Gold higher as yields get pinned

A mildly positive start to the Friday session for European markets after Wall Street set fresh records, with the S&P 500 jumping to a new all-time high even as data showed US inflation surged in May. US CPI rose to 5% last month, whilst the core reading rose to +3.8%, the highest in 30 years. Core month-on-month declined from 0.9% in April to 0.7% in May but still remains extremely high. Rates actually fell with the 10yr Treasury under 1.44%, sending the dollar to under 90 and gold firmer.

Hot inflation readings right now are pretty much fully priced and understood, as is the reaction function of central banks: they see it as transitory, nothing to worry about. This was evinced by the European Central Bank yesterday, which stuck to the inflation-is-temporary script. It raised expectations for growth and inflation this year but sees inflation at just 1.4% in 2023. The message from the ECB was that things are much better, but we are not about to ease off.

The ECB said it sees risks to the growth outlook as "broadly balanced", for the first time since December 2018. And the statement was quite dovish given upgrades, with the bank saying that “the Governing Council expects net purchases under the PEPP over the coming quarter to continue to be conducted at a significantly higher pace than during the first months of the year”. We might have expected them to drop the word significantly at this meeting. It’s all set up nicely for a battle over the summer between the hawks and doves – if the data continues its current trajectory, we should anticipate a September taper announcement.

Bank of America’s closely-followed Flow Show shows strong flows to bonds, with $12.5bn inflows vs $1.5bn to equities in the last week. The paper notes dryly that “nobody knows how to trade inflation, everybody knows how to trade ‘don’t fight the Fed’.” This is an apt way of describing the fact that just about no one around today really understands either a strong and sustained period of inflation, nor a proper bear market. Just because you’ve not had to deal with it before doesn’t mean it can’t happen.

Yields falling on a hot inflation print seems counter-intuitive. But while inflation is surging, inflation expectations are not shooting higher. As such, at its meeting next week, the Fed can still argue that the inflation we are seeing is a factor of base effects and short-term supply problems. The question remains: at what point does the stream of higher inflation readings become more than just transitory?

