Faced with the uncertainties surrounding retirement and the sustainability of Social Security, Individual Retirement Accounts (IRAs) are emerging as a great option for building a solid financial future.

But what is an IRA, and how does it really work? Let’s take a look at a key retirement tool.

What is an Individual Retirement Account?

An Individual Retirement Account (IRA) is a tax-advantaged retirement savings account that can be opened by anyone with an income. Unlike a 401(k), which depends on an employer, an IRA is managed directly by the saver, via a bank, brokerage firm or financial advisor. It allows you to invest in a wide range of assets like stocks, bonds, mutual funds, ETFs, etc.

IRAs are designed to encourage long-term savings for retirement, offering tax advantages either on entry or exit, depending on the type chosen.

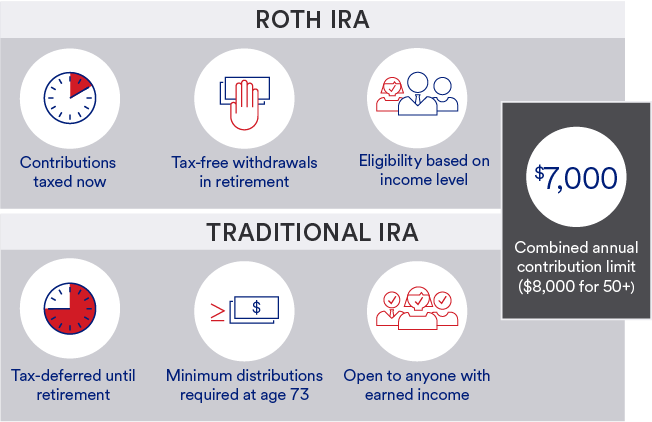

Two main types: Traditional IRA and Roth IRA

IRAs come in several versions, but the most common are the Traditional IRA and the Roth IRA. Their main difference lies in their tax advantages.

Traditional IRA: The immediate tax advantage

With a Traditional IRA, contributions may be tax-deductible (depending on your income and retirement coverage at work). On the other hand, withdrawals at retirement are taxed as ordinary income.

The major advantage is tax-deferred growth. Your investments grow tax-free until you withdraw them. This mechanism can lead to faster capital accumulation.

From age 73, holders are required to start making mandatory withdrawals, known as Required Minimum Distributions (RMDs).

Roth IRA: tax-deferred, withdrawals tax-free

The Roth IRA works in reverse. Contributions are made with money that is already taxed, but withdrawals at retirement are totally tax-free, provided certain conditions are met (being over 59½ years old and having held the account for at least five years).

Another advantage is that Roth IRAs are not subject to RMDs during your lifetime, making them an excellent inheritance or long-term tax planning tool.

Source: USBank

Contribution limits for IRAs

The IRS imposes contribution limits on all IRAs (Traditional + Roth combined). In 2025, the annual limit is set at :

- $7,000 for those aged under 50

- $8,000 with the catch-up contribution for those aged 50 and over.

Income limits also exist to determine eligibility for tax deductions (Traditional IRA) or to contribute to a Roth IRA. These thresholds vary according to tax status (single, married, etc.) and the presence of a retirement plan at work.

Why open an IRA, even when having a 401(k)?

Many people feel that their 401(k) is sufficient to prepare for retirement. But according to Fidelity, you'll need between 70% and 80% of your pre-retirement income to maintain your standard of living after you leave the workforce. Social Security only covers part of this amount, and 401(k)s often have limited investment options.

An IRA allows you to diversify your investments, complement a corporate plan and access more flexible tax planning strategies. You can also rollover from an old 401(k) to an IRA when you change employers, to consolidate and better manage your assets.

Withdrawal and tax rules

Withdrawing money from an IRA before age 59½ generally incurs a 10% penalty, in addition to applicable taxes (with exceptions, such as medical expenses or the purchase of a first home). That's why IRAs are designed for the long term.

A more comprehensive retirement planning

One option for an effectively planned retirement is to combine several sources of savings: 401(k), IRAs, taxable accounts and Social Security.

Having an IRA, whether traditional or Roth, allows you to balance the taxation of your future income and better manage your withdrawals according to your needs and tax bracket.

Whether you're employed, self-employed or an entrepreneur, Individual Retirement Accounts (IRAs) offer a solution for anticipating the future.

Their flexibility, accessibility and tax advantages make them a good tool for securing your retirement, especially at a time when the future of Social Security is uncertain and company plans are often no longer sufficient.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended content

Editors’ Picks

USD/JPY climbs toward 162.00 as USD bounce offsets intervention risks

USD/JPY is building on Friday's recovery toward 162.00 in Monday's Asian session. Despite receding bets of a Fed hike, interest rates in the US remain higher than in Japan. This keeps the so-called carry trade in play, countering a shift in Japan's intervention tactics and undermining the Japanese Yen.

AUD/USD holds lower ground below 0.6950 amid cautious markets

AUD/USD kicks off the new week on a softer note as tensions over the critical Strait of Hormuz lend some support to the safe-haven US Dollar, leaving the pair undermined below 0.6950. However, receding Fed-hike bets limit USD gains, which, along with the RBA's hawkish stance, could limit the Aussie's downside.

Gold off two-week top, below $4,200 as Hormuz risks support USD

Gold struggles to capitalize on its strength beyond $4,200 and retreats slightly from a two-week high touched in the Asian session on Monday. The US Dollar edges lower amid persistent geopolitical uncertainties stemming from tensions in the Strait of Hormuz, acting as a headwind for the bullion. However, receding Fed-hike bets might hold back USD bulls and help limit the downside for the non-yielding yellow metal.

Week ahead: ISM services PMI and Fed Minutes to shake Fed hike bets

Dollar drops on NFP, but rate hike still expected by year-end. ISM services PMI and Fed minutes are the greenback’s next catalysts. RBNZ expected to raise rates, focus will be on forward guidance. ECB minutes, China CPI and Canada’s jobs report also on the agenda.

Why central banks are loading up on Gold during the current 30% correction

Gold has crashed from $5,500 to $4,000 in five months, marking a decline of almost 30% that has triggered widespread retail panic. However, this correction could present a significant opportunity, driven by an unprecedented market indicator: central bankers and the world's largest asset managers are aggressively buying.

Johnson & Johnson flashback update: Wave five extension in progress toward new highs

As discussed back on June 10, Johnson & Johnson was expected to continue higher after completing a complex wave 4 correction. That scenario played out, with price pushing back to all-time highs. A projected wave 5 now appears to be in progress, with further upside potential as a lower-degree five-wave bullish impulse unfolds.