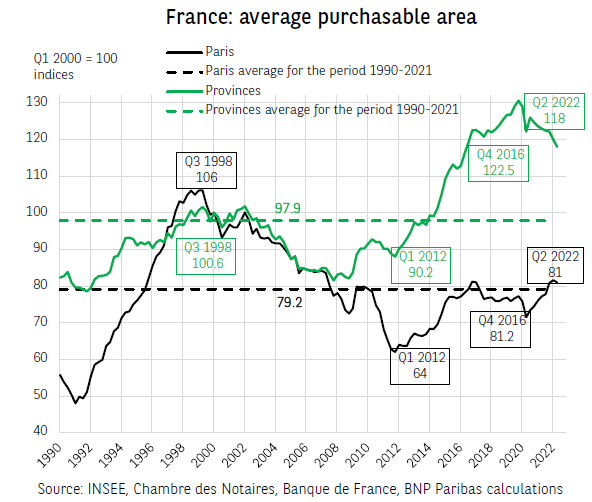

France: Households’ property purchasing capacity is improving in Paris

Our households’ property purchasing capacity indicator tracks the development in the maximum purchasable area of a representative household in France. Before rebasing (Q1 2000=100), it compares borrowing capacity expressed as an amount (calculated according to the average household income, fixed interest rates and the average duration of loans) to the price of old housing per square meter. In the provinces, Households’ property purchasing capacity was significantly higher than its 1990–2021 average (+21%) in the second quarter of 2022; however, in Paris, where the longterm average takes into account the 1990 property bubble which had undermined households’ property purchasing capacity, it was almost equal to its 1990–2021 average (+2%).

Starting in 1990 from a particularly deteriorated level (peak of the bubble), Households’ property purchasing capacity more than doubled until 1998 in Paris (+143%) not only due to the deflation of the bubble (drop in prices of 34%), but also to the increase in household income (+14% between 1991 and 1998) and the reduction in the cost of credit (from around 11% to 6%)1. In the provinces, the rise in prices over the same period absorbed a large part of the positive effects of income and credit conditions, so that purchasing capacity increased more moderately, by around 39%. Between 2000 and 2007, the reductions in households’ property purchasing capacity were more homogeneous between Paris and the provinces due to comparable price increases. Between 2008 and 2020, the positive effects of the continued drop in interest rates and the lengthening of the average duration of loans were almost completely wiped out by the rise in prices in Paris (+69%), where purchasing capacity even fell by 2.7%. On the contrary, these same factors supported households’ property purchasing capacity in the provinces (+49.7%), where price growth was limited to +4.7% over the same period.

Since 2020, the Covid-19 crisis and the price levels reached have been shuffling the deck: Paris is losing its appeal to the benefit of medium-sized cities, which have become more attractive due to the lockdowns and teleworking opportunities. Prices are slowing in the capital (+1.2% between Q1 2020 and Q2 2022 compared with +18.2% in the provinces). In a context of relatively stable credit conditions, the main determinant of the development in purchasing capacity was the gap between rises in households’ income (+7.2% over the same period) and that of house prices. It therefore recovered in Paris (+6.9%) while it declined in the provinces (-8.5%) from a record level in 2020. In the coming quarters, the impact of the sharp rise in bond market rates since the beginning of 2022 on bank loan conditions could contribute to an adjustment in prices that could alleviate the effects on households’ property purchasing capacity.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.