How the ECB’s new operational framework could impact bank liquidity and funding

The European Central Bank is set to release its new operational framework, including the level of Minimum Reserve Requirements (MRR). We would see an unchanged MRR as a positive for eurozone banks, while an increase would come with negative impacts on bank profitability and liquidity.

The level of MRR in focus in the review

ECB President Christine Lagarde confirmed in a press conference last week that the central bank aims to reach a consensus to complete the review of the operational framework on 13 March and publish it thereafter. She also confirmed that the Minimum Reserve Requirements (MRR) would form part of the review and the announcement.

ECB speakers have discussed the level of the MRR on several occasions. Expectations for any changes to this, however, were downplayed yesterday. According to Bloomberg, which cited people with knowledge of the matter, ECB officials are leaning against any immediate change to the MRR. A push by some members to increase the requirement from the current 1% level has struggled to gain momentum, according to the article. That being said, the article notes that no decision has yet been taken, and even if the level is confirmed this week, officials haven’t excluded the prospect that it could be raised in the future.

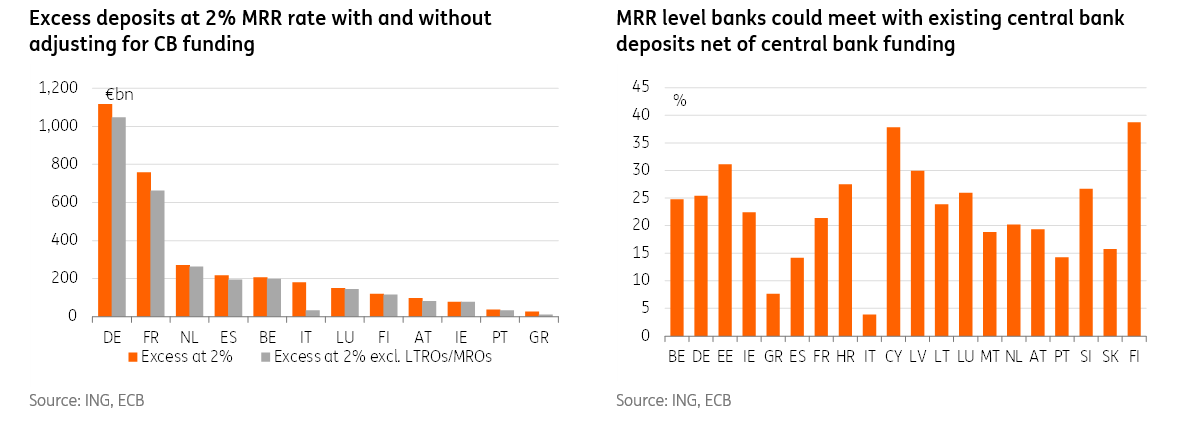

Banks have now enough central bank deposits for an MRR hike

Eurozone banks must set aside c.€161bn as minimum required reserves to meet the 1% requirement as of March 2024. An increase to 2% would double the level unless it came with action by banks to drive down their individual absolute requirements. An increase would have been negative for bank profitability as the ECB doesn’t pay interest on funds posted for the MRR.

Looking purely at current and deposit accounts, eurozone banks are well positioned for a potential (modest) increase. In all countries, banks could absorb an increase to 2%, and this is also the case if adjusting for the outstanding ECB funding programmes. In all eurozone countries, Italian banks would have the least room for a higher MRR, in our view. Even in Italy though, with the current net central bank liquidity, the sector could absorb an increase even to 3%, based on our calculations.

Existing central banks deposit vs potential MRR hike

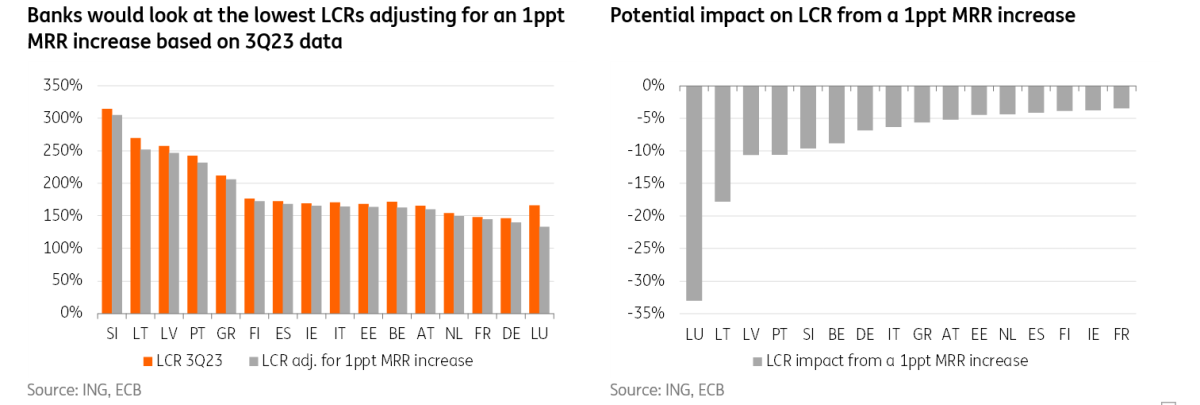

But an MRR hike would have a substantial negative impact on LCR liquidity buffers

Funds posted to meet the MRR can’t be used to fill LCR requirements, meaning that an increase will have a clearly negative impact on bank Liquidity Coverage Ratios (LCR).

The latest available LCR metrics at the eurozone level are for 3Q23. Adjusting the LCR for the increase in MRR would result in an LCR decline of some 9ppt on average. The LCR ratios would remain well ahead of the 100% requirement. Among larger countries, German and French banks would see their LCR ratios at the lowest end of the pack, while Southern European banks would retain higher average LCRs.

Impact on LCR buffers from higher MRR

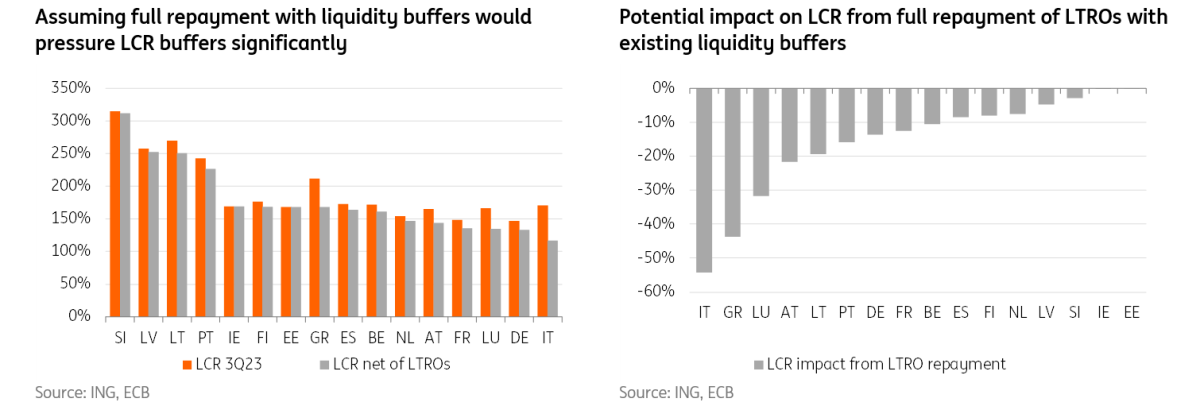

LTRO repayments continue to drive down LCRs

The 3Q23 LCR ratios look inflated due to the ECB’s TLTRO-III programme. Going forward, we expect the ratios to continue to edge lower as banks repay their TLTROs.

If we adjust the 3Q23 LCR liquidity buffers with the LTROs that were outstanding at the time, assuming a full repayment with existing liquidity buffers, the LCRs would be, on average, some 16% lower than the reported levels, with the largest impact on Italy and Greece. Italian banks would see their LCR ratio edge lower towards 116%, with Germany and France also positioned at the lower end of the spectrum here.

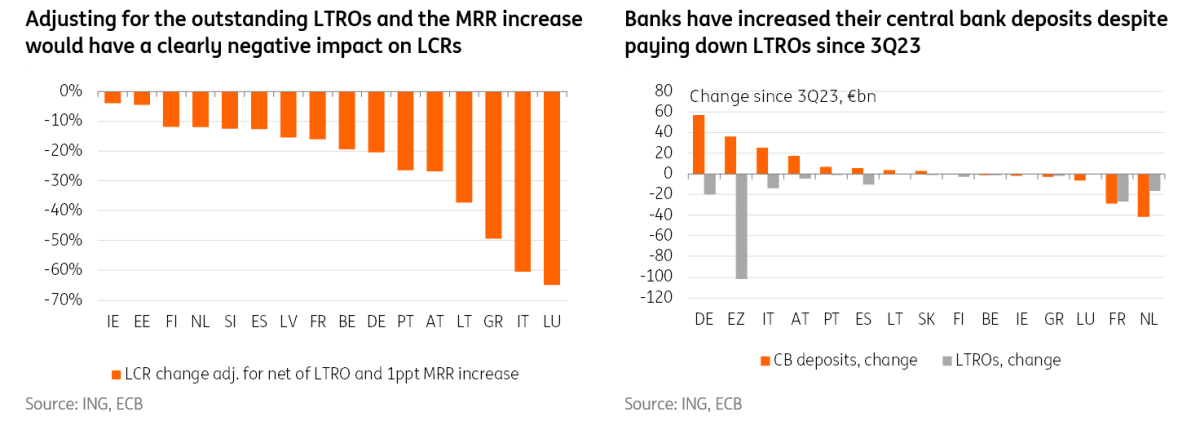

If we adjust the LCR liquidity buffers for both the maturing LTROs and a higher MRR rate, the LCRs would be on average some 25ppts lower than the actual reported ratios. The difference would again be the largest for those countries with larger TLTRO balances outstanding such as for Italy or Greece. While the country-level LCRs would remain above 100%, the headrooms would be undoubtedly much more limited.

Full LTRO repayment would drive down liquidity buffers

Banks have protected their liquidity buffers while repaying the ECB

The reality would likely be somewhat less negative than this as banks have taken action to refinance part of the TLTRO redemptions outside the central bank.

Since 3Q23, eurozone banks have paid back a combined €102bn in longer-term central bank funding as the TLTROs have continued to mature. During this time, French banks have paid down the largest share at €27bn, followed by Germany (€20bn), the Netherlands (€17bn), Italy (€14bn) and Spain (€10bn).

At the same time, banks have increased their central bank deposits by €36bn. In particular in Germany, Austria and Italy, the net change in liquidity has been positive, while in the Netherlands and France, the net change has been negative.

In the past months, banks have increased central bank deposits despite the LTRO runoff

Another €216bn in TLTROs mature in March and €177bn later this year

The negative impact on liquidity buffers from the LTRO redemptions is set to continue. The TLTRO-III tranche 7 which matures on 27 March 2024 is currently the largest outstanding TLTRO tranche with €215.5bn in outstanding balances. In addition, a 3m tranche with €1.1bn balances redeems on this date. The next TLTRO-III early repayment opportunity is also offered in connection with these maturities.

For early repayments on 27 March in tranches 8-10, banks will have to notify the national central bank by 13 March at 17.00 CEST. We would not expect large early repayments, particularly in the longer tranches in March. Instead, we would expect the early repayments to be concentrated in the shortest tranche 8 that redeems in June. The early repayment amounts will be published on 15 March.

Banks have prepared for the approaching €216.5bn LTRO redemptions (TLTROIII.7 and the 3m LTRO) via active issuance in the bond markets. After the March redemption, (prior to any potential early repayments) the size of the TLTRO-III programme drops to €177bn, split between June (€53bn), September (€85bn) and December (€39bn).

Italian banks have €141bn in outstanding TLTROs which are set to mature in 2024, the highest across countries, followed by France at €96bn and Germany at €69bn.

Repayment of LTROs may impact liquidity buffer composition

The LTRO runoff and potential MRR changes may impact the level of liquidity buffers but also potentially the composition of these buffers.

Repayment of LTROs with existing buffers would have a direct negative impact on LCR cash balances, while the holdings of high-quality bonds remain unchanged. A potential increase in MRR would also impact negatively the LCR cash buffer, while other liquidity buffers would remain intact. These factors could have implications for bond holdings in liquidity buffers.

