Eurozone: Stabilisation but not yet a bottoming out

Recent business surveys suggest that the cyclical environment in the Eurozone, Germany and France is stabilising but it would be premature to call it a bottoming out. Such a positive development seems unlikely in the near term. Monetary policy is expected to remain tight for some time and part of the effect of the past rate hikes still needs to manifest itself. Bank lending policy is expected to remain cautious because of rising credit risk in a stagnating, high interest rates economy and credit demand from firms and households is weak. Significant progress in terms of disinflation seems to be a necessary condition for a lasting upturn in the economic outlook.

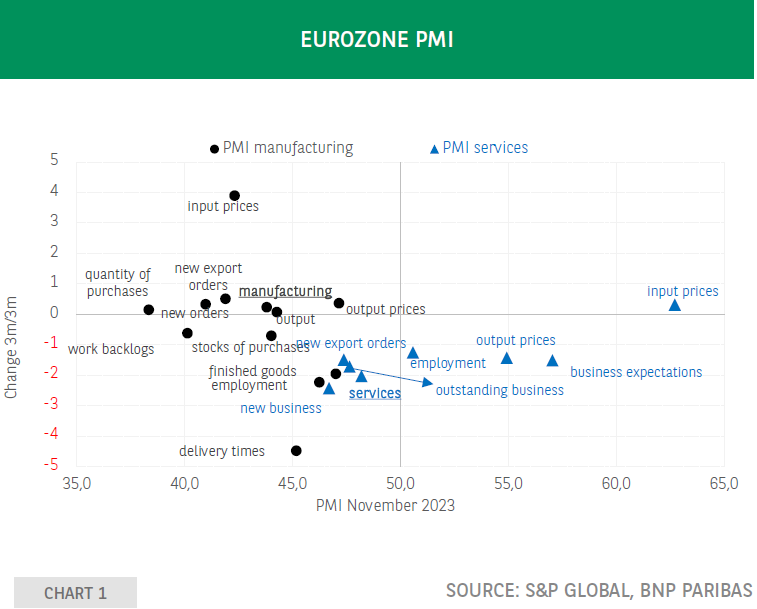

After the disappointing third quarter Eurozone GDP data a contraction of -0.1% versus the second quarter, recent business surveys have brought some relief. The Eurozone S&P Global composite flash PMI for the Eurozone improved slightly in November -from 46.5 to 47.1- on the back of better data for both manufacturing and services. When economic data have been on a downtrend, it is tempting to interpret the first sign of improvement as the start of a new uptrend. However, more is needed than one month of better data to be able to say that activity and demand are bottoming out. Looking at the average PMI for the past three months versus the previous three months, a stabilisation can be noted in manufacturing -the momentum is slightly positive but very close to zero- whereas momentum has been negative in the services sector (chart 1). In manufacturing, total as well as export orders have improved. However, the PMI employment data have weakened. This needs to be monitored closely considering the historical correlation between this series and Eurozone employment growth. In services, all series are weaker in recent months compared to before, except for input prices. This implies that news is concerning both on the activity and inflation front. France and Germany have also released business sentiment data recently. In the former, the INSEE business climate edged down from 98 to 97 in September it was still at 100 but this is masking strong divergences. The situation was stable in industry for a third consecutive month as well as in services. It weakened slightly in the construction sector whereas in retail trade the strong downtrend continued: since July this year, the index has lost 10 points, dropping from 106 to 96. In Germany, the ifo index improved in November for the third month in a row on the back of a better assessment of the current situation and expectations that were less pessimistic than before. Manufacturing saw a marked improvement, but the situation worsened slightly in services. Sentiment rose notably in trade and improved in construction.

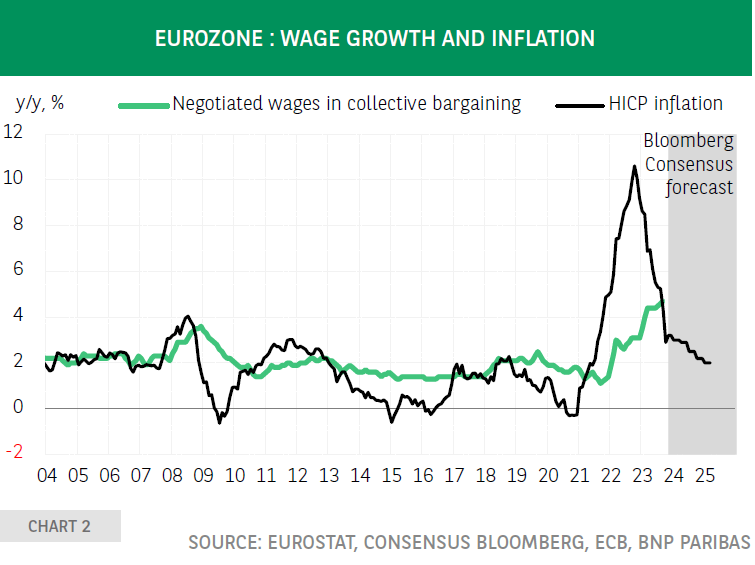

Although based on these data the case can be made that the cyclical environment in the Eurozone, Germany and France is stabilising, it seems premature to call it a bottoming out, because this would suppose that the situation is about to improve. Such a positive development seems unlikely in the near term. Monetary policy is tight and is expected to remain so for some time and part of the effect of the past rate hikes still needs to manifest itself. Bank lending policy is expected to remain cautious because of rising credit risk in a stagnating, high interest rates economy and, as showed by the latest ECB bank lending survey, credit demand from firms and households is weak. Survey participants expect this trend to continue in the current quarter, albeit at a slower pace. Uncertainty about the economic outlook may also push cash rich households and firms to adopt a more cautious stance, which could weigh on discretionary spending and investments. In the coming months, a genuine improvement in activity and demand will crucially depend on the outlook for official interest rates, which in turn will be driven by the inflation developments and prospects. Progress on disinflation should support the economy because it eases the pressure on the cost base of firms. Workers will benefit from the expected crossover between inflation and wage growth (chart 2): as the former drops below the latter, real wage growth increases, which should support consumer spending thereby raising confidence of firms. Finally, it will allow the ECB to provide guidance that the terminal rate has been reached, thereby eliminating lingering concerns of economic agents that rates would move higher still. Significant progress in terms of disinflation seems to be a necessary condition for a lasting upturn in the economic outlook.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.