Congress unleashes the fiscal firehose

Executive Summary

Last night, the U.S. Senate passed a landmark fiscal bill designed to keep the U.S. economy afloat amid the drastic measures taken to combat COVID-19. The vote was unanimous, a testament to the severity of the public health and economic crisis facing the country. If the House of Representatives can also manage to swing a unanimous vote, then passage of the bill should be swift, likely within a day or so. If the members have to be called back to Washington D.C. for a full vote, however, the bill may not pass until early next week. Regardless, we expect final passage in the near future, and for the president to quickly sign it into law once it is through Congress.

The United States economy is facing an unprecedented shutdown of economic activity, but this slowdown is being met with unprecedented monetary and fiscal stimulus, both in terms of size and speed. Although we do not yet have an official score from the Congressional Budget Office, the bill currently working its way through Congress appears to be about $2 trillion in size, or roughly 9% of U.S. GDP. But, even this may understate the true size of the package. Our understanding is that roughly $454 billion of that money will be used as an equity infusion into a Federal Reserve 13(3) emergency lending program designed to lend directly to ‘Main Street', e.g. businesses, states and municipal governments. Assuming the Fed uses the equity to lever up about ten times, that would generate more than $4 trillion in lending power, bringing the potential total size of the package up to a stunning $6 trillion.

In this report, we first walk through a summary of some of the key parts of the bill. Then, we analyze what we think it means for the U.S. economy and the federal budget deficit. In short, the passage of this fiscal stimulus bill gives us reasonable confidence that another Great Depression is not in the cards, and that a healthy bounce back in economic growth will occur starting this fall. But, even these extraordinary measures can only do so much, and in our view the economic contraction in the months ahead will still be quite severe. This is not to say the policies are ill-designed, but rather that until the COVID-19 outbreak is in check, fiscal and monetary policymakers are just buying time until the economy can begin to operate normally again. Our latest federal budget deficit forecasts for FY 2020 and FY 2021 are $2.4 trillion and $1.7 trillion, respectively. If realized, the FY 2020 federal budget deficit would be the biggest deficit as a share of the economy since World War II.

Household Policies

On the household front, the cornerstone policy is a plan to send checks directly to individuals. The cash payments would be $1,200 for individuals making $75,000 or less and $2,400 for couples making $150,000 or less, plus a $500 per child bonus. The payments are slowly phased out past those income levels, with rebates not available above the $99k/$198k threshold for single and married filers, respectively. Ultimately, eligibility will be determined by a taxpayer's 2020 income. But, since this is not yet known, the government will use 2019 tax data, and where this is not available, 2018 tax data. In total, these rebates would cost roughly $300 billion. Paired with this would be a boost to unemployment benefits so that payments are larger (an extra $600 per week for four months), more expansive (e.g. it would include furloughed workers) and can be collected for longer (thirteen weeks past when state unemployment benefits run out). Although more uncertain, this segment of the bill could end up costing another $200-$300 billion.

The bill pushes the tax filing deadline of April 15 back to July 15, and waives the 10-percent early withdrawal penalty for distributions up to $100,000 from qualified retirement accounts for coronavirus-related purposes. Income attributable to such distributions would be subject to tax over three years. The bill also waives required minimum distribution rules for certain defined contribution plans and IRAs for calendar year 2020.

Small Business Policies

At a high level, the small business relief in the bill attempts to make Small Business Administration (SBA) loans available to businesses in a way that, if the money is used for certain purposes, such as keeping workers on the payroll or making mortgage payments, the loans will eventually be forgiven. Specifically, the bill contains $350 billion to provide cash-flow assistance through 100 percent federally guaranteed loans to employers who maintain their payroll during this emergency. If employers maintain their payroll, the loans would be forgiven, which would help workers remain employed and affected small businesses quickly snap-back after the crisis. Businesses with 500 employees or fewer will be eligible to apply for the loans, unless the applicable size standard for the industry as provided by SBA is higher. The size of the loans would be tied to an applicant's average monthly payroll, mortgage/rent, utility payments and other debt obligations over the previous year. The maximum loan amount would be $10 million.

Corporate Policies/Federal Reserve Lending Facility

Generally speaking, the rescue package for larger corporations takes the form of more traditional loans. The bill contains $500 billion for such measures, with $46 billion directed specifically at three industries: passenger air carriers ($25 billion), cargo air carriers ($4 billion) and $17 billion for "businesses important to maintaining national security". The remaining $454 billion would be "for loans, loan guarantees, and investments in support of the Federal Reserve's lending facilities to eligible businesses, states, and municipalities."

Our understanding is that this $454 billion would be used as an equity infusion into a Federal Reserve 13(3) lending facility designed to lend directly to businesses and other non-bank entities. Critically, when the Federal Reserve sets up these 13(3) lending programs, it typically takes an equity infusion from the federal government (often from the Exchange Stabilization Fund) and then uses that equity cushion to lever up. Based off of other 13(3) lending programs, as well as comments from lawmakers over the past few days, we believe that the Federal Reserve would take this money and generate more than $4 trillion in direct lending power.

The bill also relaxes the limitations on a company's use of losses to improve cash flow and liquidity. Net operating losses (NOL) were limited as part of the Tax Cuts and Jobs Act, and at present they cannot be carried back to reduce income in a prior tax year. The bill provides that a net operating loss arising in 2018, 2019, or 2020 can be carried back five years. The bill also temporarily removes the taxable income limitation to allow an NOL to fully offset income. In addition, the bill would temporarily increase the amount of interest expense businesses are allowed to deduct on their tax returns, by increasing the 30-percent limitation to 50 percent of EBITDA for 2019 and 2020.

Miscellaneous Policies

While far from an exhaustive list, below are a few more key items included in the bill.

-

Suspend federal student loan payments for six months, with no accruing interest.

-

Allow businesses to defer payments of the employer side of the Social Security payroll tax.

The deferred employment tax would be paid over the following two years, with half of the amount required to be paid by December 31, 2021 and the other half by December 31, 2022. -

Give depository institutions the option to temporarily delay measuring credit losses on financial instruments using the new Current Expected Credit Losses (CECL) accounting standard.

-

Authorize a slew of supplemental appropriations for federal agencies/programs, hospitals, and state and local governments, among others.

This portion of the bill contains roughly $340 billion in funding, including $117 billion for hospitals and veterans' health care, $45 billion for the federal emergency management administration (FEMA), $30 billion for K-12 and higher education, $25 billion for public transportation emergency relief and $25 billion for child nutrition and the supplemental nutrition assistance program (SNAP).

What Does This All Mean?

The traditional Keynesian stimulus solution to an economic slowdown is for fiscal stimulus to boost aggregate demand. For example, increasing infrastructure spending creates jobs for individuals who can then take their newfound income and spend it on a variety of goods and services, thus boosting aggregate demand in the economy. While this is the goal of this bill to some extent, the current slowdown is unique in nature. Several segments of the economy are shut down, and huge swaths of the U.S. population are confined to their homes, making increased consumption and investment nearly impossible in some sectors. Thus, this fiscal package is designed to achieve a somewhat different goal: keep households, businesses and municipalities liquid and solvent through a temporary, though severe, crunch so that the economy can bounce back strongly on the other side of the virus outbreak.

To that end, this bill should help plug some of the sizable hole in lost income that is developing as a result of measures taken to stem the spread of COVID-19. As we discussed in a recent research note, total U.S. income is approximately $900 billion per month, and the combination of direct checks to households, expanded unemployment benefits, grants/loans to various levels of government and generous loans to U.S. companies should help ease what is likely to be a significant decline in U.S. total income. This in turn should help many households and businesses remain current on their financial obligations for the next couple months.

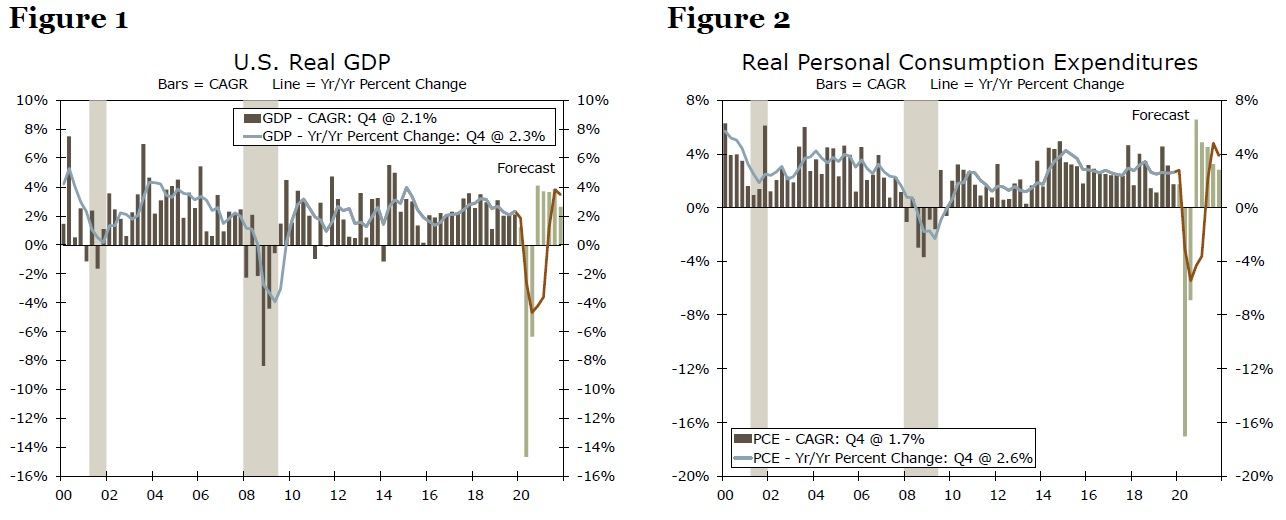

But, this fiscal stimulus is not a panacea. The household measures should help for a time, but the longer the COIVD-19 shutdown is in effect, the less these temporary boosts to personal income will be able to keep households afloat. And while in principal the small and large business lending programs should provide much needed liquidity and solvency, the usual lag in policy implementation, combined with the untested nature of these programs, raise questions about their ultimate efficacy in a period of rapid economic change. This is not to say the policies are illdesigned, but rather that until the COVID-19 outbreak is in check, fiscal and monetary policymakers are just buying time rather than solving the true underlying problems. In sum, the passage of this bill gives us reasonable confidence that another Great Depression is not in the cards. That said, the economic contraction in the months ahead will still be quite severe, in our view (Figures 1 & 2).

Source: U.S. Department of Commerce and Wells Fargo Securities

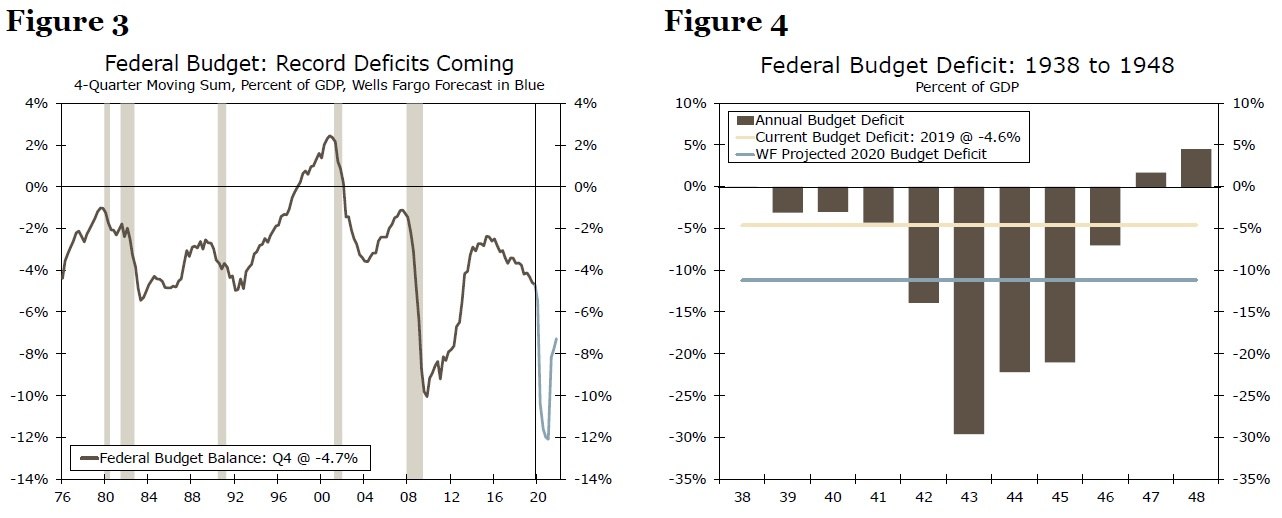

At $2 trillion, the bill that appears likely to become law would be about 9% of GDP, nearly double the size of the stimulus passed in February 2009 during the Great Recession. While we do not have a score yet from the Congressional Budget Office, the actual deficit impact will likely not be quite as big, as some of this $2 trillion are loans that will be paid back over time. Still, from a near term standpoint, the deficit and net Treasury issuance are set to explode. Our latest federal budget deficit forecasts for FY 2020 and FY 2021 are $2.4 trillion and $1.7 trillion, respectively. Relative to our forecast back in early February, these estimates are up from $1.05 trillion for FY 2020 and $1.1 trillion for FY 2021.

Should our latest forecasts prove correct, this would amount to federal budget deficits as a share of GDP of 11.2% in FY 2020 and 7.9% in FY 2021 (Figure 3). If realized, the FY 2020 federal budget deficit would be the biggest deficit as a share of the economy since World War II, when budget deficits were 25-30% of GDP at their peak (Figure 4). We will be updating our net Treasury issuance projections in an upcoming report, but as our readers can imagine, issuance will need to surge across the entire curve to meet this financing demand. Fortunately, the Federal Reserve's openended quantitative easing commitment should ease some of the pressures on private investors to take down this supply. Still, the increase in gross coupon auctions across the curve are likely to be shocking in size.

Source: U.S. Department of the Treasury, Office of Management and Budget and Wells Fargo Securities

Author

Wells Fargo Research Team

Wells Fargo