ADP report reinforces rate cut skepticism

The market is increasingly assuming that a US rate cut is some months away. After another strong data report, this time the March ADP private sector payrolls report, the market is increasingly expecting fewer rate cuts from the Fed this year, with the first rate cut currently on a knife edge between July and September. The market is currently pricing in a 36% probability that the first-rate cut will be in September, this is up from 14% a month ago. The market is becoming increasingly less optimistic about the prospect of near-term rate cuts, and this is having an impact across financial markets.

US hiring reaccelerates in March

The ADP private sector payrolls report was worth watching for a number of reasons. The number of private sector payrolls was stronger than expected at 184k, the market had expected a reading of 150k for March. This was the strongest reading since July, and the February reading was also revised higher to 155k from 140k. This suggests that the economic resilience in the US as we move through 2024 is leading to a re-acceleration in hiring, just at the wrong time for the Federal Reserve. The issue for the Fed is that it will be hard to justify cutting rates if employment is rising, which could put upward pressure on wages and core inflation down the line.

Service sector jobs drives payrolls gain

The split in ADP payrolls is also interesting. The number of service sector jobs rose by 142k, while the number of goods producing jobs was higher by 42k. The number of private sector jobs in the service industry has been accelerating since the start of 2024, whereas goods producing jobs have remained fairly low and stable. This is a problem because the stickiest part of inflation is in the service sector. Job growth was strongest in the south and in large companies compared with small ones.

This data comes at an interesting time. We are waiting to hear from Fed chair Powell, who will be speaking about the economic outlook at 5pm London time. Will he make reference to strong labour markets? It may be hard for him not to.

Waiting for Payrolls data

The ADP data does not have a particularly strong correlation with payrolls data; however, it does suggest that we could get another strong payrolls report on Friday. The market is looking for 214k, down from 275k. However, the strength of hiring in the service sector means that the bias could be to the upside for Friday’s report.

Rising bond yields threatens the stock market rally

US stocks are expected to extend their decline on Wednesday, and US government bond yields are also higher across the curve. The 10-year US yield is up 4 basis points, while the 2-year yield is higher by 3 basis points. US 2-year yields are higher by 13 basis points so far this week, which is another sign of tightening financial conditions in the US as the market prices out the prospect of rate cuts from the Fed.

The ECB set to move before the Fed

In Europe, equity markets are rising, after weaker inflation data for the Eurozone. This is boosting expectations that the ECB will cut rates before the Fed. The market now expects the ECB to cut rates in June, and they are expected to cut rates more than 3.5 times in 2024.

Commodity prices are tomorrow’s inflation risk

Commodity prices are also rising, brent crude is now a mere $0.40 away from $90 per barrel, copper prices, aluminum and nickel prices are also higher today after gold reached a record high overnight. The price of coffee is surging again, and is higher by 2.2%, while wheat prices are also higher by nearly 1%. This is all future inflationary pressure for central banks, and commodity prices are worth watching closely as we move into Q2.

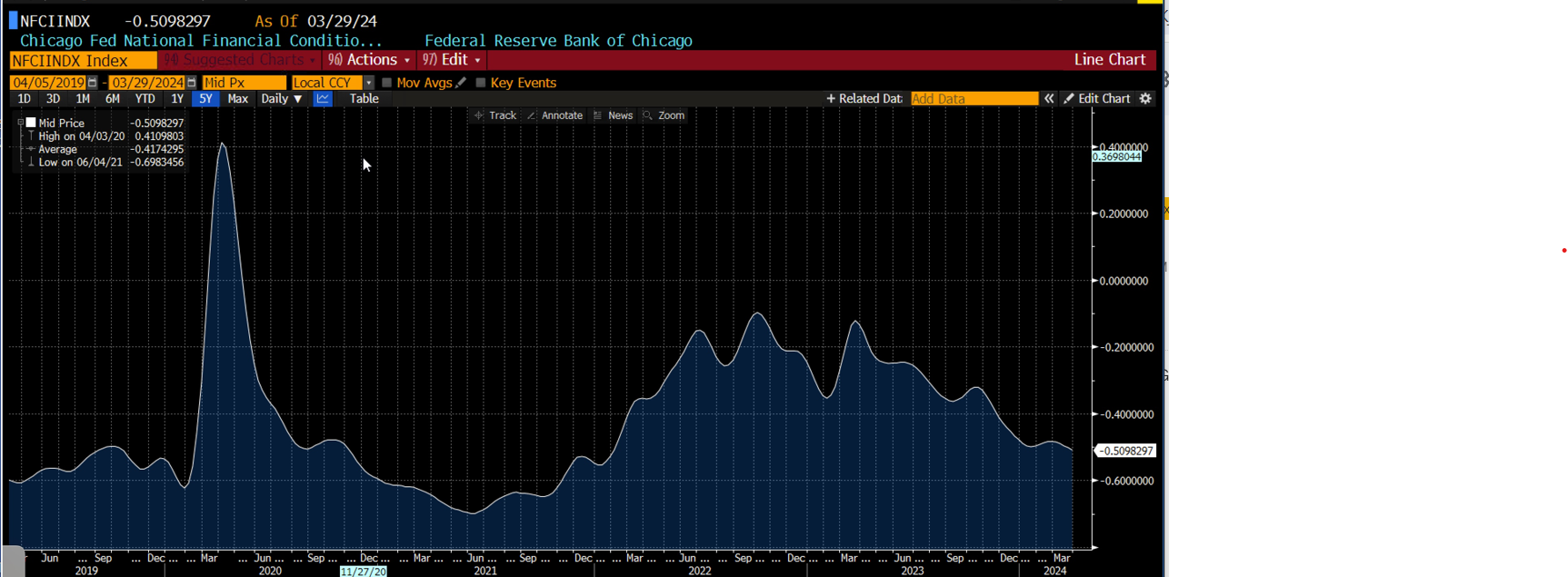

Elsewhere, Jerome Powell’s speech on Wednesday afternoon, along with the US ISM service sector survey for March are the next key drivers for markets, ahead of the payrolls report on Friday. Jerome Powell is unlikely to react to one piece of data, instead he will be looking at the big picture. This is why the financial conditions index is important to determine what the Fed may do next. Financial conditions according to the Chicago Fed National Financial Conditions Index, are lower than average and have been trending lower all year, as you can see in the chart below. However, if Powell strikes a hawkish tone later on Wednesday, then this could lead to a tightening of financial conditions, and confirmation that the market is right to be wary about rate cuts in the first half of this year.

Chicago Fed national financial conditions index

Source: XTB and Bloomberg

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.