Where are the Central Bank's positioned as we enter July?

Major central bank rundown

The central banks are listed below with their current state of play.

Reserve Bank of Australia, Governor Phillip Lowe, 0.10%, Meets July 14

Holding still

Once again the June 01 RBA meeting was uneventful. No rate hikes expected until actual inflation is within the 2-3% range and supportive monetary conditions (low rates etc) are to be maintained in order to support a return to full employment and for inflation to be consistent with this target. The labour market is not expected to be tight enough to spur higher age growth (and therefore inflation with it) until 2024. So, on hold with rates until 2024 is the mantra. The RBA noted that significant outbreaks of the COVID-19 virus remain, but as more people get vaccinated this risk should fade. The RBA still sees inflation in underlying terms remaining low and underneath the central bank targets. The economic recovery is stronger than earlier expected and is forecast to continue. The Bank’s central scenario is for GDP growth by 4.75% and 3.5% over 2022. Progress in reducing unemployment has been faster than expected with unemployment expected to drop to around 5% by the end of this year.

The takeaway

As mentioned in the last central bank overview, one of the key economic points to look at going forward is the unemployment rate. Fast progress here and this is what will move the RBA’s dial. Say, we got a surprise jump down to below 5% then that should bring forward the RBA interest rate projections and the trade would be to buy the AUD a few days or even just the day before the next rate meeting.

The July meeting is key for the Reserve Bank of Australia (RBA) because it is the place where key decisions will be made about the QE programme and whether the current yield curve control will be maintained. Here is an extract from June’s statement:

“At its July meeting, the Board will consider whether to retain the April 2024 bond as the target bond for the 3-year yield target or to shift to the next maturity, the November 2024 bond. The Board is not considering a change to the target of 10 basis points. At the July meeting, the Board will also consider future bond purchases following the completion of the second $100 billion of purchases under the government bond purchase program in September. The Board continues to place a high priority on a return to full employment.”

RBA’s Governor Lowe has taken the unusual step of arranging a press conference one and a half hours after the RBA decision. Why? This allows the Governor time to see how bonds react to a potential tapering announcement and the fact that yield curve control will be coming to an end. It is what is called a ‘parachute meeting’. Designed to halt the terminal fall in bonds. So, expectations of strength into the RBA meeting is not unreasonable.

European Central Bank, President Christine Lagarde, -0.50%, Meets June 10

A steady hand meeting

In many ways, the meeting on June 10 at the start of the month was very similar to their April meeting. Interest rates were kept unchanged and the size of the bond purchases (PEPP) was unchanged at €1.85 trillion. QE purchases are continuing at the speed of €20 billion a month, but the differences were in the emphasis of the last meeting.

A steady hand, with increasing optimism

There were four reasons for increasing optimism from the ECB going forward.

Firstly, immediately after the meeting, a sources piece revealed that three ECB board members were in favour of bond tapering, There had been some expectations around the middle of May that the ECB would taper at their June meeting. These expectations gradually dissipated as the date grew closer to June 10 due to a flurry of dovish comments in the run-up to the meeting. However, the ECB board members ready to taper shows optimism mounting.

Secondly, there were upgrades to future GDP projections. The ECB expect activity to accelerate in H2 2021. 2021 to 4.6% vs 4.0% previously. 2022 to 4.7% vs 4.1% previously. 2023 at 2.1% vs 2.1% previously.

Thirdly, inflation projections were revised higher: 2021 to 1.9% vs 1.5% previously, 2022 to 1.5% vs 1.2% previously, 2023 to 1.4% vs 1.4% previously.

Fourthly, Christine Lagarde said that growth risks were no longer ‘tilted to the downside’. Instead, they were are now seen as ‘broadly balanced’.

So, all in all, there was some decent optimism here. However, when it comes to talk about tapering Christine Lagarde was very guarded, In responding to a direct question on tapering she said that

“You’re going to be bored with me, but I am going to repeat myself. Any discussion about exit from the PEPP, as you just mentioned, would be premature, it’s too early and it will come in due course. Certainly, for the moment it’s too early and premature, as simple as that”. So, the owl has spoken.

The takeaway?

EURCHF longs look attractive from a macro perspective. Over the course of the next 6 months it would be reasonable to see further EURCHF upside on a normalisation process from the ECB if the eurozone economy continues to bounce back. The outlook for COVID-19 in the eurozone could invalidate this outlook, as could a rapid slowdown in the eurozone.

Bank of Canada, Governor Tiff Macklem, 0.25%, Meets July 14

Holding meeting

On April 21 the CAD rallied strongly after bond purchases were reduced from $4 billion per week to $3 billion per week. On top of this, the BoC brought forward interest rate hikes from 2023 to 2022 as they are expecting the economic slack to now be absorbed sooner than anticipated in the last central bank meeting. The June 09 interest rate meeting was a holding meeting and there were no major surprises. Interest rates were kept at 0.25% and QE at $3 billion per week.

However, the tone of the meeting was broadly optimistic. The BoC’s perspective is that “with COVID-19 cases falling in many countries and vaccine coverage rising, global economic activity is picking up.” The BoC noted that the US is experiencing a strong recovery and that a rebound is starting to take place in Europe.

The BoC on inflation

They see inflation rising higher in the near term. Inflation is expected to remain near 3% over the summer but ease later in the year. The BoC noted that core inflation had risen less than CPI inflation. Central banks will be keeping a close eye on inflation to ensure it doesn’t run out of control. The BoC firmly expects transitory inflation like the Federal Reserve and falling inflation into year-end.

Other points to note

Like April’s meeting concerns remain about low wage workers, but these concerns should be fine as job openings remain strong, so jobs should pick up from here as Canada is quickly vaccinating its citizens.

The fall in jobs is largely due to COVID-19 restrictions that Canada went back into and not necessarily a wider problem. So, expect this to pass. Also, a strong jobs report will tick the BoC’s box and could lead to some CAD strength if/when it comes.

The housing market once again came under the eye of the BoC, but it was just one line in the statement, “housing market activity is expected to moderate but remain elevated”. Ok, move along for now.

Path of the CAD

After the April central bank meeting, it was reasonable to expect USDCAD weakness. However, the outlook remains more neutral for now out of June’s meeting depending on the USD moves. However, CADJPY and CADCHF dip buyers continue to make sense as the BoC are still on track for further bond tapering in July.

This was a holding meeting for the BoC, but the broad optimism remains the same with the BoC attributing the recent wobble to renewed restrictions on Canada’s third COVID wave. “Despite the second wave of the virus, first-quarter GDP growth came in at a robust 5.6 per cent. While this was lower than the Bank had projected, the underlying details indicate rising confidence and resilient demand. Household spending was stronger than expected, while businesses drew down inventories and increased imports more than anticipated. Renewed lockdowns associated with the third wave are dampening economic activity in the second quarter, largely as anticipated.”

Remember that stronger oil supports the CAD as around 17% of all Canadian exports are oil-related. There is a negative correlation between USD/CAD and oil has broken down recently. Canada’s top export is Crude Petroleum at over $66 billion and around 15.5% of Canada’s total exports.

