will probably cause the JPY pairs to experience big moves.

-

The Consumer confidence report could cause higher volatility than usual upon release affecting the USD pairs. Financial confidence is a leading indicator of consumer spending, which accounts for a majority of overall economic activity. The figure has been dropping recently. U.S. consumer confidence deteriorated in April, falling to its lowest level in more than 1-1/2 years amid worries about the labour market and income. Elevated price levels, especially for food and gas, dominated consumer concerns.

-

On the 29th of May, the annual CPI change figure for Australia will be released at 4:30 causing probably a moderate shock for AUD pairs. During the Asian session. Inflation is expected to be reported lower but the previous figure indicated that it is not slowing while other indicators do not justify a strong decrease.

-

On the 30th of May, the quarterly Swiss GDP figure will be released potentially affecting the CHF pairs.

-

On the same day, the quarterly U.S. GDP preliminary figure will be released at 15:30, shedding some light in regards to if the economy slowed in the second quarter. This is what is expected with a figure of 1.3% versus the previous 1.60%. USD pairs could be affected by a moderate intraday shock at that time. Unemployment claims will be reported at that time as well and they are expected to show slight growth. However, the impact will probably not be so great.

-

On the 31st of May Tokyo's inflation figure will be released causing a moderate shock for JPY pairs at 2:30. Inflation is expected to be reported higher. The 10-year Japanese government bond yield rose above 1% last week for the first time since 2012, but the US dollar traded above JPY157 for the first time since the BOJ is believed to have intervened earlier this month.

-

Manufacturing and Non-manufacturing PMIs will be released at 4:30, expected not to change dramatically. The AUD and CNH pairs could see a moderate intraday shock at that time. China's PMI and industrial profit reports Industrial data will be the focus.

After several consecutive months of stronger-than-expected industrial production, a further decline in profits could be a sign of price competition

-

CPI data for the Eurozone will be released at 12:00. Inflation in the Eurozone cooled significantly and is very close to the target level. Expectations show that the figures will not change but remain steady. EUR pairs could see some higher volatility than normal in case of a surprise increase.

-

At 15:30 the U.S. PCE price Index figure will be released and it might cause an intraday shock for the USD pairs if the figure is reported higher than expected. The monthly CPI figure was last reported lower and the annual figure lowered as well by 1%. So expecting a lower PCE price index figure makes sense.

Commodities markets monitor

US Crude Oil

On the 21st of May, the price stayed below the 30-period MA and moved even lower today forming lower lows. The bullish divergence was valid as mentioned in our previous analysis. The price eventually jumped on the 23rd of May crossing the 30-period MA on its way up and indicating the possible end of the downtrend. However, that changed when the price experienced a sudden drop after the U.S. PMI release. The momentum was so strong that a new downtrend was created. The price broke an important support near 76.40 USD/b and sparked expectations for a further downward movement to the next support. On the 24th that support was at nearly 76 USD/b. After that, the price reversed to the upside, crossing the MA on its way up and reaching the resistance at near 77.90 USD/b. Retracement has not taken place yet but it could be the case even though the RSI does not show strong bearish signals yet (bearish divergence).

Gold (XAU/USD)

The support on the 22nd of May was broken and the price dropped heavily reaching the support at near 2,355 USD/oz. The downtrend continued until the price reached another important support at near 2,325 USD/oz on the 23rd of May and the potential for a retracement now is apparent with the target level at near 2,360 USD/oz. On the 24th of May, the price has moved only slightly upwards but the potential for a further upward movement still remains.

Equity markets monitor

SP 500 (SPX 500)

Price Movement

The triangle formation that was highlighted in our previous analysis was broken on the 22nd of May and the index moved downwards to the support near 5,290 USD before a full reversal took place. This high volatility depicted on the chart was taking place during the FOMC meeting minutes release. All U.S. indices experienced a pre-market aggressive movement to the upside and broke the resistance at near 5,330 USD reaching only near the peak at near 5,350 USD. Then, after the stock market opening and the release of the U.S. PMI figures all indices dropped heavily on the 23rd of May. S&P500 reached support at near 5,258 USD before a strong retracement took place with an upward steady movement on the 24th of May. The index reached the 5,314 USD resistance that day before it retraced to the 61.8 Fibo level.

Author

BDSwiss Research Team

BDSwiss

BDSwiss is a leading financial institution, offering bespoke CFD trading and investment products to more than 1.7 million registered clients, in over 180 countries.