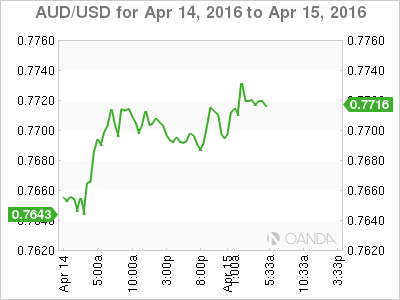

The Australian dollar has posted small gains on Friday, repeating the trend which marked the Thursday session. AUD/USD is trading at the 0.7710 line in the European session. In economic news, Chinese GDP edged lower to 6.7% but matched the forecast. In the US, today’s key event is UoM Consumer Sentiment, with the estimate standing at 91.9 points. As well, the US releases two important manufacturing reports – the Empire State Manufacturing Index and Industrial Production.

Chinese GDP for the first quarter posted a gain of 6.7%, down from 6.8% in the previous quarter. A year ago, GDP stood at 7.7%, as the Chinese economy has contracted, causing negative economic repercussions across the world. Although the Chinese economy appears to have stabilized, much of the momentum in economic activity may not be sustainable, since it is based on a surge in domestic credit levels, which may not be sustainable. The ease in credit has propelled gains in housing and real estate, sectors which could easily reverse directions. The use of easy credit to help prop up the economy has led to a “debt dependency” which could be a double edged sword, so analysts continue to monitor the Chinese economy, the second largest in the world, with a great deal of apprehension.

Australia posted excellent job numbers in March, helping the Aussie push above the 0.77 line on Thursday. Employment Change jumped by 26.1 thousand, easily beating the forecast of 18.6 thousand. This was the indicator’s strongest reading in 4 months. The unemployment rate followed suit, falling from 5.9% to 5.7%, the lowest jobless rate since October 2013. The strong job numbers correlate with a strong rise in business confidence, and give the RBA some breathing room regarding rate cuts. The central bank has stated on numerous occasions that it will cut rates if economic conditions warrant, but a stronger labor market could help create more inflation and allow the RBA to remain on the sidelines at its next policy meeting in May.

US inflation indicators continue to point to a soft inflation picture. CPI and Core CPI, key gauges of consumer inflation, posted small gains of 0.1%. The Core CPI release was particularly disappointing, coming after two consecutive gains of 0.3%. The weak inflation numbers will make it difficult to make a case for raising interest rates in the first half of 2016 and bolsters the dovish position of Janet Yellen and her supporters. Deustche Bank analyst Brett Ryan summed up the soft US inflation picture, noting that “we’re still importing deflation from other areas of the world”. There was much better news on the employment front, as Unemployment Claims fell to 253 thousand, its lowest weekly reading since March 1973. This release is another confirmation of a robust US labor market.

The US economy continues to perform well, despite some weak sectors, such as the manufacturing industry. US manufacturers continue to face stiff competition with countries that pay much lower wages, such as China, India, Bangladesh and other Asian countries. With turbulent global economic conditions leading to weaker demand, the manufacturing sector is facing additional challenges. The Empire State Manufacturing Index has recorded mostly sharp declines since the second half of 2015, but the markets are hoping for a gain in the March report.

AUD/USD Fundamentals

Thursday (April 14)

- 21:30 RBA Financial Stability Review

Friday (April 15)

-

8:30 US Empire State Manufacturing Index. Estimate 2.1

-

9:15 US Capacity Utilization Rate. Estimate 75.4%

-

9:15 US Industrial Production. Estimate -0.1%

-

10:00 US Preliminary UoM Consumer Sentiment. Estimate 91.9

-

10:00 US Preliminary UoM Inflation Expectations

-

16:00 US TIC Long-Term Purchases

| S3 | S2 | S1 | R1 | R2 | R3 |

| 0.7472 | 0.7560 | 0.7678 | 0.7796 | 0.7913 | 0.8054 |

-

AUD/USD has shown limited movement in the Asian and European sessions

-

0.7678 remains a weak support line

-

There is resistance at 0.7796

-

Current range: 0.7678 to 0.7796

Further levels in both directions:

-

Below: 0.7678, 0.7560, 0.7472 and 0.7385

-

Above: 0.7796, 0.7913 and 0.8054

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities.

Opinions are the authors — not necessarily OANDA’s, its officers or directors. OANDA’s Terms of Use and Privacy Policy apply. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Recommended Content

Editors’ Picks

EUR/USD edges lower toward 1.0700 post-US PCE

EUR/USD stays under modest bearish pressure but manages to hold above 1.0700 in the American session on Friday. The US Dollar (USD) gathers strength against its rivals after the stronger-than-forecast PCE inflation data, not allowing the pair to gain traction.

GBP/USD retreats to 1.2500 on renewed USD strength

GBP/USD lost its traction and turned negative on the day near 1.2500. Following the stronger-than-expected PCE inflation readings from the US, the USD stays resilient and makes it difficult for the pair to gather recovery momentum.

Gold struggles to hold above $2,350 following US inflation

Gold turned south and declined toward $2,340, erasing a large portion of its daily gains, as the USD benefited from PCE inflation data. The benchmark 10-year US yield, however, stays in negative territory and helps XAU/USD limit its losses.

Bitcoin Weekly Forecast: BTC’s next breakout could propel it to $80,000 Premium

Bitcoin’s recent price consolidation could be nearing its end as technical indicators and on-chain metrics suggest a potential upward breakout. However, this move would not be straightforward and could punish impatient investors.

Week ahead – Hawkish risk as Fed and NFP on tap, Eurozone data eyed too

Fed meets on Wednesday as US inflation stays elevated. Will Friday’s jobs report bring relief or more angst for the markets? Eurozone flash GDP and CPI numbers in focus for the Euro.