Is “selling in May and going away” justified?

Yesterday’s trading session was quite volatile and it was to be expected given the FOMC Rate Decision and the Fed Chair Powell’s Press Conference. The S&P 500 rallied after 2:00 p.m. to give back all the gains, ultimately closing 0.34% lower. At the highest point of the day, it was gaining 1.20%.

On previous Friday, the index hit a new medium-term low of 4,953.56. This marked its lowest level since late February, with a decline of over 311 points or 5.9% from the record high of 5,264.85 on February 28. Last week, stock prices rebounded as tensions in the Middle East somewhat eased, and investors shifted their focus to the quarterly earnings releases.

This morning, the market is likely to open higher and retrace a part of its yesterday’s intraday retreat, with futures contract gaining 0.7%. Today’s Unemployment Claims release has been slightly lower than expected, which didn’t change much for the open.

Yesterday, in my Stock Price Forecast for May, I noted “The question arises: Is this merely a correction or the beginning of a more significant downtrend? It's difficult to determine at this point. Last month, hopes for a Fed pivot were dashed as new data reignited inflation fears, and geopolitical tensions added further uncertainty. However, as of today, it appears the market is only correcting a rally that began in November.”

The investor sentiment improved, as indicated by yesterday’s AAII Investor Sentiment Survey, which showed that 38.5% of individual investors are bullish, while 32.5% of them are bearish. The AAII sentiment is a contrary indicator in the sense that highly bullish readings may suggest excessive complacency and a lack of fear in the market. Conversely, bearish readings are favorable for market upturns.

The S&P 500 is basically trading within a short-term consolidation following its mid-April sell-off, as we can see on the daily chart.

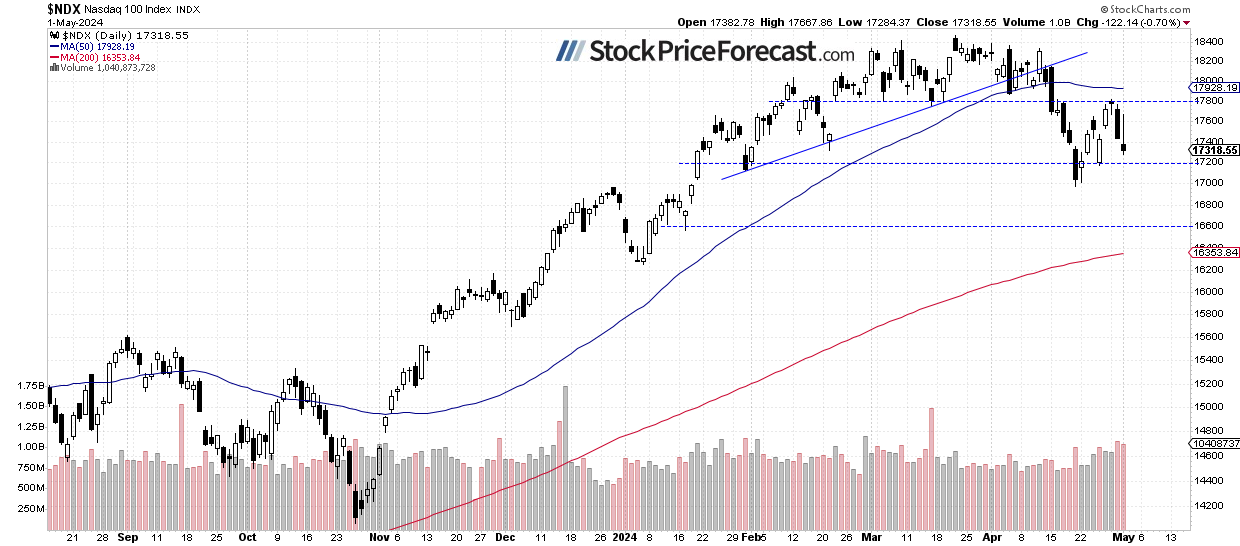

Nasdaq 100 also reversed lower

The technology-focused Nasdaq 100 index closed 0.7% lower yesterday, retracing its post-Fed intraday advance. Last week, it was rebounding from the previous Friday's local low of 16,973.94. The 18,000 level continues to act as a key resistance. Earnings releases have resulted in mostly sideways trading. The market will be waiting for the important release from AAPL today.

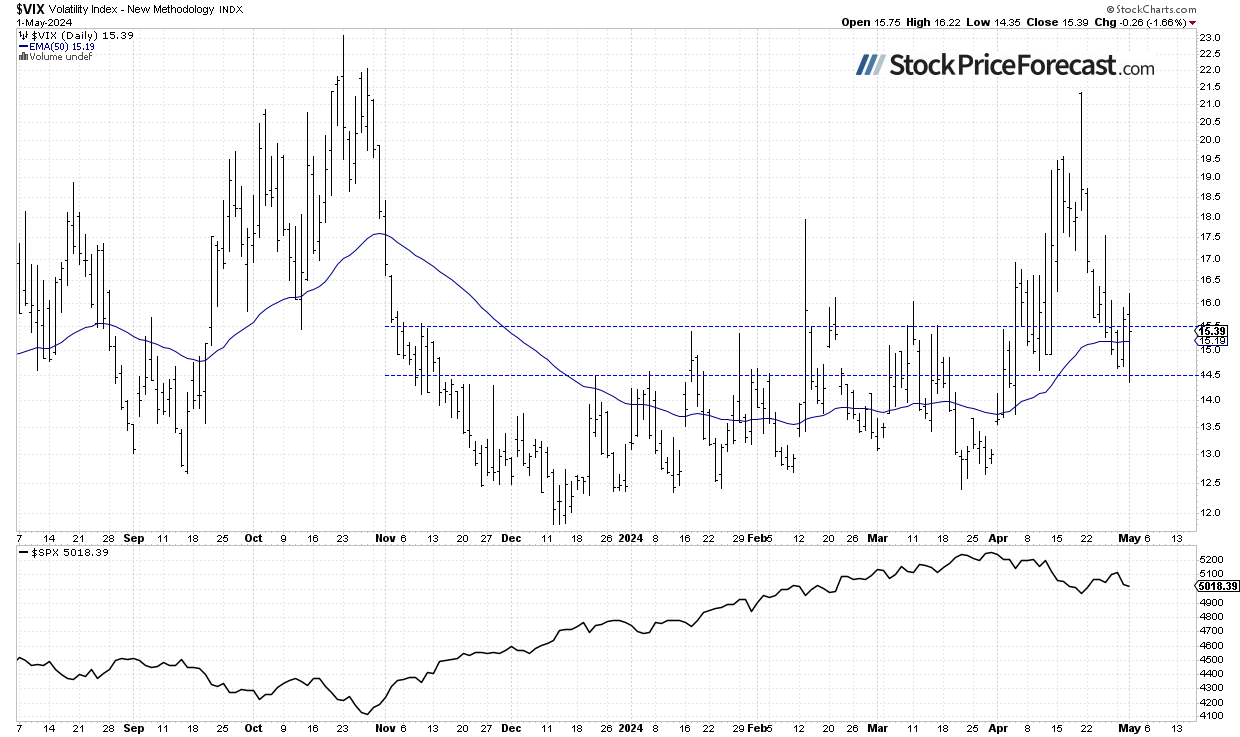

VIX remains near 15

The VIX index, also known as the fear gauge, is derived from option prices. In late March, it was trading around the 13 level. However, recent market volatility has led to an increase in the VIX. On previous Friday, it reached a high of 21.4, the highest since late October, signaling fear in the market. By Friday last week, it retraced to 15. This week, it continued to fluctuate along that level. Overall, the VIX remained relatively low despite significant moves in stocks.

Historically, a dropping VIX indicates less fear in the market, and rising VIX accompanies stock market downturns. However, the lower the VIX, the higher the probability of the market’s downward reversal.

Futures contract slowly gaining

Let’s take a look at the hourly chart of the S&P 500 futures contract. Early this week, it was moving sideways after last week's volatility, but Tuesday’s economic data pushed the market lower, breaking its narrow trading range. The futures contract dropped to a local low near 5,038, retracing nearly all of last week’s rebound from Thursday's local low. The Fed news yesterday caused a rebound, but it didn’t last long, and the market came back closer to its local low.

Today, it is slowly retracing a part of that decline. Investors are eyeing the earnings release from AAPL today after the session closes. The resistance level is at 5,100, and the support level is at 5,000-5,020.

Conclusion

The S&P 500 index rebounded last week, largely driven by quarterly earnings releases from major tech companies. However, Tuesday saw the bears regain control, with the index dropping over 1.5%, and on Wednesday, the market failed to extend gains after the Fed news.

Recently, the S&P 500 was continuing a correction from the March 28 record high of 5,264.85 on Middle East tensions, strong U.S. dollar. On previous Friday, it sold off below the important 5,000 level, and last week, it retraced a much of those declines.

This morning, the stock market is poised to open higher, retracing some of its yesterday’s intraday pullback. However, it may see more short-term uncertainty as investors await earnings from AAPL and the important monthly jobs data tomorrow.

On Tuesday, I mentioned “While earnings reports offer cause for cautious optimism, it remains uncertain whether last week's gains signify a true upward reversal or simply a correction of recent declines.” The pullback in stock prices brought even more uncertainty, with both bullish and bearish scenarios seeming likely depending on market reactions to data and earnings.

In my Stock Price Forecast for May, I added “Where will the market go in May? There's a popular saying: 'Sell in May and go away,' but statistics don't consistently support such clear seasonal patterns or cycles. The safe bet for May is likely sideways trading, with investors digesting recent data suggesting that inflation may not be transitory, and the Fed could maintain its relatively tight monetary policy. However, economic data isn't entirely negative, and strong earnings from companies may continue to fuel the bull market.”

For now, my short-term outlook remains neutral.

Here’s the breakdown:

-

The S&P 500 is likely to retrace a part of its yesterday’s intraday pullback, further extending a consolidation following mid-April sell-off.

-

On Friday, April 19, stock prices were the lowest since February, indicating a correction of the medium-term advance.

-

In my opinion, the short-term outlook is neutral.

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Paul Rejczak

Sunshine Profits

Paul Rejczak is a stock market strategist who has been known for the quality of his technical and fundamental analysis since the late nineties.