Hike and tightening bias maintained; September hike due!

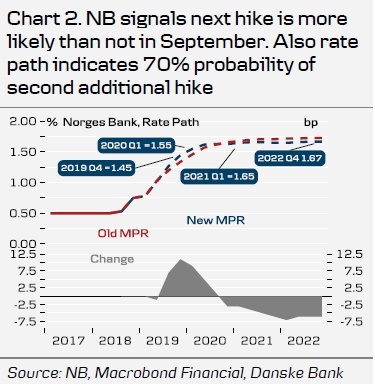

As widely expected, Norges Bank (NB) this morning raised policy rates by 25bp taking the sight deposit rate from 1.00% to 1.25%. The rate path was marginally adjusted upwards at the short end and marginally downwards at the long-end (chart 2). The message is clearly hawkish as a strong domestic business cycle suggests a further frontloading of monetary tightening despite elevated international uncertainty at present.

The executive board concluded that the ‘...current assessment of the outlook and balance of risks suggests that the policy rate will most likely be increased further in the course of 2019'. The rate path implies a 70-80% probability of that hike coming in September. While NB has previously cautioned against over-interpreting the implied probabilities the press conference did confirm that the board wanted to signal September as the most likely time for the next rate hike. The long-end of the rate path was lowered marginally to 1.67% (from 1.73%). This falls within NB's estimate of the neutral sight deposit rate of [1.60%-2.60%]. Overall the rate path therefore suggests another hike in 2019 and a roughly 70% probability of a second additional hike – most likely in 2020.

According to NB's assessment underlying inflation is a little higher than the target. Capacity utilisation is somewhat above normal levels and has been underestimated by NB. The upturn in the Norwegian economy is somewhat stronger than earlier projected despite elevated global uncertainty which Olsen emphasised as the largest risk factor for NB. Generally the economic projections had few surprises (see appendix). We share NB's view on the Norwegian economy going forward. We now expect NB to hike the sight deposit rate again by another 25bp at the 19 September board meeting. We acknowledge the drop in foreign rates since Friday (the deadline of the MPR) but still think September is more likely than December. For 2020 our base case remains another 2 hikes.

FI/Rates. We have argued for buying short-end FRAs outright. In light of today's sight deposit rate hike and the new rate path we reiterate these strategies. There should still be upside potential in NOK FRA 3M SEP19 and DEC 19 – despite today's jump in DEC 19 of 8bp. The current inverted FRA curve from the start of 2020 going forward is in stark contrast to the NB's rate projection. In the current international environment it may be premature to add steepening strategies in the red and green NOK FRAs. The hawkish NB relative to international peers and the downward pressure in international interest rates may trigger a renewed interest for long-end NGBs. We therefore reiterate our strategy for a flattening of the Norwegian yield curves.

FX. EUR/NOK moved sharply lower upon announcement triggering profit taking in the 9.67-9.69 range. Strategically, we still like to be long NOK. In FX Strategy – Why is the NOK so weak?, we argued that some of several explanations for the NOK decoupling from the relative rate over the last year has been A) the global environment and B) pivotal carry in the sense that the NOK has been ‘carry-dominated' by Triple-A commodity alternatives in CAD, AUD and NZD. With yesterday's FOMC message A) is set to become much more supportive for the NOK going forward. In addition with the NB's message the NOK carry will now catch-up up making the NOK increasingly attractive to buy relative to B). We expect a stronger NOK in the coming months and remain short USD/NOK and AUD/NOK.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.