Federal Reserve Preview September 17-18 FOMC: Shifting Odds

- Expectations for a second 25 basis point cut have declined

- Credit market reflect uncertainty over economy, international politics

- FOMC divided on rate cut in July, 7-2

The Federal Reserve will conclude its scheduled two day policy meeting of the Federal Reserve Open Market Committee on Wednesday September 18th. The central bank will issue its decision for the fed funds rate at 2:00 pm EDT, 18:00 GMT. Chairman Jerome Powell will read his statement and hold a news conference beginning at 2:30 pm EDT, 18:30 GMT

Federal Reserve Policy and the Economy

The already complicated economic and bureaucratic circumstances for Wednesday’s Federal Reserve decision were further disturbed when Saudi oil facilities were attacked over the weekend throwing the world oil market into turmoil and casting a pall over the global economy.

On the surface the US economy would not seem to need additional support. Growth averaged 3.1% in the first quarter, 2.0% in the second and is tracking at 1.8% in the current period according to the Atlanta Fed’s GDPNow model.

Industrial production rebounded in August to 0.6%, three times its forecast after July’s 0.1% loss.

Reuters

The declining GDP masks considerable strength in the labor market. Wages have increased at 3.0% or better for 13 months, and unemployment at 3.7% is near a five decade low, with record levels for African-American and Hispanic workers. While job creation has cooled this year, the three month moving average has dropped from 245,000 in January to 156,000 in August, the two year burst of employment after the 2016 election has left the economy with a backlog of unfilled positions. That surplus is one of the factors driving wages higher.

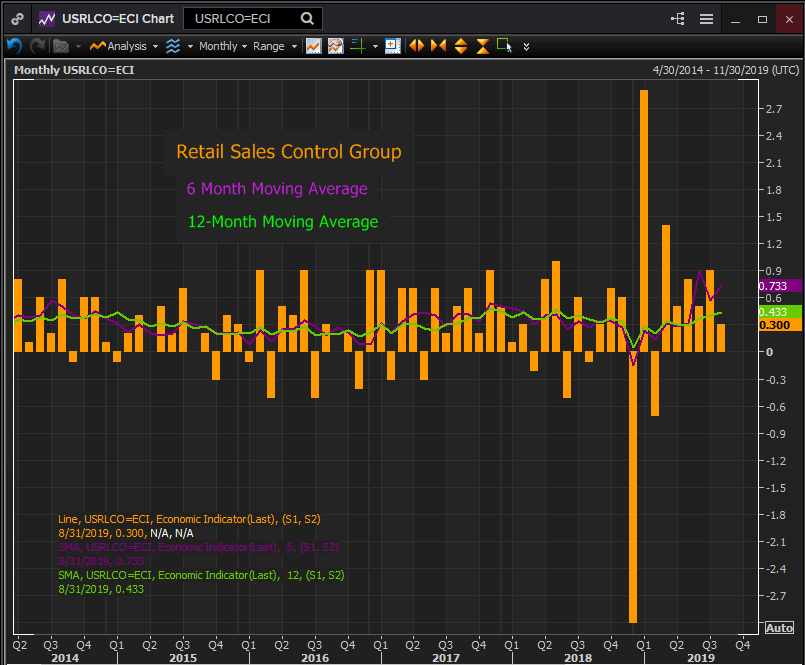

Consumers have taken their income to the stores and internet. Retail sales have been positive for six months and the 0.733% average monthly increase of the control-group over that half year is the best in 16 years.

Reuters

It is good for the economy that consumer attitudes reflect the labor market because it is consumption that is fueling growth. Business investment has been curtailed by concerns over the US China trade dispute and a slowdown in economic growth worldwide. Manufacturing has been the hardest hit with job growth dropping from a 3 month average of 25,000 last December to 6,000 in August.

The current rate of spending in the consumer sector which is about 70% of US economic activity is commensurate with GDP expansion between 2.0% and 2.5%.

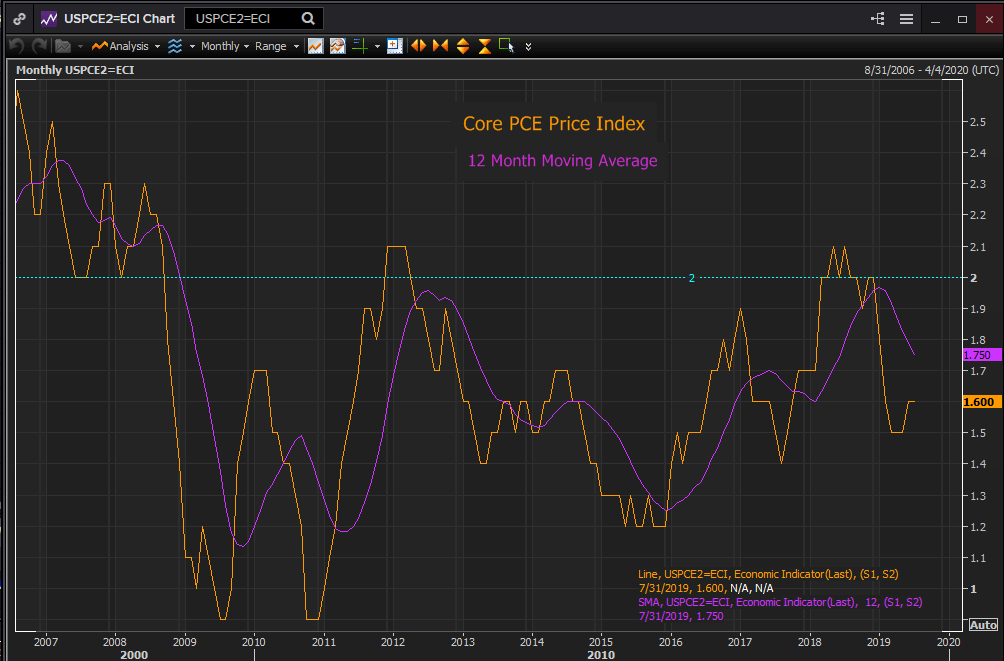

Inflation has fallen sharply this year. The core PCE price index the Fed’s preferred gauge has shed 0.4% from 2.0% in January to 1.6% in July. The August figures will be reported on September 27th.

Reuters

While the US has slowed since the first quarter and inflation is, as it has been for most of the past decade, below the Fed’s 2% target, the overall economic performance has been good, as the Fed itself has noted many times.

The Fed’s rate reduction logic is not domestic. Chairman Powell has repeatedly cited the need to defend the economy and the labor expansion against external threats. The US China trade dispute has damaged business sentiment and investment here and the pending British exit from the EU has had a similar impact in Europe.

Beyond the specific trade uncertainties global growth has slipped and with Germany on the brink of a recession, China’s industrial sector weakening and Europe beset with political unrest in Italy and France and Brexit the risks are almost all negative. The Fed, as Mr. Powell has said, is taking out insurance.

Credit Markets

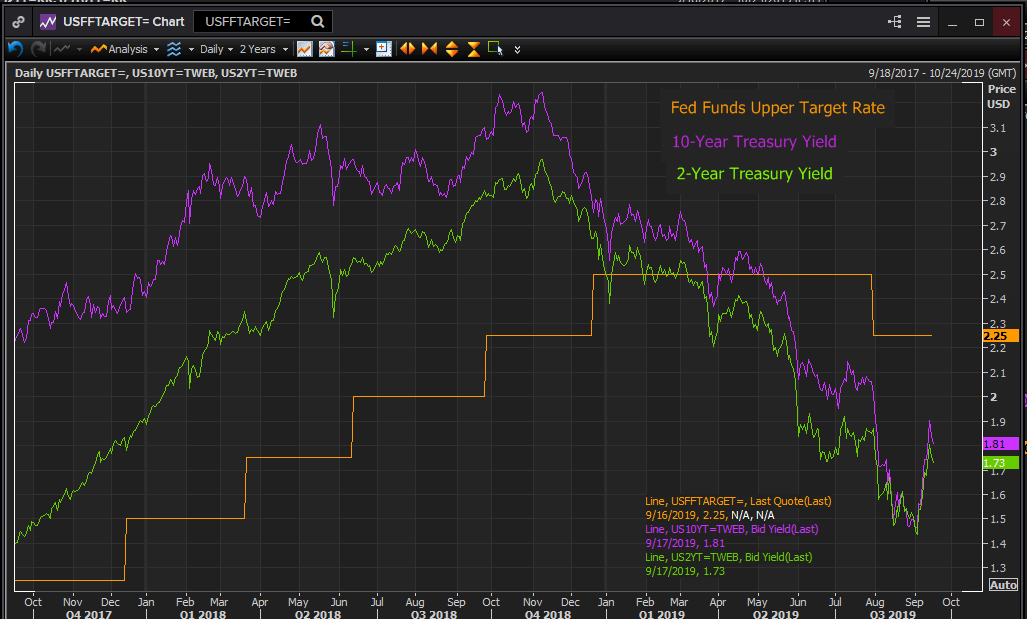

The Treasury market has been predicting lower interest rates well in advance of the Fed.

The returns of the 2 and 10-year Treasuries began falling last November even before the Fed completed its last fed funds increase that December. The recent brief inversion of the 2-10 year spread, an historically accurate predictor of recession, reinforced the fear that whatever the current state of the American economy it was unlikely to remain isolated from the burgeoning troubles overseas.

Reuters

Futures

The treasury futures market is still heavily weighted towards a lower fed funds rate by the end of the year but the timing has changed substantially.

Last month the futures were rating the chance of a second 25 basis point cut at Wednesday’s meeting at over 90%. As of the FOMC morning the odds for a reduction had dropped to 70.4%.

CME Group

At the final FOMC for this year on December 11th the odds for additional cuts or a pause at the 2.00% upper target are identical at 43.6%.

CME Group

The shift in market sentiment is due to two factors. The economy has slowed this year but there is no sense in the statistics that it is headed for a slump. The salient fact behind the drop in GDP is the pullback in business investment, a development tied to a specific situation, the trade dispute with China. Settle or ameliorate that and business spending and GDP will recover. None of the traditional indicators, employment, wages, labor force participation, initial jobless claims point to a deepening slowdown in economic growth.

At the July FOMC two governors dissented. Eric Rosengren of Boston and Esther George of Kansas City voted to leave the Fed funds rate unchanged. Their logic, as above, was that nothing economic warranted a rate cut. While disagreement on policy is not unknown the votes of two governors, backed by the performance of the economy over the past six weeks may move others to caution.

Economic Projections

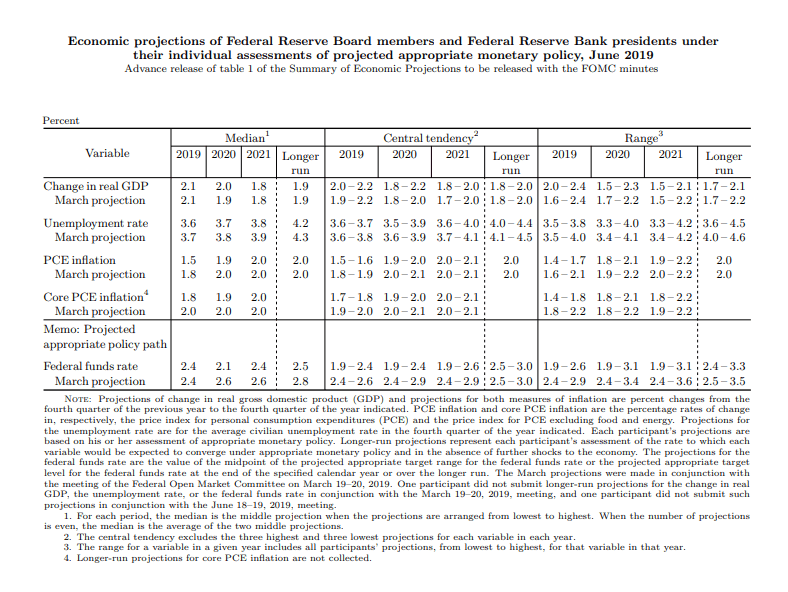

The Fed and its analysts distill their views of the US economy and rate policy into a set of projections four times a year. The third issue is due on Wednesday.

In the prior release on June 19th the central tendency for the fed funds rate at the end of 2019 was 2.4%, as it had been in March. It envisioned no rate reductions through year end. That estimate limited the switch to the more accommodative policy that began on July 31st conditional on developments that took place in the second quarter and July. Economic growth this year was projected to be 2.1% and 2.0% next.

The rate estimate for 2020 in the June materials was 2.1%, where the fed funds are now. If there is a serious change in the Fed’s thinking on the immediate future, this is where it will show up.

Mr. Powell has portrayed the change in rate policy as a precaution justified by external risks. The question is does the Fed think those risks have become embedded in the US economy?

Conclusion

The circumstances of the US economy have not changed in the past six weeks. Brexit has moved closer if the October 31st exit date is honored. The trade war with China has moderated from antagonistic rhetoric. New negotiations are set to begin next month but expectations for a deal are low.

American economic growth appears to have stabilized around 2%, the labor market is strong as are equities. Yields in the 2-year Treasury have regained about 30 points from their low earlier in the month, in the 10-year it is almost 40. The 2-10 spread has moved out to 8 points after inverting briefly.

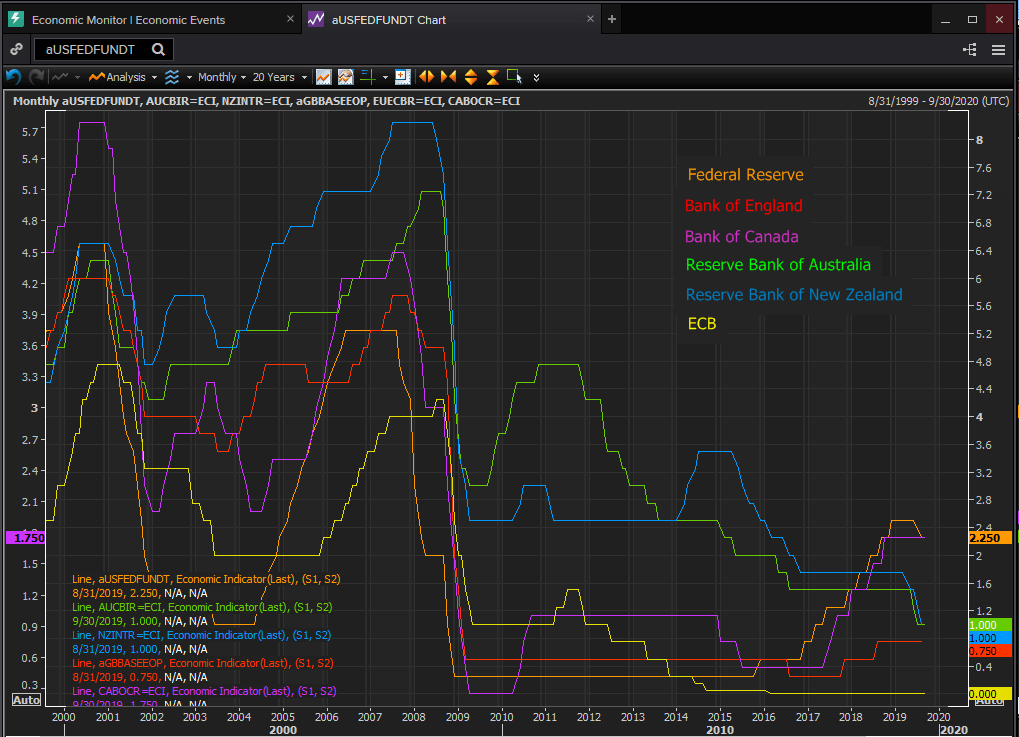

The Fed joined the central banks of Australia, New Zealand and the Eurozone in reducing rates but Canada and England have declined to do so. The movement to greater accommodation and the view that the globe is headed for recession is not universal.

Reuters

The recent attack on the Saudi refinery could be the start of a prolonged conflict over production facilities in and around the Persian Gulf. All such installations are extremely vulnerable and a large and sustained increase in crude prices might tip a weak global economy into decline. But the Fed will not condition policy on the prospect of higher crude prices.

The Fed’s bias must still be judged towards further reductions but the timing and extent is unclear. The most probable outcome of today's meeting is a 0.25% cut coupled to a pause for economic assessment. Mr. Powell will be hard pressed to make a confusing and somewhat unstable situation clear, someone is bound to be disappointed.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.