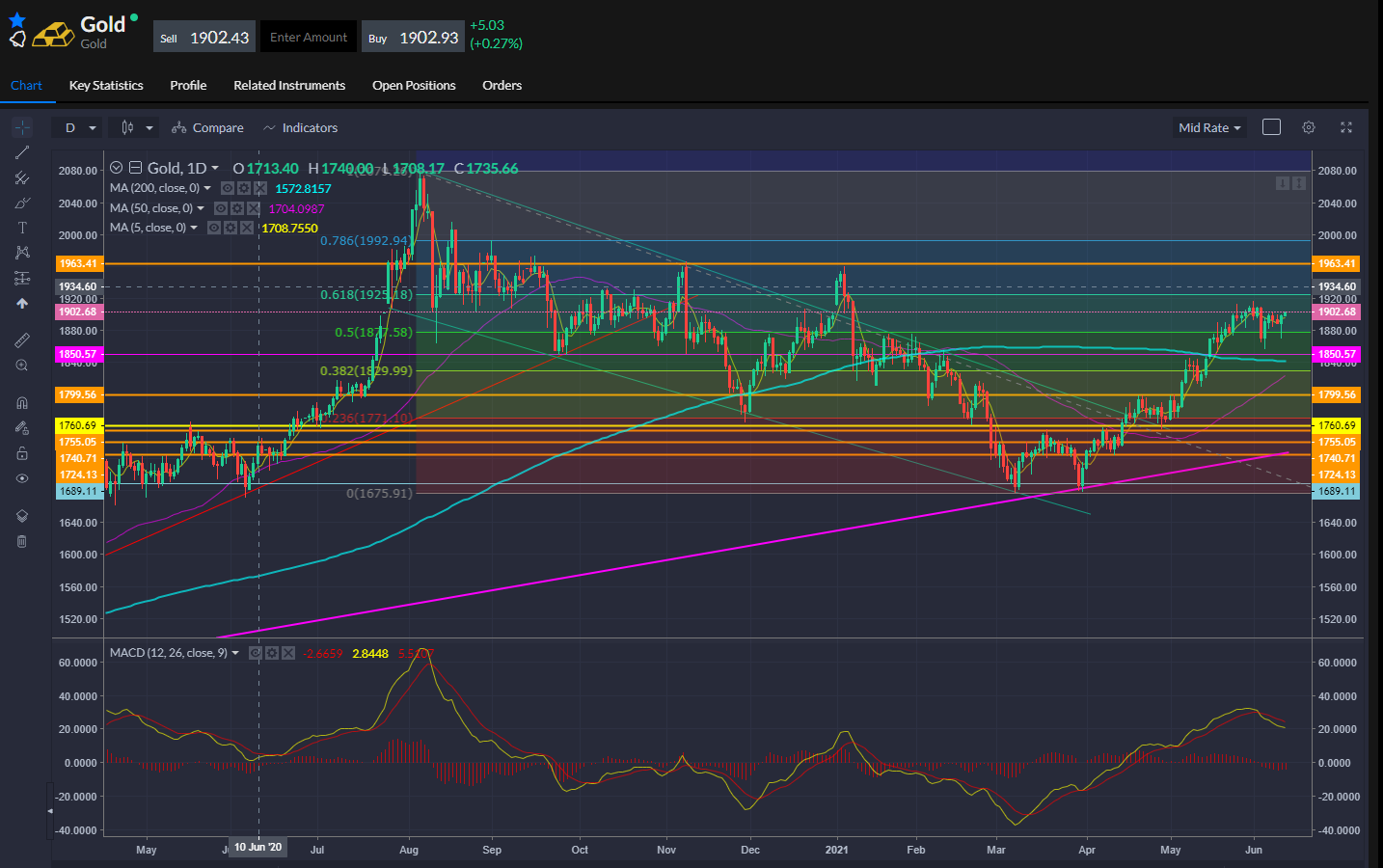

With yields sinking to fresh 3-month lows, real rates (TIPS) shot lower too, giving a helping hand to gold. The set up for gold looks promising – rising inflation + a Fed willing to keep its thumb on yields, producing even-more negative real rates. Prices have clawed back the $1,900 level and could be heading for the $1,960 region if the recent peak at $1,196 can be cleared. Failure to retain the $1,900 could see the 50% retracement at $1,877 again.

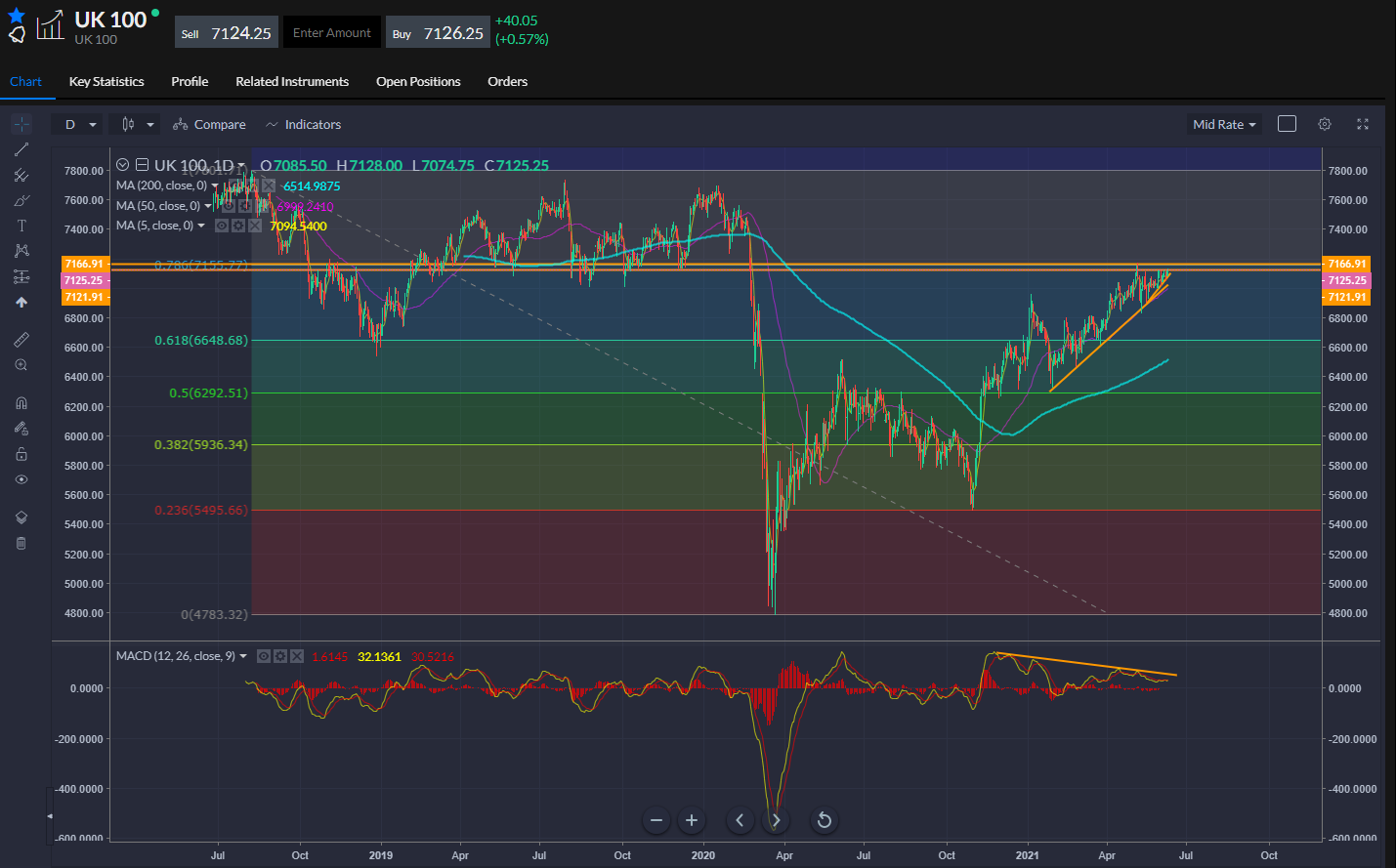

The FTSE 100 is testing the near-term highs around 7120 in early trade – a break could call for test of the post-pandemic peak at 7,164 at the top of the ascending triangle. Continued MACD divergence is a headwind.

Author

Neil Wilson

Markets.com

Neil is the chief market analyst for Markets.com, covering a broad range of topics across FX, equities and commodities. He joined in 2018 after two years working as senior market analyst for ETX Capital.