EUR/USD 2022 Forecast: Policymakers will continue to chase inflation and King Dollar will make the best out of it

- Central banks will be forced into action in 2022, but will it be worth it?

- Sentiment seesaws between fears and hopes related to the pandemic.

- EUR/USD at a brink of a long-term bearish breakout, 1.0635 exposed.

Much water has run under the bridge in 2021, and as usual, the dollar made the most out of it in these tumultuous times. The greenback is ending the year on a strong note, compliments to the US Federal Reserve’s decision to kick-start tapering.

The US central bank is not alone in its tightening path, however, nor has it been the first, for a change. The Canadian and New Zealand central banks were the first to announce measures, while the Reserve Bank of Australia took a Lil step forward, and the Bank of England is menacing to make a move. On the other hand, the European Central Bank is among the laggards – those that are still in wait-and-see mode.

Understanding EUR/USD behavior

Joe Biden became the 46th US President on January 20, 2021, replacing Donald Trump. You may love him or hate him, but there are no doubts Trump was much more fun for financial markets, leaking reports, taking abrupt and unexpected decisions, and overall, spurring volatility.

Biden not only offered the Treasury Secretary to Janet Yellen but also nominated Federal Reserve Chair Jerome Powell for a second term, meaning we will have Powell for another four years. Biden cited the “decisive action” taken by Powell during the early stages of the pandemic crisis as a reason to reappoint him.

The coronavirus pandemic that hit the world in March 2020 still goes on, although there’s a better economic perspective. Vaccine rollout brought hope alongside the economic comeback. But there is no chaos without a butterfly effect. Reopenings and overall, the path towards “normal” unexpectedly sent prices to multi-decade highs across the world. Supply chain issues, as the global machine slowly geared up, became much steeper than anticipated. Consumer demand or hopes for higher demand outpaced supply, with no end and sight for such a situation.

Gas prices skyrocketed as the OPEC+ was utterly conservative in unwinding record production cuts. Back in 2020, the organisation slashed output by roughly 10 million bpd or 10% of global supply scaling back to about 3.8 million bpd throughout the year. In their latest meeting, they decided to increase output in January 2021 by 400K bpd. Producers had regularly failed to meet their output targets, however, delivering roughly 700K bpd less than planned in September and October.

Grappling with the challenges

In a desperate attempt to bring down oil prices, US President Biden released 50 million oil barrels from the Strategic Petroleum Reserve in November, but like the Fed, it seems to be doing too little too late. Still, oil prices are just a piece of the puzzle.

Central bankers from around the world have been cooling down speculation on persistently high inflation, calling in “temporarily,” and forecasting it would slowly stabilize to more suitable levels by 2022.

But make no mistake: Hot inflation is the elephant in the room. It took the US Fed pretty much the whole year to finally take note of price pressures, while European policymakers remain in denial, saying high levels of inflation are only high “temporarily.”

The lady isn’t tapering

European Central Bank President Lagarde insists that she sees inflation rising "in the near term, but then declining in the course of next year." Back in July, the ECB’s forward guidance established three conditions that need to be satisfied before rising rates, which have not been met so far.

“The Governing Council will not consider raising rates unless three conditions have been met: first, we need to see inflation reaching two per cent well ahead of the end of the projection horizon; second, after convergence, inflation should be seen to be stabilising durably at the target through the end of the projection horizon; and third, realised progress in underlying inflation should, in our judgement, be sufficiently advanced to be consistent with inflation stabilising at two per cent over the medium term.”

A light of hope surged in September, as the central bank decided favourable financial conditions could be maintained with a moderately lower pace of net asset purchases under the Pandemic Emergency Purchase Program (PEPP) than in the previous two quarters. Lagarde noted that such a reduction didn’t amount to a “tapering” but was instead a mere “recalibration.” PEPP purchases would continue until at least the end of March 2022 with a total envelope of €1.85 trillion.

Heading into the final meeting of the year, Lagarde maintained its caution stance. “Despite the current inflation surge, the outlook for inflation over the medium term remains subdued, and thus these three conditions are very unlikely to be satisfied next year." At the same time, ECB Vice-President Luis de Guindos noted that “the current higher phase of inflation could last longer than earlier thought,”

Inflation, inflation, inflation!

In contrast to the ECB’s “recalibration,” the US Federal Reserve kick-started tapering its pandemic-related asset purchase program. In their November meeting, US policymakers noted that the economic recovery was enough to start rolling back financial support. Officials also expressed concerns about how long inflation would remain elevated. The amount of bond-buying was reduced by $15 billion per month, $10 billion in Treasuries and $5 billion in mortgage-backed securities.

Despite their optimism, policymakers were clearly concerned about price pressures. During the press conference offered post-decision, Powell admitted that inflation was the main theme discussed.

Chair Powell and Treasury Secretary Janet Yellen testified on the CARES act before the Senate early in December and surprised markets. They said that it was about time to remove the word “transitory” to describe inflation and announce they would discuss speeding up bond-buying tapering in the Fed’s December meeting. There is still no consensus on when the US central bank will hike rates, but market participants understand that faster tapering means a sooner hike. They also anticipated the central bank would discuss speeding up tapering in their December meeting, with the market rushing into pricing in a reduction of $30 billion per month.

Source: Reuters

How much have economies progressed?

Central bank mandates rotate around keeping inflation under control. For the US, it also implies maximum employment.

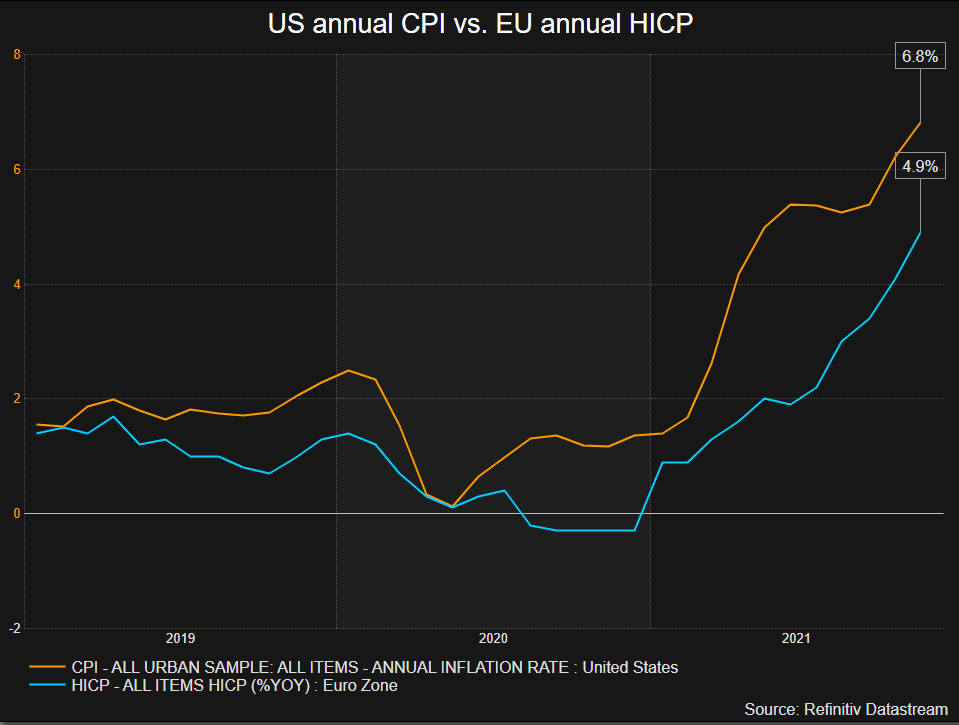

Maintaining price stability has been a lost challenge in 2021. The euro area annual inflation rate was 4.1% in October 2021, up from 3.4% in September, the highest rate of inflation since July 1991. In the US, the annual inflation rate soared to 6.2% in October, the highest since November 1990.

Regarding employment, “the EU economy and labour market have started to recover from the COVID-19 pandemic with employment and unemployment at almost pre-crisis rates,” according to the European Commission report on Employment and Social Developments Quarterly Review from September 2021. Eurostat estimates that 14.312 million men and women in the EU, of whom 12.045 million in the euro area, were unemployed in October 2021.

Across the Atlantic, the US has managed to add 210K new jobs in November 2021, which means it’s still roughly 4 million positions short of pre-pandemic levels. The number of persons not in the labor force who currently want a job was 5.9 million, according to November stats.

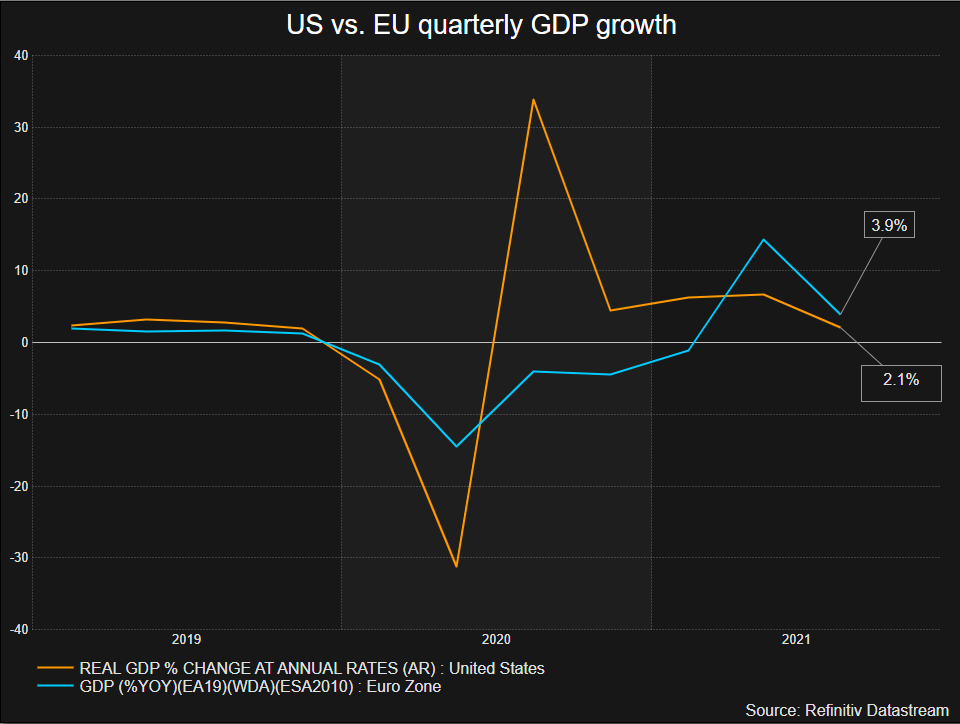

Nevertheless, US economic progress was faster through the first half of the year, while the pace of the recovery in Europe picked up in the second and third quarters. A faster pace of vaccination and a larger fiscal stimulus - in absolute terms and relative to other countries - skewed the scale in the US’s favor.

The US has grown at an annual 4.9% pace in the third quarter of 2021, while the EU economy expanded by 3.7% in the same period. Still, numbers do not reflect how uneven the recovery from the COVID-19 crisis has been so far.

Source: Reuters

The loose end

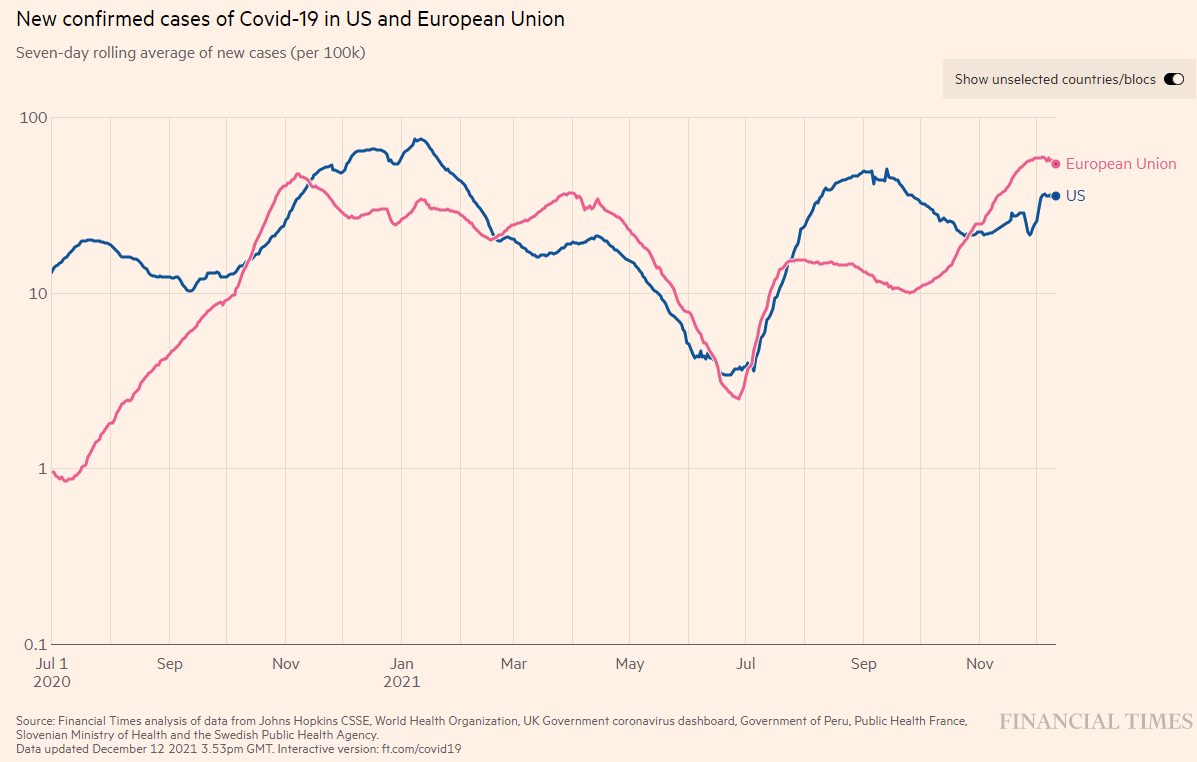

And here comes COVID-19. The pandemic is far from over, despite global efforts. The world is learning to live with the virus, but new strains appear every so often challenging progress. Vaccines have helped reduce hospitalisations and deaths dramatically, and the Bloomberg covid tracker reports that more than 8.3 billion shots have been given so far. However, and according to the same report, countries and regions with the highest incomes are getting vaccinated more than ten times faster than those with the lowest.

Uneven access to vaccines has resulted in the discovery of the latest Omicron strain that’s storming the world heading into 2022. There is loads of uncertainty around it, but so far, it’s clear that it is much more contagious, putting governments and market players on their toes.

The one lesson learned through 2021 is that lockdowns and travel restrictions do little to prevent the spread. The economic halt experienced earlier in 2020 has become a huge drag for economic progress that continues up to these days and will likely keep taking its toll through at least the first half of 2022.

Speculation mounts about the Omicron variant being less deadly, spurring hopes that it will become the beginning of the end of the pandemic, as it fits into the pattern of virus evolution observed historically. One thing is for sure, the coronavirus is here to stay, although when it will turn into an endemic illness is still a mystery.

As long as the market fears a new strain could result in restrictive measures delaying the economic comeback, sentiment-related trading will prevail.

Where are central banks heading?

On Wednesday, December 15, the US Federal Reserve announced its monetary policy decision, while the European Central Bank revealed its conclusions on the same matter on Thursday, December 16. Both took tapering-related measures to tame stubbornly high inflation but failed to impress market participants.

The Fed increased the reduction in bond-buying on a monthly basis to $30 billion, from $15 billion as announced in November, starting January 2022. That means the central bank will stop buying $20 billion Treasuries and $10 billion Mortgage-Backed Securities per month, which means sooner rate hikes. The Fed’s dot-plot now implies three rate hikes in 2022 and three more in 2023.

The inflation forecasts have been raised to 5.6% for 2021 and 2.6% for 2022, up from 4.2% and 2.2% previously. In addition, the Gross Domestic Product is now projected AT 4% in 2022, up from the previous median forecast of 3.8%, while the economy is estimated to grow 2.2% in 2023, down from the 2.5% from September.

The ECB confirmed it will end the Pandemic Emergency Purchase Program on March 2022 as previously anticipated. The Government Council also decided to expand its Assets Purchase Program to €40 billion per month in the second quarter of 2022 and to €30 billion in the third quarter of the year, to partially compensate the end of the monthly €60 billion bond-buying through PEPP.

The central bank now foresees inflation increasing from 2.6% this year to 3.2% the next one. But it said price growth would then fall to hit 1.8% cent in 2023 and stay at that level in 2024 while lowering growth forecast in 2022 to 4.2% from 4.6% previously.

The one thing that these central banks have in common is that they are not dealing with the reasons but with the consequences. Rates will have to go really high from their current levels to significantly impact inflation unless the world finally overcomes the pandemic crisis and bottlenecks resolve themself.

EUR/USD technical outlook

The EUR/USD pair started the year trading at 1.2239 and traded as low as 1.1185 in November. It’s heading into the yearly close, trading much closer to the 2021 low than to the peak of 1.2349 from January. Back in March 2020, when the crisis started, the pair bottomed at 1.0635.

Drawing a Fibonacci retracement from the March 2020 low to January 2021 high, the 61.8% retracement comes in at 1.1288. The fact that the pair is currently struggling around it fuels speculation of a possible bearish breakout that may extend to the bottom of the mentioned range.

The monthly chart shows that EUR/USD broke above a long-term descendant trend line coming from the historical high at 1.6036 at the end of 2020. It completed a pullback to the line in November and spent most of this December struggling around it. The trend line is not far from the mentioned Fibonacci level, further reinforcing the idea that a yearly close below it could mean a bearish 2022.

The pair has been falling pretty much in a straight line since May this year and is technically oversold. However, that does not prevent it from resuming its slump. Some consolidation around the current levels could be expected, yet a break below 1.1200 would confirm the bearish route, at least for the first quarter of 2022.

The picture can change, but the road up is tough. A long-term static resistance area comes in at around 1.1460/70, while the 38.2% retracement of the monthly rally is located at 1.1691. A recovery above the latter could put EUR/USD in the way towards 1.2000 and then 1.2400.

However, and for the time being, there are no technical signs that the shared currency could make a substantial comeback. The pair is developing below all of its moving averages in the monthly and weekly charts, while technical indicators on the same time frames are flat to bearish within negative levels. In both charts, some technical indicators are flirting with oversold readings. Yet again, such conditions could dilute with continued consolidation or short-lived corrective advances.

King Dollar is poised to maintain its advantage against most major rivals, EUR included.

Gregor Horvat projects a bearish continuation for EUR/USD in his Elliott Wave analysis:

EUR/USD Elliott Wave Analysis

EURUSD came lower in 2021 so price action remains trapped in a big sideways price action that belongs to a bearish trend that is in play since 2008. Ideally, it’s a triangle that can cause more weakness in second part of 2022. Ideally the multi-year low will be printed around parity.

Forecast Poll 2022

| Forecast | Q1 - Mar 31st | Q2 - Jun 30th | Q4 - Dec 31st |

|---|---|---|---|

| Bullish | 16.1% | 18.9% | 21.6% |

| Bearish | 51.6% | 51.4% | 34.2% |

| Sideways | 32.3% | 29.7% | 44.7% |

| Average Forecast Price | 1.1306 | 1.1278 | 1.1264 |

| EXPERTS | Q1 - Mar 31st | Q2 - Jun 30th | Q4 - Dec 31st |

|---|---|---|---|

| Alberto Muñoz | 1.0900 Bearish | 1.0750 Bearish | 1.0600 Bearish |

| Andrew Lockwood | 1.1200 Sideways | 1.1000 Bearish | 1.0800 Bearish |

| Andrew Pancholi | 1.1490 Sideways | 1.1675 Bullish | 1.2100 Bullish |

| ANZ FX Strategy Team | 1.1300 Sideways | 1.1300 Sideways | 1.1500 Sideways |

| Barclays | 1.1600 Bearish | 1.1700 Bullish | 1.1900 Bullish |

| BMO Capital Markets Team | 1.1200 Sideways | 1.1100 Sideways | 1.1200 Sideways |

| BNP Paribas Team | 1.1200 Sideways | 1.1000 Bearish | |

| BoA FX Rates & Commodities | 1.1300 Sideways | 1.1200 Sideways | 1.1000 Bearish |

| Brad Alexander | 1.0900 Bearish | 1.0700 Bearish | 1.0600 Bearish |

| Brian Wang | 1.1700 Bullish | 1.1460 Sideways | 1.1540 Sideways |

| CIBC World Markets Team | 1.1300 Sideways | 1.1200 Sideways | 1.1000 Bearish |

| CitiFX | 1.1100 Bearish | 1.1200 Sideways | 1.1200 Sideways |

| Commerzbank Analyst Team | 1.0900 Bearish | 1.0800 Bearish | |

| DBS Group Research | 1.1100 Bearish | 1.1000 Bearish | 1.1000 Bearish |

| Eren Sengezer | 1.1400 Sideways | 1.1000 Bearish | 1.1000 Bearish |

| Francesco Bergamini | 1.2000 Bullish | 1.2200 Bullish | |

| Frank Walbaum | 1.1500 Sideways | 1.1200 Sideways | 1.1000 Bearish |

| Gil Ben Hur | 1.1500 Sideways | 1.1700 Bullish | 1.1900 Bullish |

| Goldman Sachs | 1.1400 Sideways | 1.1600 Sideways | 1.1800 Bullish |

| ING Global Economics Team | 1.1500 Sideways | 1.1400 Sideways | 1.1000 Bearish |

| Ivan Cummins | 1.1500 Sideways | 1.1200 Sideways | 1.0900 Bearish |

| JP Morgan | 1.0900 Bearish | 1.1000 Bearish | |

| Matias Salord | 1.1445 Sideways | 1.1215 Sideways | 1.1100 Sideways |

| Murali Sarma | 1.1075 Sideways | ||

| NAB Global Markets Research | 1.1600 Bullish | 1.1700 Bullish | 1.2000 Bullish |

| NatWest Markets | 1.1200 Sideways | 1.1700 Sideways | |

| Navin Prithyani | 1.1300 Sideways | 1.1500 Sideways | 1.0500 Bearish |

| Nenad Kerkez | 1.0898 Bearish | 1.0975 Bearish | 1.1215 Sideways |

| Nomura FX Research & Strategy | 1.1100 Bearish | 1.1300 Sideways | 1.1700 Sideways |

| Rabobank Financial Markets | 1.1300 Sideways | 1.1300 Sideways | 1.1200 Sideways |

| RBC Economic Research Team | 1.1200 Sideways | 1.1300 Sideways | 1.1400 Sideways |

| Societe Generale Analyst Team | 1.1300 Sideways | 1.1100 Sideways | |

| Standard Bank Research Team | 1.1700 Bullish | 1.1800 Bullish | 1.1400 Sideways |

| UniCredit Research | 1.2000 Bullish | 1.2100 Bullish | 1.2200 Bullish |

| Usman Ahmed | 1.1054 Bearish | 1.0926 Bearish | 1.0796 Bearish |

| Wells Fargo Research Team | 1.0900 Bearish | 1.0800 Bearish | 1.0700 Bearish |

| Westpac Instituional Bank Team | 1.1100 Bearish | 1.0900 Bearish | 1.1000 Bearish |

| Yohay Elam | 1.1000 Bearish | 1.1600 Sideways | 1.1900 Bullish |

We see continued USD weakness in 2021 and diversification into EUR's from real money managers rhough 2021. The USD index as a whole should bounce in the 1st quarter 2021, however the EURUSD should trend to the high 1.20's as long as 1.1900 level holds.

by Blake Morrow

A harsh covid winter may set the old continent back but by the summer, things will markedly improve. The German elections could cause the rally to pause in the autumn.

by Yohay Elam

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.