GBP/USD Forecast: End of the Boris bounce? Scary scenarios and hard data eyed

- GBP/USD has attempted a rise as amid the PM's discharge and worrying forecasts.

- Hard data for March and PMIs for April will likely set the tone.

- Mid-April's daily chart is painting a mixed picture.

- The FX Poll is showing a bearish trend.

Pound/dollar has hit the highest in a month amid Prime Minister Boris Johnson's discharge from hospital and US dollar weakness. After the OBR published worrying scenarios and markets'volatile week, economic figures are eyed.

This week in GBP/USD: Is the worst over?

Boris is back – at least out of the hospital, but still not back in Downing Street. After several days between life and death in intensive care, the PM is resting in Chequers and is set to return to work. The excellent news supported the pound. Johnson was elected by a landslide and Foreign Secretary Dominic Raab – who is deputizing – and other ministers lack the political clout.

Yet while the PM is recovering, Britain's coronavirus situation remains dire. The curve is hardly flattering, and that is happening only when counting confirmed COVID-19 mortalities. Deaths at care homes and the total losses of life in the UK suggest that the real number of victims from the disease is significantly higher.

The government has come under growing criticism for failing to ramp up testing, especially in comparison to Germany. Having a capacity of 100,000 probes per day – as health minister Matt Hancock wants – would allow the easing of the lockdown and a gradual return to normality. However, Raab presided over a decision to extend the shuttering for another three weeks – at least.

The longer the shuttering continues, the worse for the economy. The Office of Budget Responsibility has published a scenario in which Gross Domestic Product plunges by 35% in the second quarter and falls by a total of 13% in 2020. The International Monetary Fund also released gloomy forecasts. It is essential to note that the level of uncertainty is extremely high.

In the US, coronavirus continues spreading at a rapid pace, with a third of new deaths happening in the world's largest economy. President Donald Trump wants to reopen the economy as soon as possible and clashed with state governors by claiming he has total authority. Trump also withdrew funds from the World Health Organization, blaming it for taking China at its word.

Upbeat Chinese trade figures have temporarily lifted the market mood and weighed on the US dollar, but the general picture remains downbeat.

US Retail Sales for March plunged by 8.7%, worse than expected. Jobless claims topped five million – better than the previous week – but painting a grim picture. Other data points such as housing figures also disappointed and the Federal Reserve's Beige Book spoke about "severe" damage.

US data weighed on the market mood and sent the safe-haven dollar higher.

UK events: Up-to-date data, coronavirus updates

COVID-19 statistics will likely be closely watched for signs of flattening and bending it down. The debate about whether to incorporate unconfirmed coronavirus mortalities at care homes will likely remain lively, as will figures related to testing.

The health data feeds into the decision about loosening restrictions and, to a lesser extent, about extending the lockdown in early May. If Boris Johnson returns to addressing the press, his words will carry more weight than any of his peers in government.

Longer lockdowns mean more near-term and long-term damage to the economy, and some evidence of what has already happened is on the docket as well.

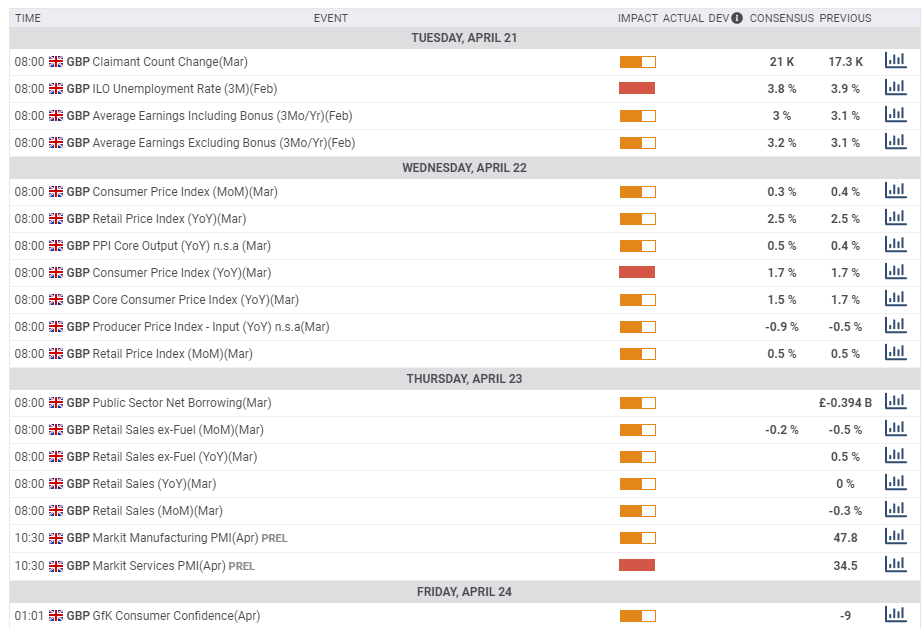

The UK calendar kicks off with the jobs report. The Claimant Count Change – jobless claims – for March will likely stand out. While the figure is volatile, it may begin reflecting how coronavirus hurt the labor markets. A considerable increase is likely. The Unemployment Rate and Average Earnings – that draw attention in normal times – are for February, and will likely be disregarded by markets.

The Consumer Price Index is due out on Wednesday and is unlikely to print significant changes. The Bank of England is following developments related to the disease and ignoring inflation. Even if CPI leaps due to hoarding, the BOE will leave rates at rock bottom levels. Nevertheless, the release may provide a baseline for future decisions.

The calendar is packed on Thursday, with Retail Sales data for March kicking off the day. It will likely show significant falls on all measures, apart from groceries. While the lockdown began only on March 23, a drop in consumption may already be seen now. Public Sector Net Borrowing is also of interest and could show how public debt has already begun rising in response to the crisis.

The final publication already looks to the future. The Markit/CIPS preliminary Purchasing Managers' Indexes for April will likely continue showing poor prospects, especially in the services sector. The Manufacturing PMI will likely remain elevated due to a quirk that counts delays in deliveries as positive. However, the services PMI is probably going to remain below 40, reflecting ongoing depression. Any score below 50 represents contraction.

Overall, a busy week awaits investors.

Here is the list of UK events from the FXStreet calendar:

US events: Health vs. economic considerations

Coronavirus figures will likely show improvement, yet the pace could remain slow. Does it justify easing restrictions and opening the economy? Health officials will probably urge extending the shelter-at-place orders while Trump is set to demand a return to normal. State governors – who have the authority – are expected to consider matters carefully and try to balance between the economic impact and saving lives.

See Coronavirus Exit Strategy: Three critical factors to watch and how they impact currencies

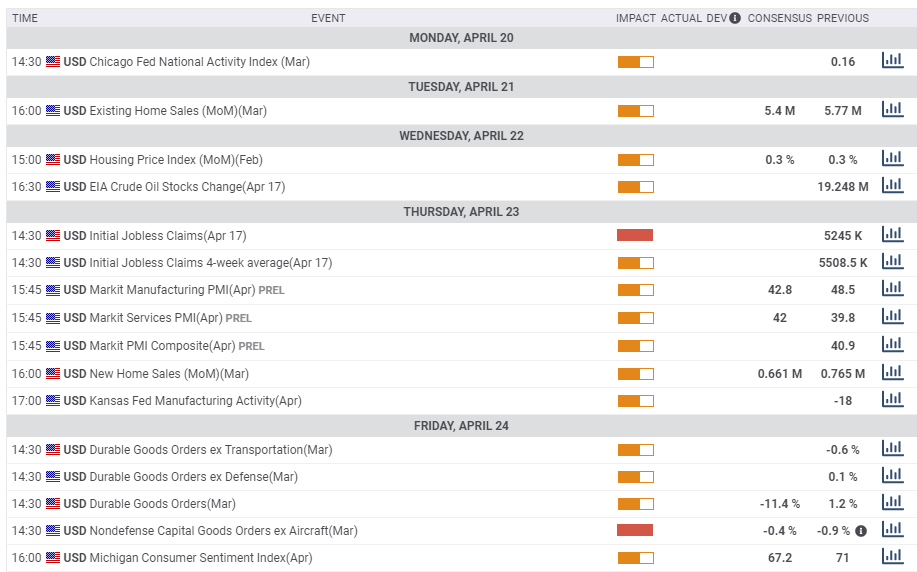

Existing Home Sales figures for March will be of some interest, but weekly Unemployment Claims – as well as Continuing Claims – will likely trigger a more significant reaction. Both numbers are forecast to remain in the millions. Markit's preliminary PMIs for April and may converge around the low 40s after pointing to different directions beforehand.

Durable Goods Orders statistics for March close he week. Headline orders have likely plunged as Americans entered a lockdown and as plane sales tumbled. Core sales and especially the nondefense ex-aircraft figures, are expected to drop only moderately.

Here the upcoming top US events this week:

GBP/USD Technical Analysis

GBP/USD is capped by an uptrend resistance line that has been accompanying it since late March and has failed to make a convincing break above the 50-day Simple Moving Average. However, momentum has turned to the upside and the currency has posted higher highs and higher lows – a bullish sign.

All in all, the picture is mixed.

Some support is at the round level of 1.24, which was a stepping stone on the way down and a cushion in mid-April. It is followed by 1.2250, a swing low in late March, and by 1.2165 – April's low. The next lines to watch are 1.1980 and 1.18.

1.2490 remains significant after it served as a stubborn cap in late March and early April. The next significant resistance is only at 1.2645, April's high. The next line to watch is the pre-crash trough of 1.2730. Next, 1.2850 awaits.

-637226536154274259.png&w=1536&q=95)

GBP/USD Sentiment Poll

Weak data from the UK will likely weigh on the pound and disappointing American figures could continue sending investors to the safe-haven dollar. Without upbeat figures and more than a slow flattening of the curve, GBP/USD has more room to fall.

The FXStreet Forecast Poll is showing that experts expect a bearish trend in the short term, sideways later on – most of those surveyed think so – and then a bearish trend. The average targets have been upgraded.

Related Reads

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.