GDP growth and currency level have a positive correlation

Outlook:

It’s a slowish news week ahead with the Big Kahuna on Friday—US GDP. Before then, we get eurozone PMIs, expected to show a slowdown but implying growth is still pretty good, if decelerating.

We also get the latest US trade numbers with their usual implications for Trumpian rhetoric. Most of it will be wrong because Trump can’t see past the numbers and will fail to note that front-loading imports (and losses from falling exports of things like the famous soybeans) will temporarily skew the numbers. The trade deficit is a drag on growth, but inventory stocking is a boost.

The US growth rate was a whopping 4.2% in Q2 and is likely to be at least 3% in Q3 and likely 3.4% (WSJ), the best performance in 13 years. Bloomberg notes the last time the US had growth averaging 3% was 2005, before the financial crisis. The Atlanta Fed remains the biggest cheerleader, with 3.9% as of last Wednesday (and another estimate this coming Thursday).

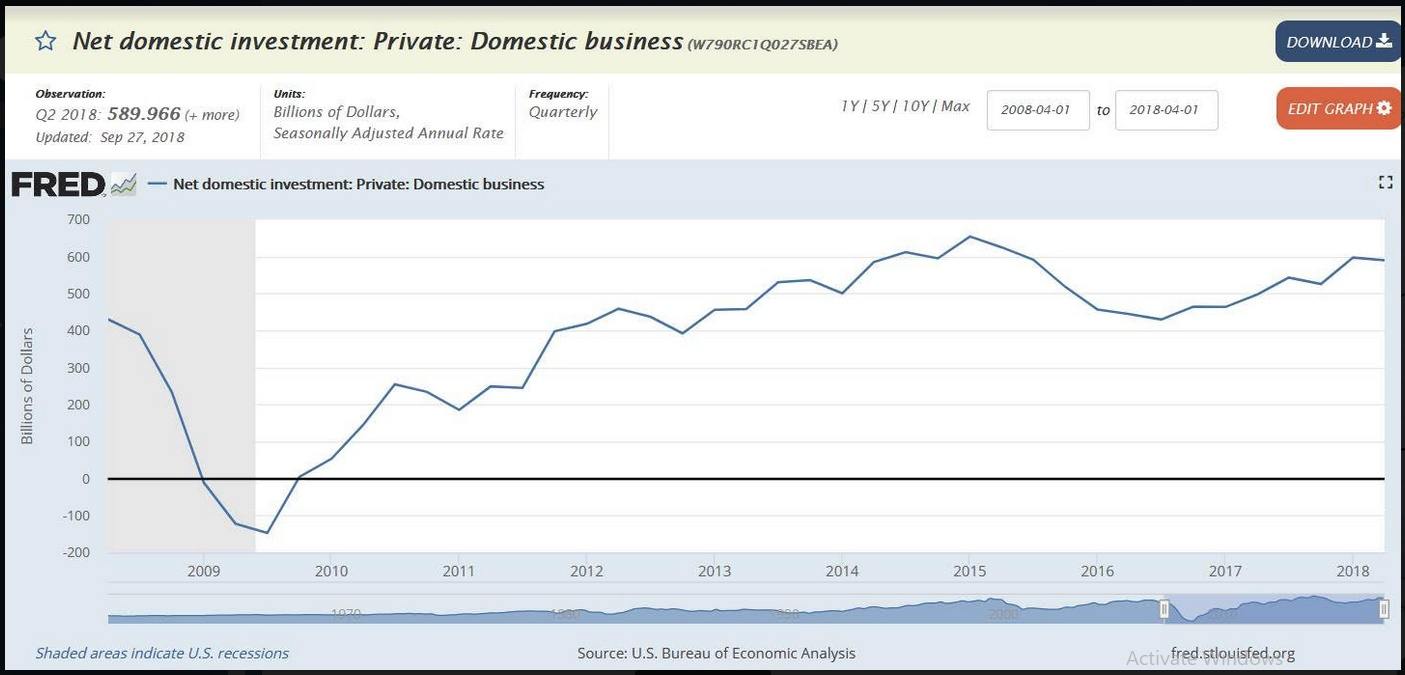

Market Watch notes “business investment has risen at an average 8.6% annual clip in the last six quarters. And that in turn reflects strong spending by consumers who are very confident in the economy.” Well, let’s not forget the tax cut, too, which must have nudged investment along. But we were surprised by the number so checked with Fred. See the chart. You don’t have to grasp all the ins and outs of the data to appreciate that the growth rate is pretty robust and GDP “should” be dollar-favorable. Over long periods of time, GDP growth and currency level have a positive correlation.

The dollar’s rally can still be interrupted by the cooling of the Italian drama, if that’s what we are getting. It’s probably too early to say Brussels is going to retreat and be less obnoxious and supercilious to Italy, but we had no outbursts over the weekend, and that’s a very good sign, indeed. The Moody’s downgrade was not as bad as feared, but it’s only the first of the ratings agencies to issue a judgment. And it’s a weaselly judgement, too. The “stable” outlook is a joke when every analyst is worried that growth with not suffice to keep the deficit at 2.4% instead of ballooning to some hideous number. We face another 3-4 weeks of potential drama. First comes the official EC judgment on the budget, then Italy has three weeks to craft a response. At a guess, Italy is not going to back down and today’s relief will be short-lived. An Italy-EC clash is likely the biggest risk today.

One of the most potentially interesting events this week will be whatever Mr. Draghi says at the press conference after the ECB policy meeting on Thursday. No decisions are expected but the reporters at the press conference are not going to miss the chance to push Super Mario’s back against the wall. Because he is nothing is not consistent, Draghi is likely to repeat that QE is ending at year-end this year and rate changes should not be expected before late next year, if then. He can’t appear to be favoring Italy, but at the same time, he will be hard-pressed to avoid commenting on the Brussels/Rome clash. Since the ECB is totally divorced from fiscal matters, he will likely avoid saying anything directly, but his tone and gestures and body language may speak volumes.

Bottom line, we expect the Italian drama to proceed the same way all these dramas proceed—with visible ill-will and general crankiness. It can’t be euro-favorable. The current respite is likely short-lived.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat