“Crosscurrents” and the Outlook for Fed Policy

Executive Summary

Federal Reserve Chairman Powell noted that there were "crosscurrents" that were impacting the U.S. economy when he discussed the outlook for monetary policy at the conclusion of the January 30 meeting of the Federal Open Market Committee (FOMC). Exports and the housing market are exerting some headwinds on growth at present and business fixed investment is moving more or less sideways, but consumer and government spending are both growing at strong rates. The FOMC has said that it can be "patient," and most market participants currently believe that the Fed is done hiking rates.

We agree that the FOMC likely will remain on hold in coming months as it assesses the outlook for the U.S. economy, but we think it would be premature to claim that this Fed tightening cycle is now over. If, as we forecast, the economy continues to grow at an above-trend rate in coming months, then we look for the FOMC to tap on the brakes again with a 25 bps rate hike this summer or in the early autumn.

Is the Fed Really Done Hiking Rates?

At his press conference following the January 30 meeting of the FOMC, Chairman Jerome Powell noted that there were "crosscurrents" that were impacting the U.S. economy at present. Given the noticeably dovish tone to the FOMC statement, which was reinforced by Powell's press conference comments, financial markets are currently priced for no further rate hikes in this cycle. Have the "crosscurrents" that Powell referenced caused the economy to slow enough to remove the need for further rate hikes or will the FOMC eventually resume tightening? Could the next move in the Fed's policy rates be a cut? In an effort to answer these questions, we will discuss different spending categories in this report to determine how the overall U.S. economy is faring at present and the implications of that analysis for the outlook for Fed policy.

Swimming Against the Current

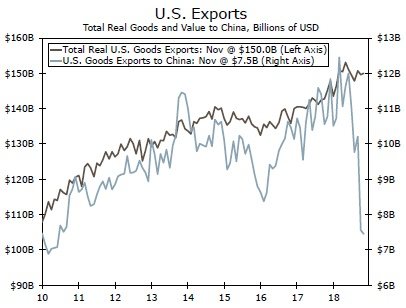

There are some spending categories that are swimming against the current at present. Start with the foreign sector. The value of American exports to China has nosedived in recent months due to the one-two punch of slower economic growth in China combined with Chinese tariffs on American goods (Figure 1). China accounts for only 8% of total U.S. exports, so the collapse in U.S. exports to China has not been replicated in the total. Nevertheless, total real exports of goods have been more or less flat in recent months (Figure 1). In other words, the contribution to U.S. economic growth from real exports has weakened recently.

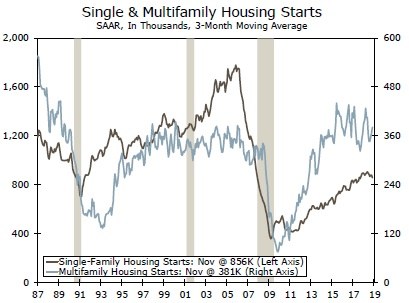

The housing market also appears to be swimming against the current at present. Multifamily housing starts have been choppy but they have been more or less flat on balance for some time, while single-family starts have rolled over recently (Figure 2). The rise in mortgage rates and the marked increase in home prices in many parts of the country over the past few years have eroded affordability. Spending on real residential construction fell 2.1% between Q4-2017 and Q3-2018, and we project that residential construction contracted again in the fourth quarter.

That said, we look for some eventual turnaround in these spending categories. Although foreign economic growth has decelerated, we expect that most foreign economies will avoid an outright recession. We also anticipate that the United States and China will reach an agreement within the next month or so on a trade deal or, at a minimum, trade tensions between the world's two largest economies will not escalate further. Consequently, real exports of goods and services in the United States should trend higher in coming quarters, albeit at a modest rate of growth. Likewise, wwhich account for roughly one-third of total residential investment, continue to grow

at a solid rate.1e look for some uptick in residential construction in coming quarters. The rate on the 30-year fixed-rate mortgage has declined half a percentage point since mid-November, which has contributed to a rebound in mortgage applications so far this year. Furthermore, improvements to the existing housing stock, which account for roughly one-third of total residential investment, continue to grow at a solid rate.1

Swimming Across the Stream

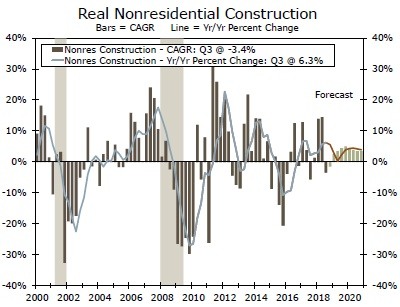

The nonresidential construction sector has had a mixed performance in recent quarters. Spending in this sector was very strong at the beginning of 2018 (Figure 3). High oil prices in the first half of the year led to rapid growth in investment in the energy sector. (Spending on structures in the energy sector shows up in the nonresidential construction component of the GDP accounts.) But, nonresidential construction contracted more than 3% at an annualized rate in Q3-2018, and we estimate that it slid a bit further in the fourth quarter. That said, we look for further gains in this sector, albeit at a modest pace, in coming quarters. Construction in the industrial sector, which includes warehouses, should remain strong, and we also look for modest rates of growth in offices and hotels.

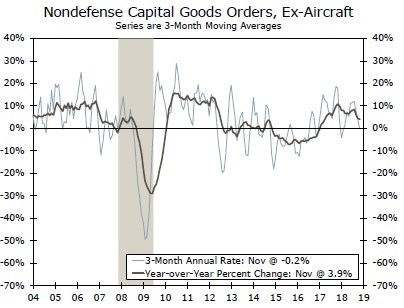

Growth in other areas of business investment spending has also softened recently. Real spending on equipment was robust in the second half of 2017 and early in 2018. However, growth in this category of spending downshifted to only 3.4% at an annualized rate in Q3-2018. New orders for non-defense capital goods (excluding aircraft), which is a leading indicator of real equipment spending, have decelerated significantly in recent months (Figure 4). Perhaps uncertainty related to trade policy is contributing to the recent slowdown in equipment spending. But whatever the catalyst(s), the near-term outlook for business spending on equipment does not look very strong. That said, sustained declines in business spending on equipment do not appear to be likely. As noted above, we look for some de-escalation of trade tensions with China in the next few months. Moreover, spending on intellectual property products (IPP), which accounts for one-third of total business fixed investment spending, has been growing strongly in recent quarters.2

Swimming With the Current

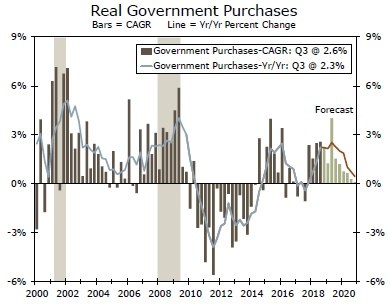

The categories of spending discussed above are either exerting some headwinds on the rate of real GDP growth in the United States or they are not adding much momentum at present. Fortunately, there are two spending categories, one relatively small but one large, that are growing at solid rates. Let's start with government spending, the smaller of the two categories, which was up 2.3% on a year-ago basis in Q3-2018 (Figure 5). Congress increased federal government spending significantly as part of the budget agreement in February 2018. Although the positive impulse to real GDP growth from federal spending appears to be close to peaking, we estimate that government spending will continue to make positive contributions to growth, albeit at diminishing rates, through the end of 2020.

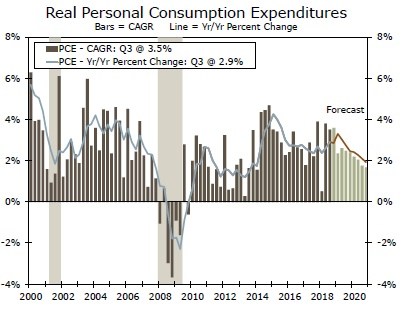

Personal consumption expenditures (PCE), which comprise two-thirds of GDP, have grown at a robust rate in recent quarters (Figure 6). Employment growth has been strong and wages have accelerated. Both of these developments have generated meaningful growth in real income, which has underpinned the heady growth rates of real PCE that have been registered recently.3 Furthermore, the personal tax cuts that took effect in early 2018 provided a boost to real disposable income for many households. Looking forward, we forecast that growth in real PCE will downshift a bit as the effects of the tax cuts start to wear off. But we expect that growth in real PCE will generally remain solid in coming quarters as strong growth in employment continues to support growth in real income.

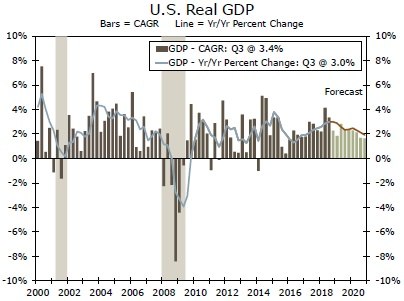

So where does all this leave us? We estimate that U.S. real GDP rose 3.0% on a year-ago basis in Q4-2018. Although we look for some deceleration in 2019—we forecast that the year-over-year rate of real GDP growth will slow to 2.4% by Q4—we expect that the expansion will remain intact (Figure 7).4 Not only is our GDP forecast for 2019 more or less in line with the FOMC's forecast, but it is above the FOMC's estimate of the long-run potential growth rate.5

How Will the FOMC Navigate the "Crosscurrents"?

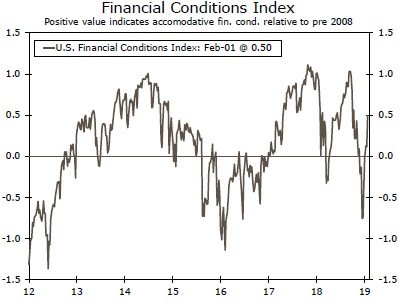

The FOMC hiked rates on December 19, and Chairman Powell suggested in his post-meeting press conference that more tightening was likely. With many economies showing signs of deceleration and with plenty of other economic policy uncertainty at the time, financial market participants were not pleased with the hawkish tone of the Fed. As shown in Figure 8, the Bloomberg financial conditions index tightened significantly at the end of last year (a movement lower in the index indicates that financial conditions have tightened). Not only did the stock market swoon, but corporate bond spreads widened markedly. If sustained, a tightening in overall financial conditions could lead to slower economic growth.

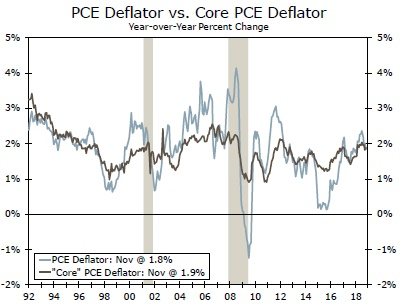

The FOMC decided to keep its target range for the fed funds rate unchanged at its January 30 policy meeting, which was universally expected. Moreover, the committee indicated that it will be "patient" as it contemplates its next move. Because rates of PCE inflation are currently near the Fed's target of 2% and showing few signs of moving higher at this time (Figure 9), the FOMC can afford to take a wait-and-see approach.

But we think it would be premature to claim that this Fed tightening cycle is now over, as is currently indicated by financial prices. For starters, financial conditions have relaxed since the turn of the year, which improves the growth outlook, everything else equal. Moreover, as outlined above, the expansion seems likely to continue, which the FOMC acknowledged on January 30.6 We agree that the FOMC likely will remain on hold in coming months as it assesses the economy. But if the economy continues to grow at an above-trend pace, which would cause the unemployment rate to recede further, then we think the FOMC will decide to bump rates up again 25 bps in late summer/early autumn. We then look for the committee to remain on hold through most of 2020 as the economy slowly loses momentum, and we forecast that conditions will be in place to induce the FOMC to start cutting rates at the end of 2020.

Conclusion

Many financial market participants seem to think that the FOMC is done hiking rates in this cycle. Although we agree that the committee likely will be on hold for the foreseeable future, we think it is premature to declare an end to the tightening cycle. Financial conditions, which tightened considerably at the end of last year, have eased in recent weeks. There clearly are some "crosscurrents" which are impacting the U.S. economy at present, but on balance the economy appears to be swimming with the current. If, as we forecast, the economy continues to grow at an above-trend rate in coming months, then we look for the FOMC to tap on the brakes again with a 25 bps rate hike this summer or in the early autumn.

Author

Wells Fargo Research Team

Wells Fargo