Every recession is preceded by an inverted curve, but not every one ends up in a recession

Outlook: We get November PPI today, likely again to 9% and core at 7.2% from 6.8% last time (consensus and Trading Economics estimate). Tomorrow it’s retail sales ahead of the Fed statement.

Everybody is building scenarios for the Fed and the economy next year, and thus the Fed’s responses. Anticipation is running high for the Fed’s forecasts and the dot-plot. At issue are inflation, whether wage gains feed inflation down the road, and growth rates, specifically whether the US goes into recession next year.

There is some fear the dollar has wrung all the gain it’s going to get out of the first rate hike—and that’s several months down the road! It might take inflation rising even further to restore the upswing, and that’s not likely—in fact, inflation is probably peaking this month and next. That will be visible especially in the month-over-month data, even if the year-over-year continues to frighten. We see inflation persisting well into the year, if not the whole year, but moderating to the 3.5-4% level. The freeing up of supply chains may well cause some precipitous oddball price drops, depending on how much buyers overbought inventory to be on the safe side. Wait for Christmas toy prices to crash in June. The wild card is wage growth, even though wage growth is hardly ever the primary source of inflation in the US—that would be commodity prices.

As for recession, that’s the wrong word. Once output catches up with demand, a slight drop in output is only to be expected and not the same thing as “recession” even if it permeates overall growth (especially jobs). It will be used to appeal to Fed doves, anyway. We confidently predict a fight between those who say the Fed tapering/hike should be limited, very limited, and those who want to ensure inflation goes down to 3.5% and stays there, if for the expectations component if not Fed reputation and credibility.

If this is how things develop and barring any Covid surprises, global growth resumes and that means we follow the leader, the Australian dollar. (And by the way, Australia reports employment data on Thursday and may validate the growth thesis.).

But thinking of Australia makes us think of China, and there we are not yet sure the Evergrande/property development sector debacle is going to get ended without a Crisis or any Shocks. On the western side of the Eurasian continent, Russia is trying to be a world player but is really only the 11th biggest country by GDP (see World Bank table). It was the 6th largest only a few years ago (2017). As often quoted, many US states (California, Texas, New York) have a bigger economy in GDP terms than Russia. The fun map is from the American Enterprise Institute in 2015 and for some reason excludes Russia. It’s not clear that size determines bellicosity, anyway, although it probably affects the duration of conflict. But becoming punier by the day only increases Putin’s need for affirmation and getting some territory back seems to be his first choice. You have to feel great pity for the Russian people. Anyway, a serious showdown over Ukraine (or anywhere else in the neighborhood) is a surefire promoter of the safe-haven dollar.

-637750861941287180.png)

Ah, but the yield curve is telling us not to expect global growth to resume. We don’t know where the bond gang is getting their insight from, but the problem is still with us—flattening everywhere. See the chart from the FT. While every recession is preceded by an inverted curve, not every inverted curve ends up in a recession. As the FT explains, the curve represents the collective wisdom of crowds and they see recession. Another idea is the inverted curve undermining confidence in the economy. Hmm, aka self-fulfilling prophecy. The FT ends with this gloomy observation: “The gap between 10-year and two-year US yields tightened in early December to its narrowest point in about a year, before investors had begun to price in a vigorous rebound in the economy.

“To some investors, this latest flattening is a sign that the Fed will only raise rates a small amount, given relatively modest growth prospects in the medium- to long-term. Others go further, arguing it is a sign that aggressive rate rises would be a ‘policy mistake’ that choke off economic growth and therefore leave the central bank needing to cut rates again.”

We have been calling this crowd the Gloomsters on the edge of a lunatic fringe, but we may have to retreat from that. Here’s the real problem—nobody ever really knows the medium to long term growth prospects. Period. They depend on a zillion things, including demographics, weather, technology, trends in education and climate change embrace, and these days, of course, the pandemic.

The only solid evidence we have in the US of a looming recession is that pesky quits rate. With millions of people leaving the workforce, the labor shortage will persist and the trend toward higher wages and salaries will persist, too. It wouldn’t take long for “wage-push inflation” to become a Thing, again. So the Fed could complete the tapering and do one hike, but intend to retreat once it has delivered the message “We fight inflation.” If wages don’t stop rising, it comes back for more. Can you get rising wages as growth falters? Yes, on the catching-up lag. The other thing you get with rising wages is more automation, and more flight to overseas producers.

All this seems a bit tangled. Don’t forget the revised Atlanta Fed GDPNow tomorrow, at 8.7% for Q4 last week. The Atlanta Fed almost always overshoots but still, the contrast of the projected growth rate with the flattening yield curve is confounding. Both things should not be happening at the same time. Either the yields should rise or the GDP forecast should fall. Economic modelling is imperfect, to be sure, but it seems as though modelling is delivering a suspiciously narrowing range of forecasts. The Philly Fed, for example, has 5.5% this year and 3.9% in 2022. The Conference Board has 5.0% for Q4 and 5.5% for the 2021 year with 3.5% in 2022. Goldman recently cut its forecast from 4.2% to 3.8% for 2022. Bottom line, 3.5-3.9% for 2022. This is hardly stagnation.

Our best guess is this year will be an anomaly whatever the number because of the lockdown, while next year will be a more normal 3.5-4.5%, whatever normal is. Note that since the 2008-09 financial crisis, growth in the US has hovered at under 4% and more often clustered around 2%, so a return to 3.5-4.5% is actually a net gain.

Given the perpetual deflation malaise in Japan and the perpetual slow-growth mode in Europe, that leaves the US, the UK and the CAD/AUD as the growth leaders. We do not see that ending. If currencies follow growth, we’re all right, Jack.

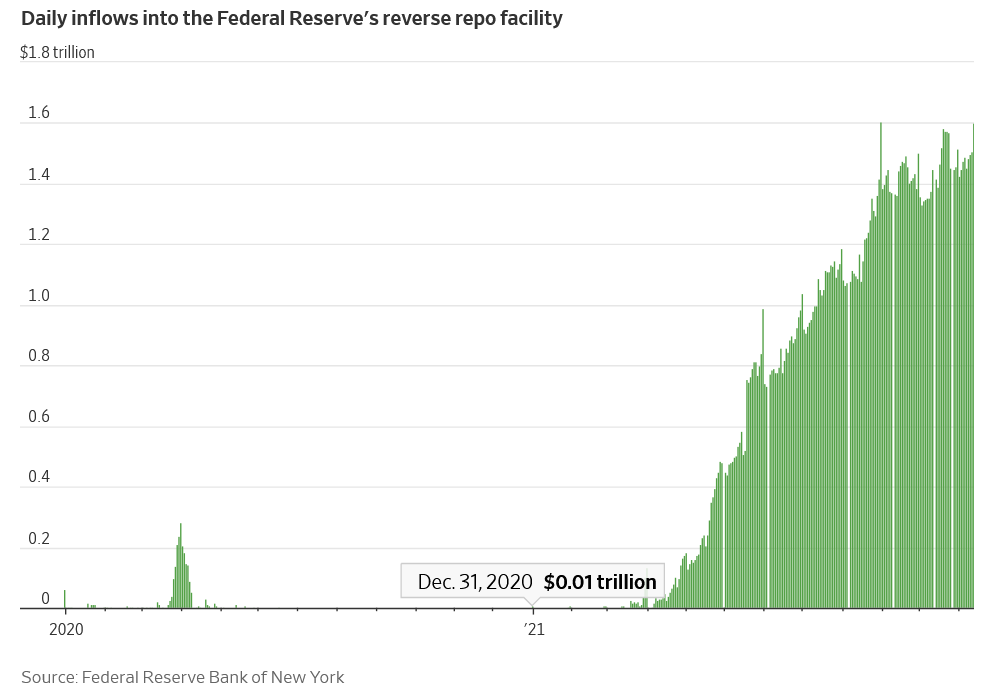

Fun Tidbit: The WSJ has a dandy story on the flood of European bank surplus cash flowing to the US repo market as year-end approaches. See the chart! Banks with excess cash have to pay to park it at the ECB (negative rates) while the Fed is paying 0.05%. “The yield on the benchmark two-year German government bond stood at minus 0.692% on Monday.”

But note the string of damning assertions: the Covid programs meant to boost lending has just “saddled banks with more cash than they can use.” One manager says “There’s so much money and not enough investments to be made.” In fact, “Last year, the ECB lowered the interest rates on its loans to as little as minus 1%, meaning banks got paid to borrow.” So, borrow at a negative rate, convert to dollars, and get 0.05% from the Fed.

Moreover, “The increased cost of converting euros to dollars is also an annual trend. It rises at the end of each year because the Basel Committee on Banking Supervision, a group of global central bankers and regulators, judges how systemically important a bank is through its year-end balance sheet, causing some banks to try to reduce their holdings to avoid higher capital charges, said Jerôme Legras, head of research at Axiom Alternative Investments.”

Does this flow to dollar have a lasting effect on the exchange rate? The analysts cited in the WSJ article say yes, but in practice, it’s not so clear, since the swap market by definition does not create any new positions. And it’s positioning that drives the spot prices. It’s a little interesting the European banks shun any markets closer to home, like the Hungarian 1-week at 2.90%.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat