Fed’s Dudley 'Warns of Overheating Risks'

US FED’s William Dudley spoke on Thursday at the Securities Industry and Financial Markets Association in New York. “Over the longer term I am considerably more cautious about the economic outlook,” said Dudley, “Keeping the economy on a sustainable path may become more challenging,” due to the risk of ‘’overheating’’. He made the point that there is a strong case to keep gradually raising rates and that the forecast for 3 rate hikes this year is a reasonable starting point. He said it could go faster or slower depending on data and he wants to achieve 2% inflation before shifting goal higher. He also said that ‘’Tax cuts will come at a cost, pose challenges for Fed.’’ Tax cuts, he said, made him considerably more cautious about the longer-term economic outlook and the cuts give a short-term boost to the economy but pose serious long-term risks. He expects 2.5% to 2.75% GDP growth, inflation hitting 2% in the medium term and unemployment down below 4% in 2018.

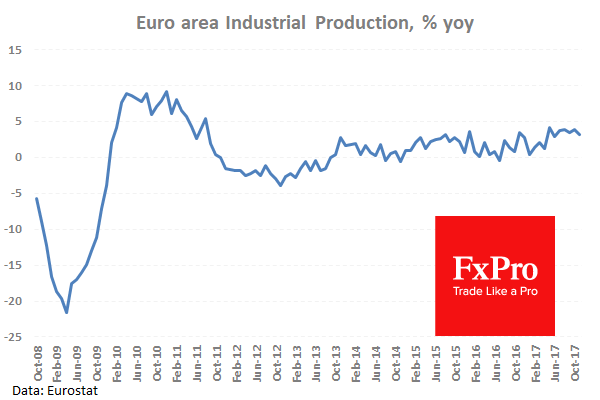

Eurozone Industrial Production w.d.a. (YoY) (Nov) was released with a number of 3.2% from a consensus of 3.0% and a prior of 3.7%, revised up to 3.9%. Industrial Production s.a. (MoM) (Nov) was 1.0% v an expected 0.8%, from 0.2% previously, which was revised up to 0.4%. EURUSD moved marginally lower on the data to 1.19387.

Eurozone ECB Monetary Policy Meeting Accounts were published at 12:30 GMT on Thursday. The ECB said they could consider a ‘’gradual shift’’ in guidance from early 2018. Inflation was an ongoing concern to the ECB and ‘’the relative importance of guidance on rates will increase as inflation rises.’’ They said that a transition to a broader forward guidance, comprising various dimensions of policy stance was warranted and they would revisit the whole issue in early 2018. On the policy side, they had ‘’ increased confidence that inflation pressures would take hold ‘’ and further easing of financial conditions are not regarded as warranted. They saw comfort in wage dynamics but inflation is still a concern. EURUSD soared higher from 1.19364 to reach a high of 1.20587.

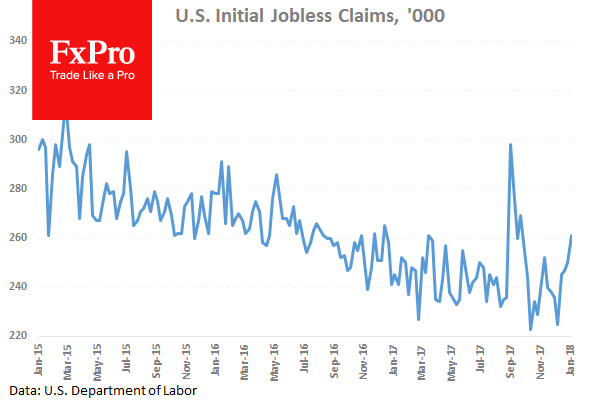

US Continuing Jobless Claims (Dec 29) were 1.867M v an expected 1.915M, from a previous number of 1.914M that was revised down to 1.902M. Initial Jobless Claims (Jan 5) was 261K v an expected 245K, with a prior reading of 250K. USDJPY moved lower after this data release from 111.616 to 111.387.

US Monthly Budget Statement (Dec) came in at $-23B v an estimated $-40B, from a previous $-139B.

New Zealand Building Permits s.a. (MoM) (Nov) was released as 10.8%. The previous reading was -9.6%, but this was revised down to -10.4%.

Japanese Foreign Investment in Japan stocks (Jan 5) came out as ¥597.9B. ¥76.2B was the previous number but this was revised to ¥76.1B. Foreign Bond Investment (Jan 5) came out at ¥173.0B, with the prior number of ¥434.2B revised to ¥427.4B.

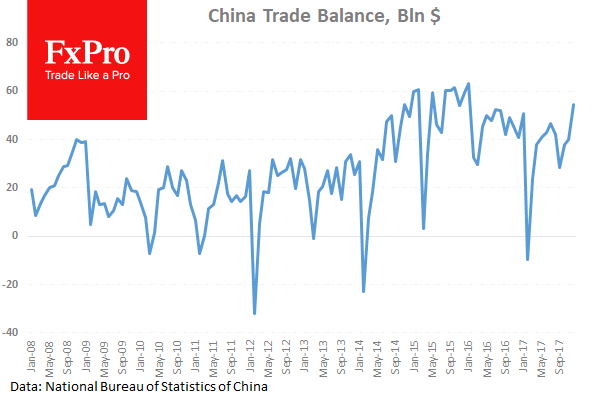

Chinese Imports (YoY) (Dec) were 4.5% v a consensus of 13.0%, from 17.7% previously. Exports (YoY) (Dec) came in at 10.9% v an expected 9.1%, from 12.3% prior. Imports (YoY) CNY (Dec) were 18.7% v an expected 11.8% and 15.6% previously. Exports (YoY) CNY (Dec) were 10.8% v 7.4% expected and 10.3% prior. Trade Balance USD (Dec) was $54.69B v $37.00B expected, from $40.21B prior. Trade Balance CNY (Dec) came in at 361.98B v 254.00B, with a previous read of 263.60B.

Japanese Eco Watchers Survey: Outlook (Dec) was 52.7 v 53.5 expected, from 53.8 previously. Japanese Eco Watchers Survey: Current (Dec) was 53.9 v 55.2 expected, from 55.1 previously.

EURUSD is up 0.11% overnight, trading around 1.20445.

USDJPY is up 0.09% in early session trading at around 111.344.

GBPUSD is up 0.07% to trade around 1.35438.

USDCAD is up 0.15%, trading around 1.25380.

Gold is up 0.47% in early morning trading at around $1,328.38.

WTI is down -0.24%, trading around $63.37.

Major data releases for today:

At 07:45 GMT, French Consumer Price Index (EU Norm) (YoY) (Dec) will be released. An unchanged reading of 1.3% is expected. EUR pairs will be influenced by this data point along with the French Stock market.

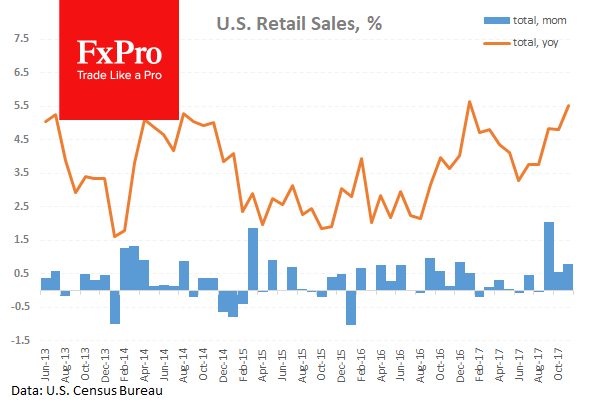

At 13:30 GMT, US Retail Sales (MoM) (Dec) will be released with an expected 0.4% from 0.8% previously. Retail Sales ex Autos (MoM) (Dec) is expected at 0.4% from 1.0% prior. Retail Sales (Dec) Control Group expected at 0.4% from 0.8% prior. Consumer Price Index (YoY) (Dec) is expected at 2.1% from 2.2% previously. Consumer Price Index Ex Food & Energy (YoY) (Dec) is expected to be unchanged at 1.7%. Consumer Price Index Ex Food & Energy (MoM) (Dec) is expected to be 0.2% from 0.1% previously. USD crosses could see increased volatility around this data release.

At 16:30 GMT, German Buba President Weidmann will be speaking at the Ludwig-Erhard summit, in Bavaria. His comments could move EUR crosses.

At 18:00 GMT, Baker Hughes US Rig Count numbers will be released. The prior number last Friday showed that there were 742 Oil rigs in operation. WTI traders will be paying close attention to this number as they look to the week ahead.

At 20:30 GMT, US Federal Reserve Bank of Boston President Rosengren will be speaking and his comments may affect USD crosses, stocks, commodities and bonds.

Author

Team FxPro

FxPro

FxPro is a UK headquartered online broker providing contracts for difference (CFD) on foreign exchange, shares, futures and precious metals primarily to retail clients.