Greenflation: How inflationary is the energy transition?

Greenflation most often refers to inflation linked to public and private policies implemented as part of the green transition.

Adapting production methods to low-carbon technologies, which emit fewer greenhouse gases, will require, on the one hand, massive and costly investments which will increase the marginal cost of each unit produced in the short term and, on the other hand, the use of rarer and therefore more expensive materials. This will create upward pressure on prices.

The ecological transition will also require putting the “price signal” into play: increase the price of fossil fuels through taxation (carbon tax) and emission allowance markets (explicit price) as well as regulations (implicit price).

The energy transition can also have indirect macroeconomic effects on inflation, both upward and downward. It would seem that in the short term, these effects are mainly inflationary, while in the medium to long term, disinflationary pressures stemming from the positive effects of the transition on supply and productivity gains could become more important.

The sooner decarbonisation is initiated, in a clear, gradual and supported manner, the more moderate its disruptive and inflationary effects are likely to be, and the sooner its positive effects become apparent.

Green production will initially cost more

The green transition will largely involve a change in production methods. These latter are indeed largely responsible for the high greenhouse gas (GHG) emissions. In order to produce “green”, this capital will need to be replaced by less GHG-emitting structures, equipment, materials and techniques. These major changes are likely to be inflationary, although opposite effects cannot be ruled out. We distinguish between several channels.

First, some of the minerals needed to develop a “net zero” industry are available in limited quantities and some are difficult to extract even though they are in high demand. According to the International Energy Agency, total demand for minerals to produce low-carbon technologies is expected to increase fourfold by 20401 assuming that the objectives of the Paris Agreements are met. Regarding lithium, for example, for which demand is expected to quadruple between 2025 and 20352, scientists are still divided as to whether the reserves available will be sufficient to meet the growing demand for electric batteries.

A first major difficulty comes from the high concentration of ore supply in the hands of a very small number of producers. 91% of lithium was produced by only three countries in 20223 (Australia, Chile and China), and more than 52% of cobalt production came from the Democratic Republic of Congo4 in 2020. The European exposure to Russian gas shows well to what extent the dependence on a single partner makes importing countries highly exposed to changes in commodity prices.

In addition, a new mine can run for twenty years, adding an additional supply constraint. Finally, environmental barriers (attention to biodiversity damage) also weigh on the supply of these minerals.

This concentration of supply, as well as the constraints on mining techniques, make supply very inelastic. The combination of low supply and strong demand creates an inflationary configuration on these markets. Lithium prices have increased sixfold since 2009. Prior to the pandemic and the energy crisis following the outbreak of Russia’s war in Ukraine, this same lithium price had increased by 43% since 2009. The evolution of copper prices is also symptomatic of the tensions that can arise on a metal that is critical to the energy transition6 (see Chart 1), in addition to the strong correlation between the price of such metals and world economic activity7. However, the inflationary effect of price surge on this type of material must be put into perspective. This can only be a relative prices distortion, without a broad-based rise in prices. Such a movement depends on the extent of the rise in the price of goods needed for low-carbon technologies and its diffusion to the other goods and services prices.

Secondly, companies and public authorities must direct their research towards new processes in order to decarbonise their industries. However, these new technologies require huge investment (notably in research and development), especially during the transition period. These investments in the energy transition are expected to represent 2% of global GDP on average per year until 20508 in order to complete this transition

In the short term, the more expensive investments will increase the fixed production costs which will be passed on to prices and therefore have inflationary effects. On the other hand, part of the capital currently used will be declared obsolete before the end of its life cycle (“stranded assets”). This is akin to capital destruction and constitutes, all other things being equal, a negative supply shock, which is potentially inflationary. The aggregate productivity gains that are awaited from green innovations should, however, subsequently have a disinflationary effect.

The inflationary effects of a carbon tax

The ecological transition also requires putting the “price signal” into play: to raise the prices of polluting products to reduce their use. The action on prices can be direct (through a tax) and indirect (through regulation); the terminology explicit-implicit is also used. The term “explicit” price refers to the actual price paid by the person who buys the good. Increasing the explicit price on a discretionary basis involves carbon taxation and emission allowance markets (see Box 2). The “implicit” price refers to the hidden costs of acquiring a good that is not reflected in the price paid at the time of exchange. Increasing the implicit cost can be achieved by regulating the production, trade and consumption of the good. For example, by facilitating administrative procedures for the installation of solar panels by private individuals, or conversely by making it more difficult to extract fossil fuels, a State would increase the implicit price of electricity produced from them. This increase in the prices of carbon products, such as oil or coal, is a necessary part of an energy transition policy, in order to reduce demand for these products, provided that alternatives are developed in parallel.

Among the most advanced options for increasing the price of fossil fuels, carbon tax is one of the easiest to apply technically. It operates by charging a tax per tonne of CO2 emitted to the originator. This increases the marginal cost of producing any carbon goods. This increase in costs is then for a large part passed on the selling price of finished products and reflected in the increase in these components of the consumer price index. The carbon tax principle and its implementation are therefore likely to create inflation whenever the rate of this tax increases

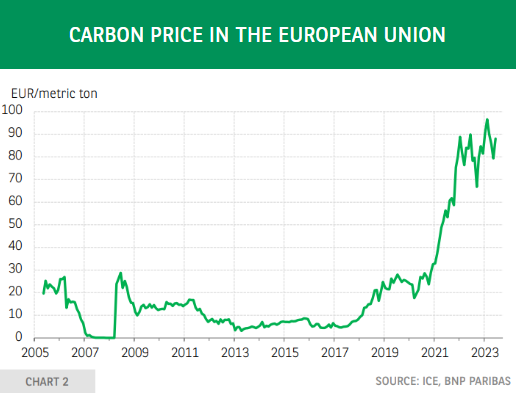

Many European countries (France, Denmark, Germany, etc.) have already introduced a carbon tax. The price per tonne of CO2 is now more than ten times higher than when the Paris Agreements were signed in December 2015, according to the ICE. While recent events affecting the energy market contributed to this increase, pollution was already 2.8 times more expensive in February 2020 than in December 20159. In France, since 2018, the carbon tax has been EUR 44.6/tonne of CO2 emitted, for a European market price of EUR 88.1/tonne of CO2 in June 2023 (see Chart 2).

What do research and business models say about the impact of a broad-based carbon tax on medium and long-term inflation?

According to Banque de France10, the inflationary impact of the carbon tax depends on its gradual and early implementation. The earlier and more gradual the implementation, the less inflationary the carbon tax would be, and vice versa. The study shows that in a scenario where the carbon tax is used to finance the public investment needed for the transition, the impact on inflation would be positive within five years (around +0.2 pp). This impact would be even greater (around +0.5 pp) in a scenario where implementation is abrupt and an isolated measure, without any accompanying public investment policy in favour of the transition. This result shows the importance of supporting the households most affected by the carbon tax.

Over a longer period, disinflation?

Without considering potential productivity gains linked to green investments, the Pisani/Mahfouz report from France Stratégie11 estimates that the impact of all transitional measures on the consumer price index would be very high, reaching +7 pp by 2040. However, disinflationary macroeconomic effects could also occur in the medium term. The classification of these effects, carried out by the Banque de France12 and found in the Pisani/Mahfouz report, according to their origin and the scenario considered, is particularly illuminating.

Firstly, some disinflationary effects could come from a negative demand shock linked to the transition policies put in place. This type of effect could occur in a scenario where high uncertainty generates a crisis of confidence among the various actors. This uncertainty would lead to a drop in household consumption via an increase in their precautionary savings13, as well as a drop in private investment. This would result in lower aggregate demand than in a scenario with no period of uncertainty, which would have a negative impact on economic activity and prices.

In its study, the Banque de France estimates that such a scenario would have a maximum negative impact on inflation of around -0.75 points after five quarters. A negative demand shock could also be the result of a poor calibration of carbon tax increases and a lack of redistribution policies that would lead to a decline in households’ disposable income, bringing in its wake lower consumption and inflation. Finally, the change in household behaviour (towards sobriety) called for by the fight against global warming (transports, energy, clothing) could also have a negative impact on prices.

Disinflationary pressures could also arise from the positive effects of the green transition on supply. These effects would occur in the medium/long term in a scenario where green investments, particularly those from the private sphere, would generate productivity gains that are large enough to offset the inflationary effects of the transition. According to the Banque de France, such a scenario would be disinflationary for France after five years, with an impact of -0.8 points on inflation.

Conversely, transition policies could also have short-term inflationary macroeconomic effects. Some public policies, such as the Inflation Reduction Act in the United States or NextGenerationEU14 in Europe, contribute to stimulate global demand, including for materials needed for decarbonised production and renewable energies. Initially, these goods will be more expensive than those currently in use and this increase in demand, in the face of still inadequate supply, will lead to higher prices, as identified above. More generally, the positive demand shock triggered by the rise in public spending could help inflation spread, especially if the fiscal support is financed by an increase in the carbon tax.

In the long run, such public investments in favour of decarbonisation could nonetheless help reduce inflation by increasing productivity, in the same way as private investments are expected to do.

Finally, as mentioned previously, negative supply shocks could also cause inflationary effects, such as a disorderly rise in carbon pricing, too sharp a tightening of environmental regulations, or an acceleration of capital obsolescence.

To conclude, the “positive” disinflationary effects mentioned – those arising from improved supply – seem uncertain, if not hypothetical. Above all, they would only occur in the medium to long term. They could then potentially dominate inflationary effects, once the transition period is over and economies have actually decarbonised. In the short term, however, the inflationary effects of the energy transition are likely to prevail.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.