Why SPY reversed

S&P 500 ran well into the data release, surged only to reverse in a four-hours selling streak. Some sectoral culprit? No, long-dated bonds did it – TLT daily slide did it. Was it fundamentally justified? Usually, you would see USD go up in tandem, but that didn‘t happen. The selling looks to me to be a combination of exhaustion to the upside (nicely illustrated with MACD divergence) and renewed rotation out of semiconductors after NVDA did its best to catch up to the upside around the data release.

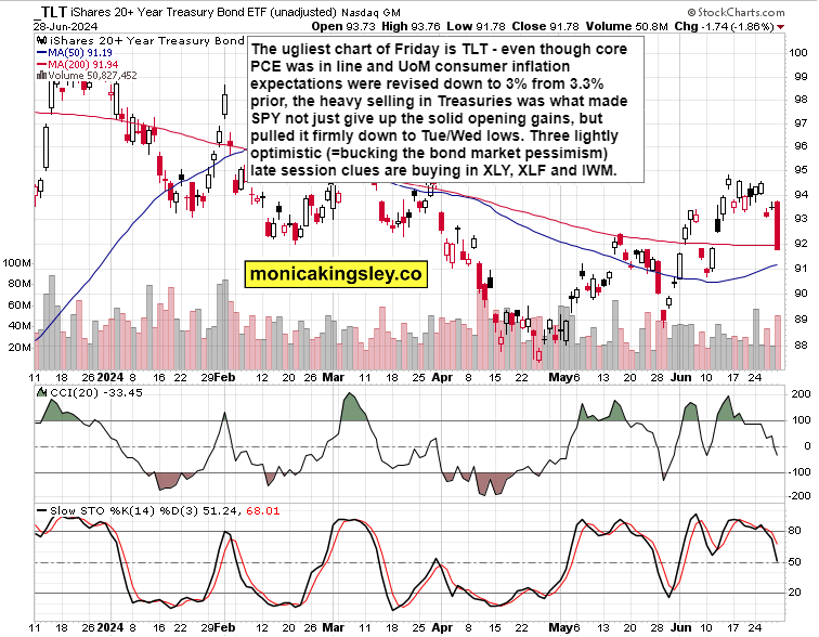

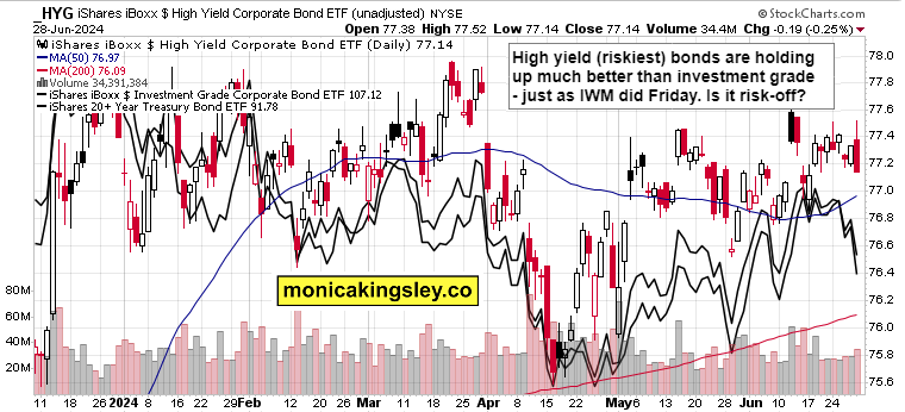

Here is the TLT chart in question, and it better be put right next to high yield corporate bonds performance lately so as to help determine when the current bout of weakness ends (one of the many tools in my toolbox).

Were the PCE data disinflationary? That‘s still been very much the case – but have earnings become that much less attractive compared to yields over the day? For all the question marks still out there, I would argue that higher lows are still there in equities, and that first we see rotations and then broadening out as IWM seems to hint at regarding true(r) rate cut expectation, weeks to months ahead.

Precious metals and oil moved in line with my expectations in the data release aftermath – and that counts for as much in the upcoming stock market path as the sectoral moves themselves.

One more note on long bonds and Friday‘s TLT move – when the US runs a 6% budget deficit and has a 4% trade account deficit, with Japan the largest friendly foreign bondholder for over a year floating policy normalization, and geopolitics playing out in finance, making many countries from the Global South think twice about holding Treasuries. That leaves the Fed ultimately in the buyer of last resort positione coupled with coralling domestic institutions into Treasuries. Hence, I consider the current appreciation of rate cut odds as missing this aspect and concentrating only on domestic economy performance, stagflation / recession worries and soft landing engineering.

Just consider the inflation data backing the Fed has to do a victory lap – the preferred core PCE yoy is at 2.6% vs. 2.8% restated projection. Can‘t be overlooked. Are commodities falling apart here? No, they are in a range, just like bonds are. There is no rush to the exit door, and Fed‘s stress tests didn‘t raise fears about the banking sector. Liquidity watchers are just waiting for it to also become clear Bitcoin could keep above $58K going back to the midpoint of its range just like oil did.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.