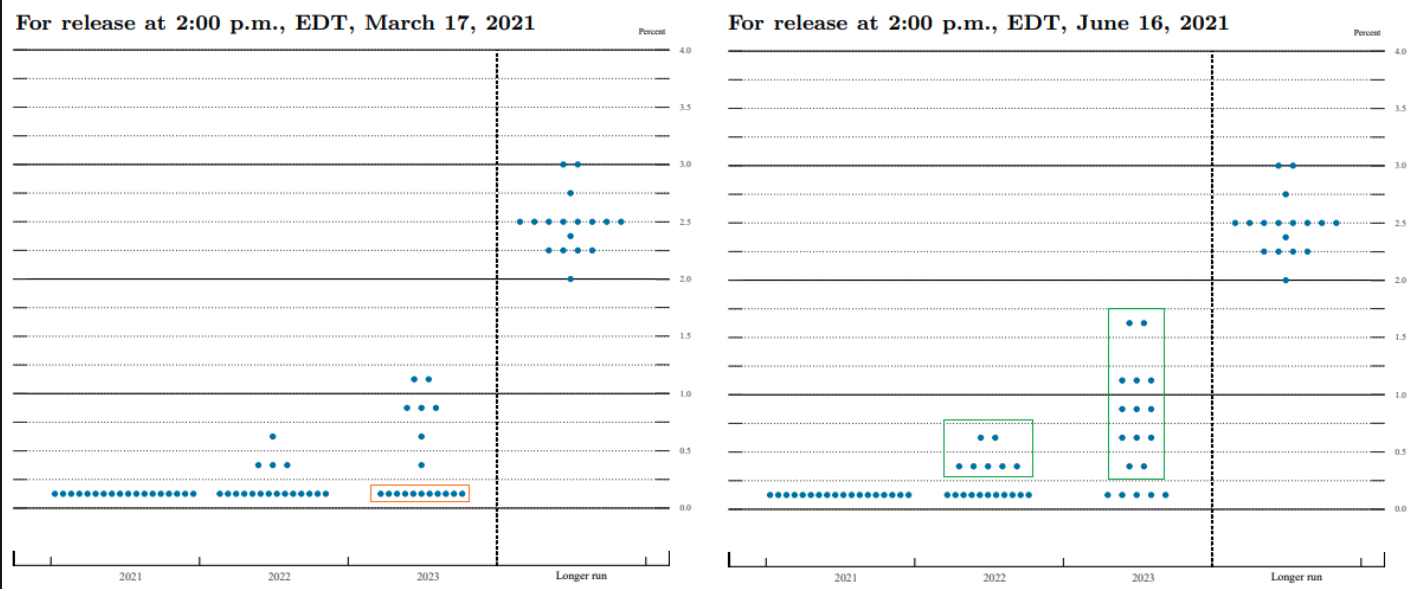

Federal Reserve, Chair: Jerome Powell, 0.125%. Meets July 27-28

Federal Reserve dumps the script of ‘no rate rises until 2024’

The major news was that there was a hawkish shift from the dot plots at the last interest rate meeting. In the end, the dot plot saw more members opting for earlier rate hikes in this meeting than last. The June meeting saw 7 members looking for hikes in 2022 and 13 members in 2023. This was a significant jump from the March meeting where only 4 members saw a hike in 2022 and 7 members saw hikes in 2023. This resulted in the US10 year yields jumping higher and does give the USD a more bullish outlook now in the near term.

The path of QE stayed at $120 bln per month and guidance was unchanged, the IOER rate was increased to 15bps from 10bps (this was not a hike just a technical adjustment).

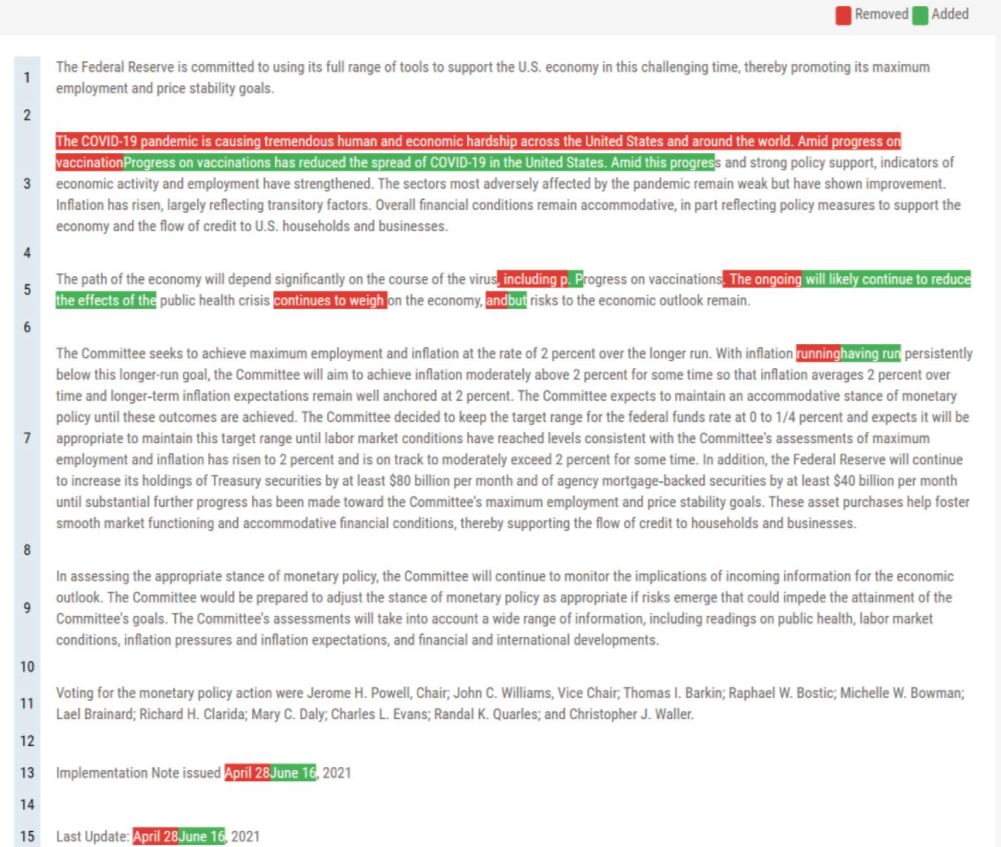

One of the noteworthy elements was that the following line was removed from the latest statement: “The COVID-19 pandemic is causing tremendous human and economic hardship across the United States and around the world.” This sentence was replaced by, “Progress on vaccination has reduced the spread of COVID-19 in the United States.” This is far more optimistic and shows a country coming out of COVID-19. In the press conference, Powell was upbeat surrounding the labour market stating that “it is clear we are on a path to a very strong labour market.”

Federal Reserve statement

In the press conference, Fed Chair Powell recognised that “inflation could turn out to be higher and more persistent than we expect.” This is a nod to the recent strong run of CPI data that has come out. Some in the Fed are clearly concerned that inflation may not be transitory. However, although the inflation projections for this year for Core PCE rose to 3.0% from 2.2% the 2022 forecast was only revised slightly higher to 2.1% and the 2023 forecast remained unchanged. This means the core Fed message is that the majority still expect inflation to be transitory.

The takeaway

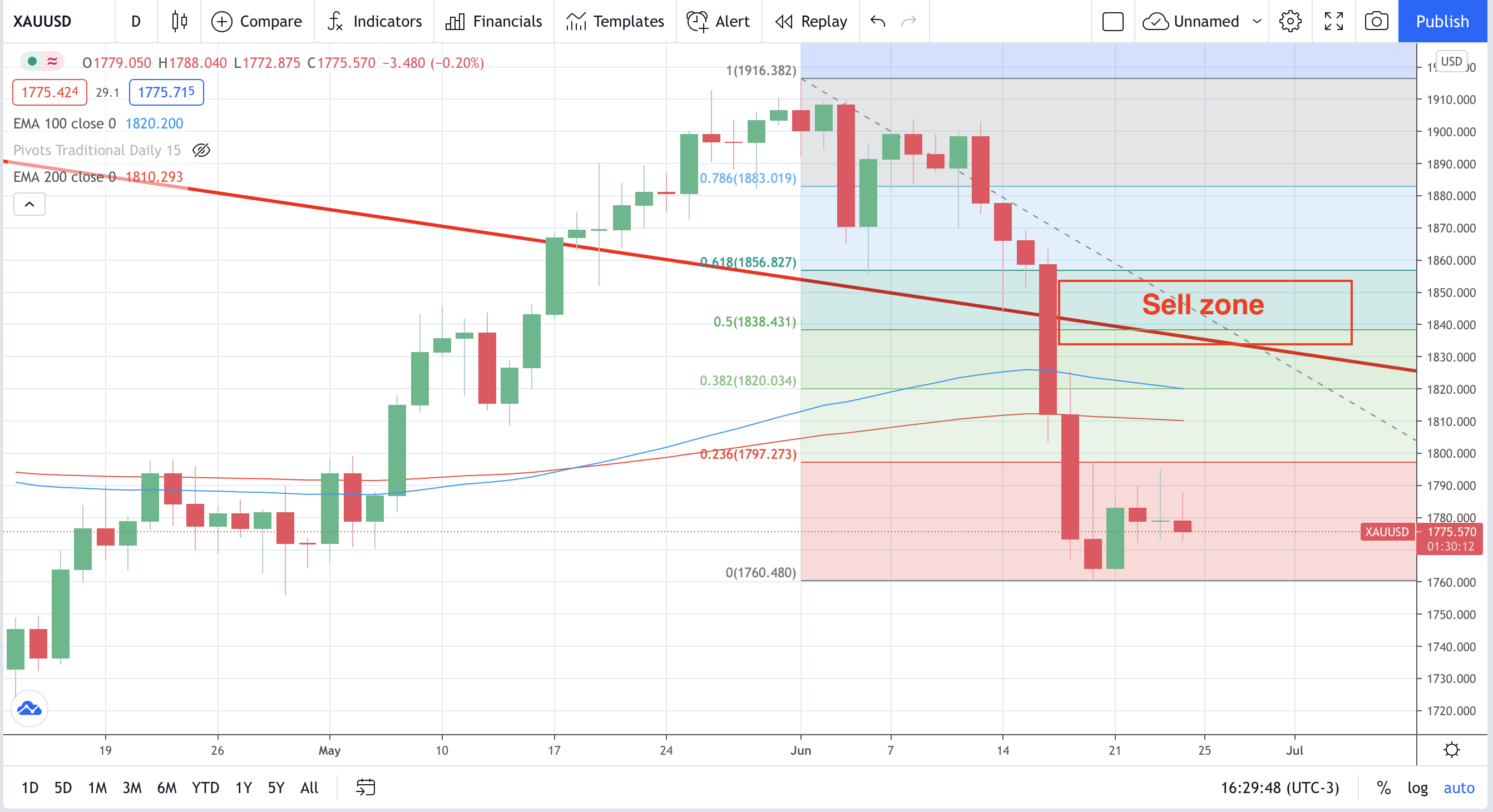

A clear shift from the Fed. Near term bullish outlook for the USD and bearish outlook for Gold, USDJPY longs on dips makes sense (check US 10 year yields) and XAUSD shorts make sense (check real yields and inflation expectations). The sweet spot for gold selling is US 10 year yields rising, and inflation measures falling.

Bank of England, Governor Andrew Bailey, 0.10%, Meets August 05

Up until this weeks meeting, there had been two upbeat central bank meetings from the Bank of England. It could have been anticipated that this would really have increased the odds of a hawkish twist from the BoE. Heading into the Bank of England meeting Sonia futures were pricing in a more optimistic Bank of England with interest rates projected to rise next year. However, the actual meeting itself was a disappointment. The only dissenter to the headline prints was Andy Haldane who voted to taper asset purchases. The vote was 8-1 in favour of tapering. However, this was Andy Haldane’s very last MPC meeting, and a lack of hawkish comment left the GBP stop sell-off fairly quickly out of the meeting.

Inflation was considered transitory, so no need to raise rates quickly. The high inflation print from May was acknowledged as being ‘above the 2% target’ (it was 2.1%).

Growth expectations were revised higher by 1.5% with a strong recovery noted in the consumer-facing services for which restrictions were loosened in April. The hot housing market, which could have had the BoE act to contain, was merely seen as ‘strong’. So, no worries there from the BoE.

The meeting as a whole was a very holding affair and August is now seen as the key date for the MPC to ‘fully assess the economic outlook’. Perhaps the BoE will taper next time? One thing for certain is that it now needs Vlieghe and Ramsden to quickly fill the absence of Haldane’s hawkish shoes if the BoE is going to move towards tapering.

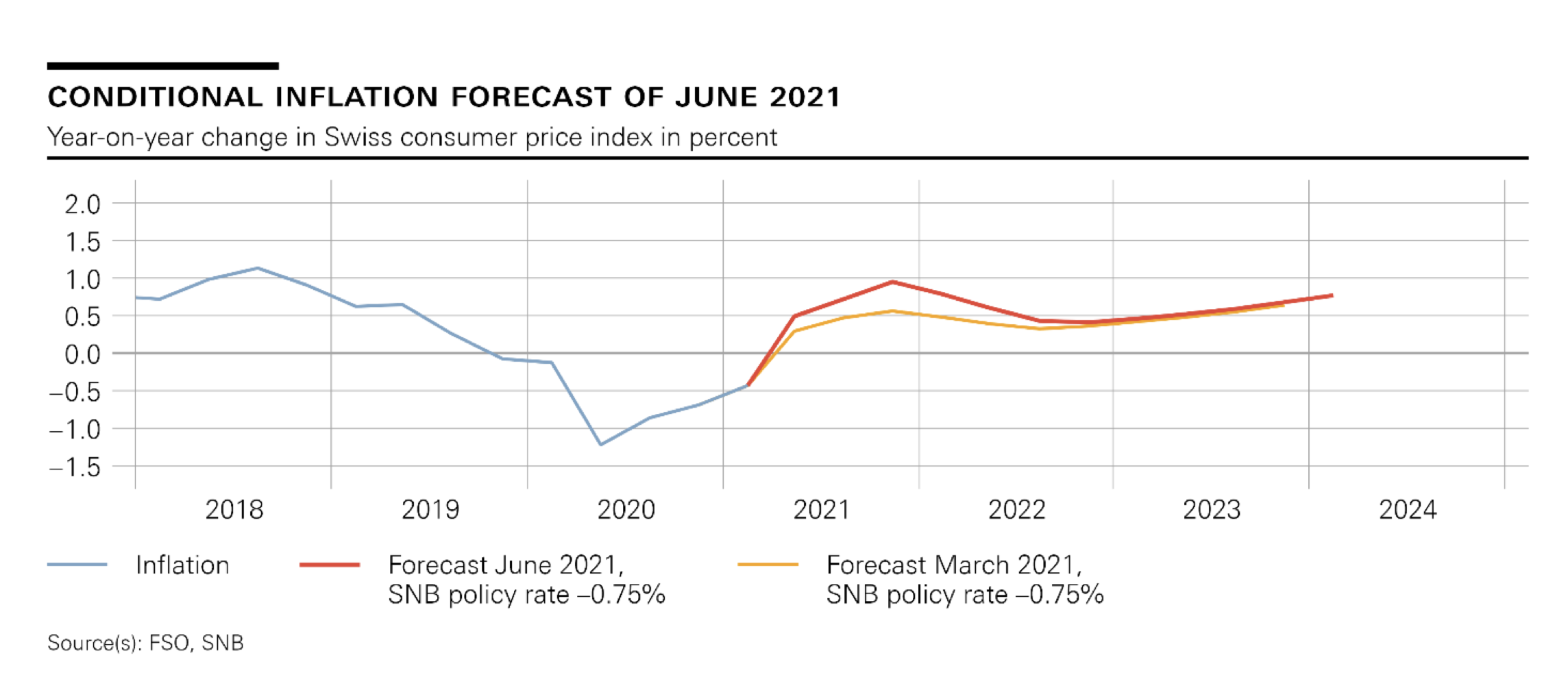

Swiss National Bank, Chair: Thomas Jordan, -0.75%, Meets September

The SNB interest rates are the world’s lowest at-0.75% due to the highly valued Franc. As an export-driven economy, they hate a strong CHF and are doing their best to make it as unattractive as possible. The market generally ignores this and keeps buying CHF on risk aversion which has been here in one form or another since around 2008/2009 according to the EURCHF chart. The SNB hate this and repeat, as they did in the latest meeting, that the ‘Swiss franc remains highly valued’. However, recent prices mean the EURCHF long term floor does look in place.

On their June 17 meeting, the SNB left rates unchanged. The inflation forecasts were revised higher again. The reasons cited had increased too from the previous meeting. In the March meeting, it was only oil-related products that were mentioned. In the June meeting, it expanded to ‘higher prices for oil products and tourism-related services, as well as for goods affected by supply bottlenecks’. The new forecast stands at 0.4% for 2021, and 0.6% for both 2022 and 2023. The conditional inflation forecast is based on the assumption that the SNB policy rate remains at −0.75% over the entire forecast horizon. Watch out for high inflation to possibly prompt the SNB into action, but note that we are nowhere near that now.

In terms of growth, the SNB was far more upbeat. In the March meeting, they projected growth of 2.5% -3%. In the June meeting, they noted that the economic indicators had improved significantly of late. Growth for 2021 is now seen at around 3.5 mainly due to the lower than expected decline in GDP in Q1. The statement struck a tone of optimism vs ‘who knows what will really happen. However, a more optimistic note was found in the statement.

The SNB will continue to intervene in the FX markets. The Swiss are always mindful of the EURCHF exchange rate because a strong CHF hurts the Swiss export economy. The SNB want a weaker CHF. The rest of the world wants CHF as a place of safety in a crisis, so we have this constant tug of war going on.

Note that a currency like the EUR could offer some decent upside against CHF over the coming months as the ECB prepare to taper. The SNB are still content to be the lowest of the central bank pack and dissuade would-be investors by charging them for holding CHF. EURCHF for a 6-12 month hold is worth considering and just checking in with the ECB and SNB policy shifts.

Bank of Japan, Governor Haruhiko Kuroda, -0.10%, Meets July 16

The Bank of Japan remains a very bearish bank and there is no sign of exiting from its easy monetary policy. The latest meeting saw no surprises and everything was expected in the June 18 policy meeting. The headlines were as expected with Interest rates remaining at 0.10%. In a similarly unmoved fashion, the Yield Curve Control (YCC) was maintained to target 10-year JGB yields at 0.0%. The vote on YCC was made by 7-1 votes with Kataoka the dissenter and Masai the abstainer.

The general outlook is that the economy is seen to be improving. The BoJ noted that ‘exports and industrial production have continued to increase steadily. In addition, corporate profits and business sentiment have improved on the whole.’

There was a new funding scheme announced to help firms adapt to greener climate demands in the future. ‘The Bank judged it appropriate to introduce a new fund-provisioning measure, through which it provides funds to financial institutions for investment or loans that they make to address climate change issues based on their own decisions.’

Inflation was revised up fractionally, but low inflation has dogged the BoJ for years and they are a long way off their 2% target.

- Japanese National CPI (May) -0.1% y/y vs. