BoE has spoken, attention will turn to next week’s CPI and the ECB

Outlook

We get the usual jobless claims today, ho hum. Now that the Bank of England has spoken, attention will turn to next week’s CPI (May 15th) and the ECB. The FT has commented several times about how inflation in the US differs from inflation in the eurozone. The IMF takes the stance “… virtually all the US upward price pressures since inflation peaked come from a labour market that is ‘too’ strong. In the Eurozone, it’s entirely a story of outside shocks and their propagation.”

Well, no. When you put the data on the same measurement bases, the US and eurozone have remarkably similar numbers. So the “divergence” story is a crock, at least when it comes to inflation and its underlying causes.

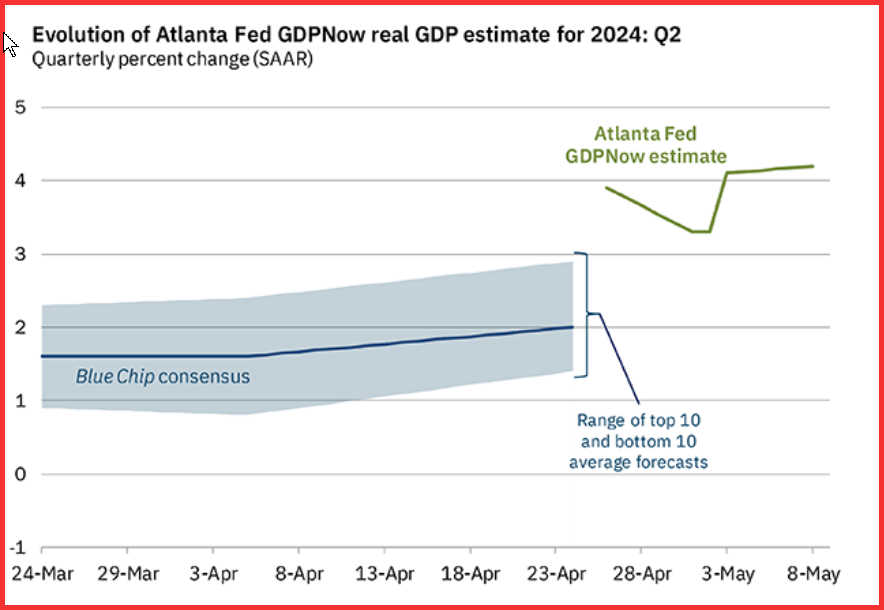

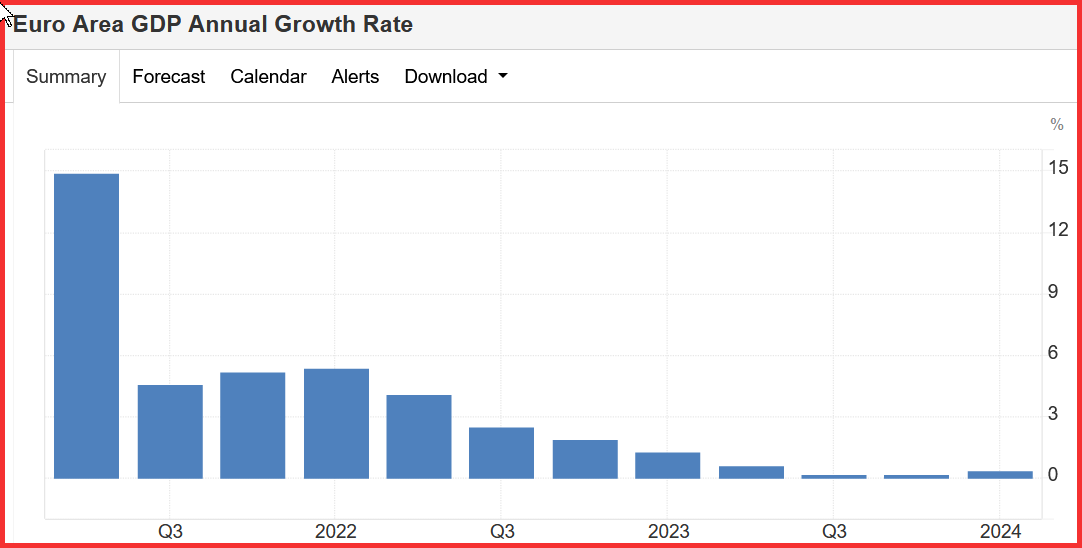

The same cannot be said about economic growth. Some observers were unhappy when the Atlanta Fed reports the latest GDPNow for Q2 up yesterday to a whopping 4.2% (from 3.3% on May 2). The contrast with the eurozone could not be stronger. From recession/near recession over the past two years, eurozone growth is running at 0.4% q/q and will be lucky to hit 1% for the year. Granted, there are wild differences among the member countries, with the former losers (Greece, Spain, Italy) getting the better number and the former winners struggling (Germany, France).

But the point is that the ECB needs a rate cut to goose growth while the US needs to keep rates on hold to rein in exuberance. So while some may want to suggest the Fed is only a month or two behind the UK and ECB with cuts in June, the growth numbers contradict that scenario.

Should we not consider the others will wait for the Fed? Yeah, maybe. If so, a key reason, although hardly anyone will want to say so out loud, is that the ECB rate cut in June dooms the euro to further declines.

Forecast: The pullback is continuing and perhaps gathering steam. As noted above, a central factor is the expectation of a June rate cut by the ECB that policy members have been promoting for some time, while the Fed stands pat and the differential widens. In addition, the messy Middle East prods some to go for the safe-haven dollar.

We might also add that despite some courts allowing Trump to postpone meeting the law until after the election, the one actual trial we do have is going very badly for him and his conduct shows him in an unfavorable light—e.g., swearing out loud at a witness. The so-called base is not influenced but pundits are betting that the very large “undecided” demographic is leaning away, if not actually running.

Intervention saga

We asked a real expert on BoJ intervention whether it’s a rumor or true, and what’s next? Here is part of the reply: “BOJ intervention tactics haven't changed in all these years (and they eventually work so why change?).” Some of the intervention story is actual “covert” intervention and some is whispers. The Japanese attitude: “Why make it public?”

The expert nailed it! This is exactly the attitude we have seen for decades. It’s sophisticated and probably saves a lot of reserve money—one or two small purchases and several whispers to get the machine rolling.

Reasons for the Fed to cut rates

Avoid embarrassment from getting inflation wrong twice.

Normalize the yield curve.

Head off any recessionary tendencies.

Help housing via mortgage rates.

Help banks rollover commercial property loans.

Help the stock market.

Synchronize with the ECB (and Riksbank and SNB).

(Help the current White House).

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat