As Americans take a more proactive role in their retirement planning, it's essential to understand the key differences between Individual Retirement Accounts (IRAs) and 401(k) plans.

With Social Security facing long-term funding problems and pensions becoming increasingly scarce, it's more important than ever to build your own retirement nest egg through tax-advantaged accounts.

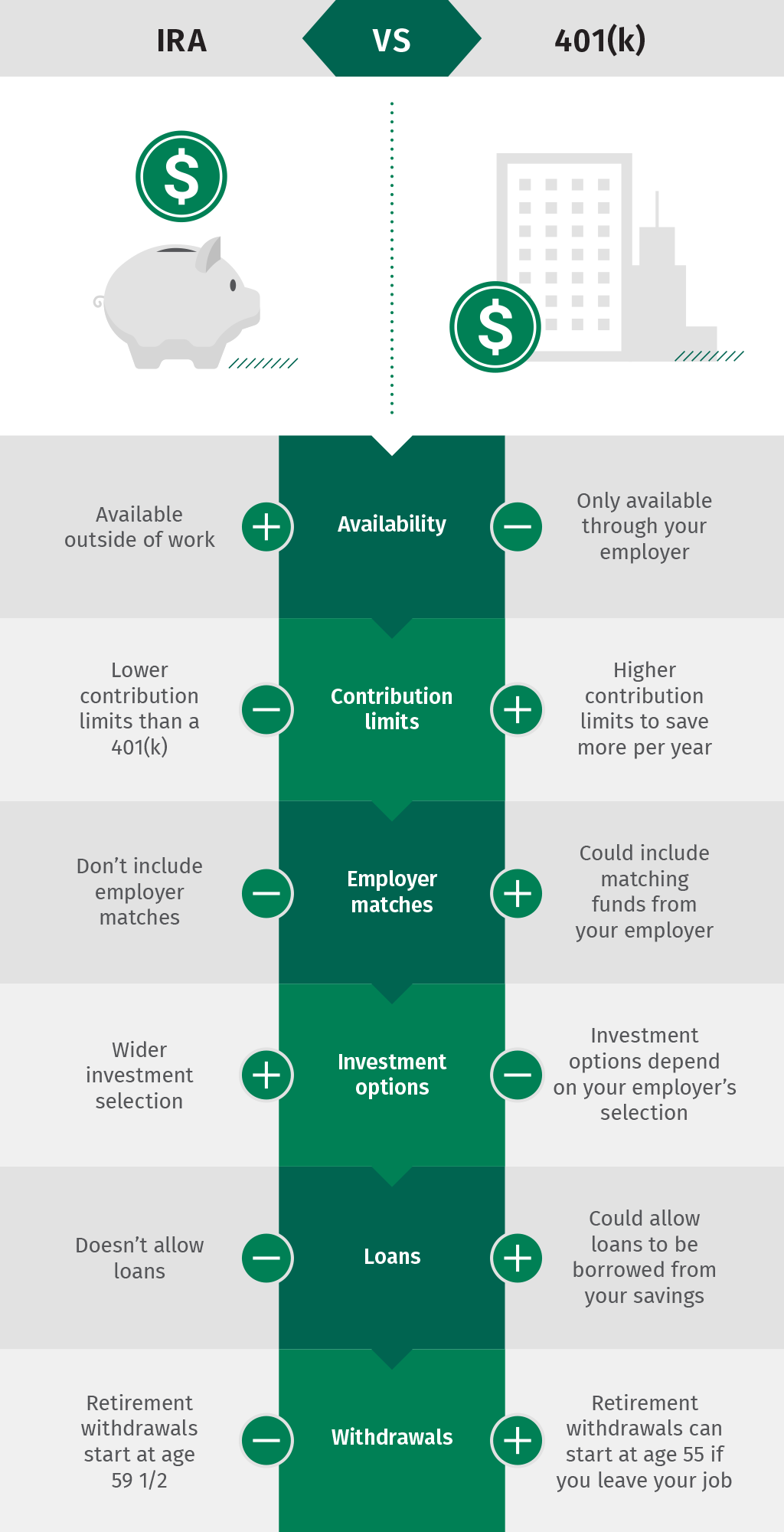

So, when it comes to choosing between an IRA and a 401(k), which is right for you? The answer depends on your employment status, income level, savings goals and the control you wish to exercise over your investments.

IRA and 401(k): Understanding the basics

A 401(k) is an employer-sponsored retirement plan that allows employees to save a portion of their salary, usually on a pre-tax basis.

Contributions reduce taxable income now, and the money grows tax-free until retirement. Many employers offer matching contributions, providing free money to encourage saving.

An Individual Retirement Account (IRA) is opened independently by a bank or brokerage firm. Anyone with income can contribute, whether or not their employer offers a plan.

Like 401(k)s, IRAs come in two main forms: Traditional and Roth. IRAs offer greater flexibility in investment choices, but lower contribution limits.

Traditional or Roth?

- Traditional 401(k) and IRA: Contributions are tax-deductible (based on income in the case of IRAs), but withdrawals are taxed as retirement income.

- Roth 401(k) and Roth IRA: Contributions are made with after-tax money, but qualified withdrawals at retirement are tax-free.

The choice between Roth and Traditional depends on the tax bracket you expect to be in during retirement.

IRA or 401(k): Which should you choose first?

If your employer offers a match, consider maximizing the 401(k) first

Employer matching is the most obvious gain in retirement planning. Not taking advantage of it is like leaving money on the table.

Want to control investments? Consider an IRA

IRAs generally offer broader investment options than most 401(k) plans. If you're comfortable choosing your own funds or working with an advisor, this can lead to better long-term returns, especially if your 401(k) plan has high fees.

Making a lot of money? Beware of IRA limits

If your income exceeds certain thresholds (for example, $165,000 for Roth IRAs in 2025), your ability to contribute or deduct IRA contributions may be limited. 401(k)s do not have these income restrictions.

Want early access? 401(k)s offer more flexibility

Some 401(k) plans allow penalty-free loans or withdrawals starting at age 55 if you leave your job (rule of 55). IRAs generally don't offer loans, and early withdrawals may be more limited.

Source: Citizens

Can you use both IRA and 401(k)?

Absolutely. Many savers contribute to both an IRA and a 401(k), using the 401(k) to benefit from employer matches and higher limits, while using an IRA for investment flexibility or Roth diversification.

Just bear in mind the annual limits and potential income-based restrictions.

Don't rely on Social Security alone

Social Security was never designed to fully replace your earned income. For most Americans, it only replaces about 40% of pre-retirement income, according to the Social Security Administration.

IRA and 401(k) plans help bridge this gap by offering the power of compound interest and tax advantages over decades of savings.

It's not IRA vs 401(k), it's IRA and 401(k)

There's no single answer, but for many, the best strategy combines the strengths of both accounts. Start by capturing all employer 401(k) matches, then consider maximizing an IRA.

If you're self-employed or changing jobs, transfers to an IRA can help you consolidate and manage your retirement savings.

Smart retirement planning isn't about choosing the "best" account, it's about using the tools available to build the retirement you want.

IRAs FAQs

An IRA (Individual Retirement Account) allows you to make tax-deferred investments to save money and provide financial security when you retire. There are different types of IRAs, the most common being a traditional one – in which contributions may be tax-deductible – and a Roth IRA, a personal savings plan where contributions are not tax deductible but earnings and withdrawals may be tax-free. When you add money to your IRA, this can be invested in a wide range of financial products, usually a portfolio based on bonds, stocks and mutual funds.

Yes. For conventional IRAs, one can get exposure to Gold by investing in Gold-focused securities, such as ETFs. In the case of a self-directed IRA (SDIRA), which offers the possibility of investing in alternative assets, Gold and precious metals are available. In such cases, the investment is based on holding physical Gold (or any other precious metals like Silver, Platinum or Palladium). When investing in a Gold IRA, you don’t keep the physical metal, but a custodian entity does.

They are different products, both designed to help individuals save for retirement. The 401(k) is sponsored by employers and is built by deducting contributions directly from the paycheck, which are usually matched by the employer. Decisions on investment are very limited. An IRA, meanwhile, is a plan that an individual opens with a financial institution and offers more investment options. Both systems are quite similar in terms of taxation as contributions are either made pre-tax or are tax-deductible. You don’t have to choose one or the other: even if you have a 401(k) plan, you may be able to put extra money aside in an IRA

The US Internal Revenue Service (IRS) doesn’t specifically give any requirements regarding minimum contributions to start and deposit in an IRA (it does, however, for conversions and withdrawals). Still, some brokers may require a minimum amount depending on the funds you would like to invest in. On the other hand, the IRS establishes a maximum amount that an individual can contribute to their IRA each year.

Investment volatility is an inherent risk to any portfolio, including an IRA. The more traditional IRAs – based on a portfolio made of stocks, bonds, or mutual funds – is subject to market fluctuations and can lead to potential losses over time. Having said that, IRAs are long-term investments (even over decades), and markets tend to rise beyond short-term corrections. Still, every investor should consider their risk tolerance and choose a portfolio that suits it. Stocks tend to be more volatile than bonds, and assets available in certain self-directed IRAs, such as precious metals or cryptocurrencies, can face extremely high volatility. Diversifying your IRA investments across asset classes, sectors and geographic regions is one way to protect it against market fluctuations that could threaten its health.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended content

Editors’ Picks

USD/JPY keeps the bid tone around 163.00

The selling pressure around the Japanese Yen remains unabated on Tuesday, lifting USD/JPY above the key 163.00 hurdle for the first time since December 1986. The pair’s move higher comes on the back of the stronger US Dollar and higher US Treasury yields, all amid steady geopolitical uncertainty.

AUD/USD clings to gains around 0.7000

AUD/USD is now giving away some of its earlier gains and recedes toward the 0.7000 region ahead of the opening bell in Asia. Indeed, the pair now advances modestly, adding to Monday’s uptick and challenging the area of multi-week highs despite the better tone in the Greenback. On Wednesday, Westpac will release its Leading Index gauge.

Middle East crisis intensifies, Gold up

Gold now seems to have embarked on a consolidative phase below the key $4,100 mark per troy ounce in the latter part of Tuesday’s session. Meanwhile, uncertainty surrounding the Middle East conflict and rising expectations for a hawkish Fed policy outlook are expected to limit the precious metal’s bullish momentum in the near term.

XRP rebounds on rising on-chain activity

Ripple (XRP) ticks up and trades around $1.13 at the time of writing on Tuesday. This rebound aligns with a broader recovery in the cryptocurrency market, attributed to reports that mediators between the United States (US) and Iran are seeking a 10-day cessation of strikes to find a way back to the signed Memorandum of Understanding (MoU).

The Iranian war has again risen

The Iranian war has again risen to the top of the economics factor list. There is no end in sight. Intelligence experts say the current level of offense/retaliation will not change minds in Tehran, while in Washington, Trump fears all-out war, which would mean boots on the ground.

![Nasdaq 100 ETF (QQQ) Elliott Wave signals double correction toward 684 [Video]](https://editorial.fxsstatic.com/images/i/Equity-Index_Nasdaq-2_Medium.jpg)

Nasdaq 100 ETF (QQQ) Elliott Wave signals double correction toward 684 [Video]

The short‑term Elliott Wave view on the Nasdaq 100 ETF shows that the instrument is correcting the cycle from the March 30, 2026 low. The decline from the June 3, 2026 all‑time high continues, with the extreme target zone defined by the 100%–161.8% Fibonacci extension. This area lies between $646 and $684 and represents the next logical support cluster within the ongoing correction.