Final full week of May welcomes updated inflation data

The week that was

The Reserve Bank of New Zealand (RBNZ) stood pat on rates, consequently leaving the Official Cash Rate (OCR) at 5.50% for a seventh consecutive meeting. However, the central bank echoed a hawkish stance that propelled the New Zealand dollar (NZD) to a high of $0.6153. In a nutshell, the peak OCR forecast was raised from 5.60% to 5.65%, and there were talks of policy firming at the meeting, but members settled for a hold. According to the OIS curve, markets are pricing in no change in the OCR this year, though November’s meeting is still possible (-23bps of easing priced in).

The FOMC meeting minutes emphasised that while inflation has cooled, the accelerated inflation in recent months highlights a ‘lack of progress’. The minutes also communicated the ‘willingness’ to increase the Fed funds target range should ‘risks to inflation materialise’. Importantly, the minutes revealed doubt concerning the degree of restrictiveness of policy, calling into question whether the neutral rate (r*) is higher and, thereby, higher rates may be less effective than in the past. You will recall that the May FOMC meet saw the Fed funds target rate remain unchanged at 5.25%-5.50% for a sixth successive meeting. The Rate Statement communicated a lack of progress on inflation and maintained the message of requiring greater confidence in the disinflation process before easing policy. Fed Chair Jerome Powell added that it would take the Fed longer than anticipated before reaching that level of confidence, though the Chief did note that his ‘personal forecast’ was that inflationary pressures would begin to subside again this year. Clearly, he was correct in the month of April!

Headline UK inflation slowed to +2.3% in the twelve months to April, down from +3.2% in March (consensus: +2.1%); the drop was expected due to the reduction in the Ofgem energy price cap regulation in the UK. The latest inflation data mark the lowest inflation rate since 2021 and evidently place the Bank of England’s (BoE) inflation target of 2.0% within touching distance. Given the slower-than-expected pace of disinflation in the headline number (as well as core inflation also coming in higher than expected and remaining stubbornly high year on year at +3.9% versus the +3.6% estimate [prior: +4.2%]) and services inflation, a metric that the BoE is keeping a close eye on, coming in stronger than expected at +5.9% versus +5.5% expected (prior +6.0%), this will likely throw a ‘spanner in the works’ for a rate cut in June.

Last week, the S&P Global PMIs for May were also a highlight. For the eurozone, the PMIs suggested that the economy gained momentum, portraying an improving economic situation. Input and output prices softened, which will be welcome news at the European Central Bank (ECB). The HCOB Flash Eurozone Composite PMI Output Index hit a 12-month high at 52.3, up from April’s 51.7. The Services PMI remained unchanged, while the Manufacturing PMI rose to a 15-month high of 47.4 (up from 45.7). In the UK, a similar view was seen, bolstering continued recovery following the mild technical recession last year. The Manufacturing PMI departed contractionary territory and recorded a 22-month high at 51.3, up from 49.1 in April. Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, commented: ‘With companies now reporting the slowest price growth in over three years, and headline inflation falling close to the 2.0% target, the PMI data support the view that the Bank of England will start cutting interest rates in August providing the data continue to move in the right direction over the summer’. Stateside, the US PMI also revealed an acceleration in economic performance, particularly in the service sector. The Flash US Services Business Activity Index rose to a 12-month high of 54.8 (up from April at 51.3).

The week ahead: Inflation eyed

Monday will likely be a snoozer, with US and UK banks closing in observance of Bank Holidays.

The majority of focus this week will fall on Friday’s US PCE inflation for April (the Fed’s preferred measure of inflation), alongside personal income and spending. Last week’s FOMC minutes echoed a strong higher-for-longer vibe about the need for rates to remain at current levels for longer than previously anticipated. In light of recent events, traders, investors and the Fed will look for signs of slowing inflation this week, which could influence the US dollar. Estimates for US data call for month-on-month and year-on-year core PCE measures to match March’s prints at +0.3% and +2.7%. Ahead of this print, however, investors welcome consumer confidence data on Tuesday (you may recall that consumer confidence deteriorated for a third consecutive month to 97.0, though it has remained in a sideways trend for over two years). Following this, on Thursday, we’ll get the second estimate (preliminary) for Q1 GDP, which is expected to remain unchanged (annualised rate of 1.6%). All in all, it is a busy one for the US this week.

Friday also welcomes May’s euro area flash inflation data, a widely watched print ahead of the ECB clearly being on the verge of easing policy at June’s meeting. Yet, what is less transparent is the future rate path following a 25bp cut in June, particularly given improved economic conditions (the recent eurozone PMIs indicated improved economic performance) and hotter-than-expected wage growth. Expectations heading into euro area CPI inflation data indicate year-on-year data to rise to +2.5%, up from +2.4% the month prior. While a small increase is likely, this will unlikely deter policymakers from cutting rates In June.

Additional data to watch this week is Aussie CPI inflation for April on Wednesday. As of writing, investors do not expect a rate cut to emerge this year. Friday’s PMI prints for May for China will also likely elevate volatility in Asia Pac hours, a release that can affect the AUD and NZD.

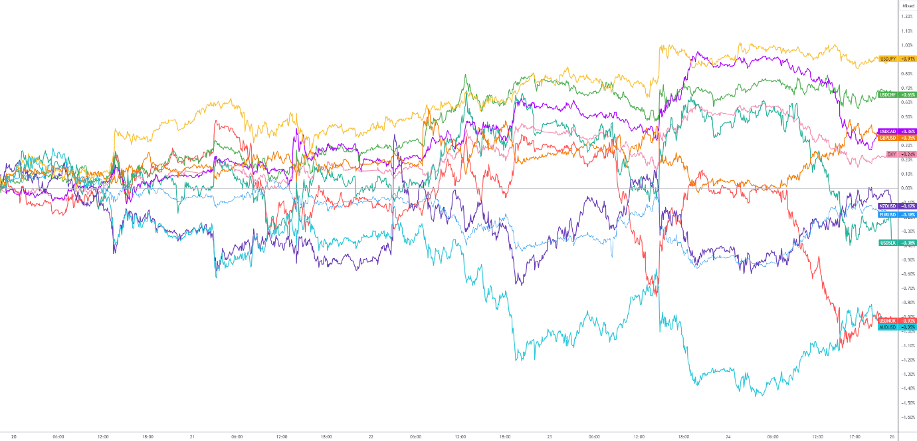

G10 FX (five-day change):

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,