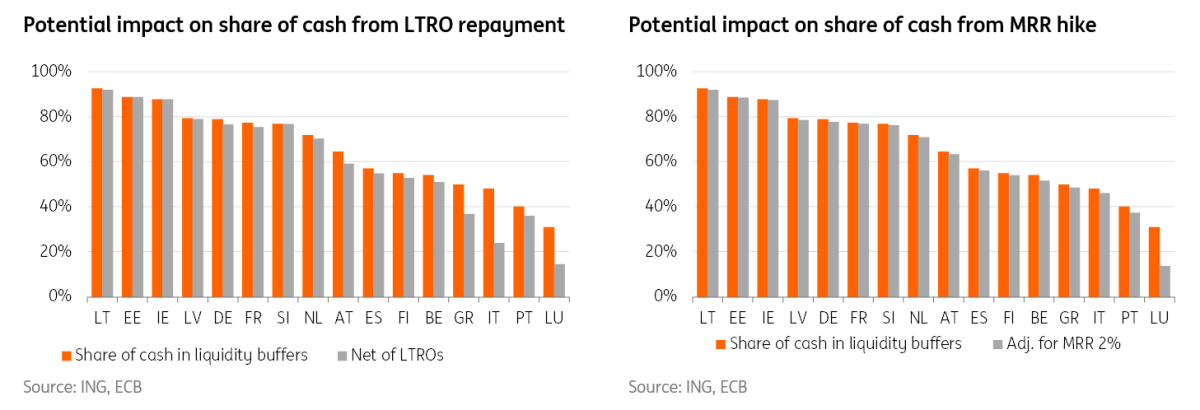

The LCR stats published by the ECB don’t include the split of cash vs govies. To get at least some sort of broad picture on the potential split we adjust the cash and central bank deposits on significant institutions' balance sheets with the MRR and compare the number with the total LCR buffers. While you should treat these numbers with some caution, they may give some idea of the direction. On average banks rely to a large extent on cash in their liquidity buffers with the share at 66%. That being said, country differences are large with banks in Southern Europe relying perhaps less on cash than their more Northern counterparts.

If we adjust the assumed cash positions with a full repayment of outstanding LTROs, the share of cash in LCR buffers substantially declines towards an average of 61%, with the largest impacts obviously for banks with larger outstanding LTROs (as of 3Q23 to align with LCR numbers) such as in Italy and Greece. We also adjust the numbers for a potential increase in the MRR to 2%. The share of cash would be some 2ppts lower on average, with Portugal, Belgium, Italy and Greece among the countries with a tad larger impact.

As banks may have internal targets to maintain a certain share of cash versus other liquidity buffers, a substantially lower share could result in banks taking measures to adjust the ratios higher again. This could be reflected, for example, in pressure to refinance maturing LTROs or convert other liquidity buffers such as government bonds into cash.

The share of cash in liquidity buffers could edge lower

Check also for the future plans regarding the funding operations

Indications on the refinancing operations are also worth a careful look. Earlier press reports suggested that the ECB aimed to revive the interbank market with its new monetary policy framework. The design was meant to allow the ECB to run with a smaller balance sheet size and still deliver stable funding conditions for banks, relying on a structural bond portfolio and bank loans to provide sufficient liquidity.

Banks are meant to be able to participate in refinancing operations, with durations anticipated to be similar to offerings in the past, according to a Bloomberg article published in late February. In addition, maintaining the current policy of satisfying all bids at a fixed rate was said not to have faced any major objections.

In the past years, banks have been offered liquidity via the MROs and LTROs with the durations ranging between seven days to up to three months for the standard operations and up to three years via the targeted longer-term refinancing operations.

Banks have relied very heavily on the ECB in recent years for funding, but this has been driven almost solely by the attractive conditions of the longer-term funding programme TLTRO-III. The programme provided some €2.3tn of funding to banks at its peak, with the volumes dropping to €392bn as of end-2023 with the programme set to mature by the end of this year.

Instead, bank drawings from the three-month tranches have been much smaller in size, currently around a combined c.€5bn. The even shorter seven-day funding via the MRO has also been used to a limited extent with the current drawings at around €4.5bn, coming down from above €14bn at the end of the year.

Based on the press reports, it sounds likely that there will be limited changes to the funding programmes in the shorter term. That being said, while news reports have suggested that the ECB could offer similar durations to the past, it could well be that, if the central bank is targeting a smaller balance sheet size, conditions for any new longer maturity funding could be less attractive than those seen previously.

An unchanged MRR should be seen as a positive for the sector

We consider that if the ECB keeps the MRR level unchanged, as was indicated yesterday, it should be seen as a positive for eurozone banks.

An increase would have been negative for bank profitability as the ECB doesn’t pay interest on funds posted for the MRR. Keeping the MRR unchanged should also allow banks to better absorb the other negative impacts on liquidity that are in the pipeline for this year. Liquidity buffers are being hit by a combination of TLTRO repayments, deposit volatility driven by higher rates and by the government measures targeting retail deposits among others.

It is good to note that the formulation in the article published yesterday regarding the MRR level leaves some room for the ECB to revisit the level at a later stage, resulting in a somewhat negative overhang on banks regarding the matter.

Alongside the MRR, we consider that maintaining similar funding programmes could be seen as neutral or perhaps even mildly positive for the sector. Any push from the ECB for banks to move more towards financial markets from central bank funding would benefit stronger banks at the expense of weaker rated names in our view, pushing up rates on other bank funding products.

Read the original analysis: How the ECB’s new operational framework could impact bank liquidity and funding

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.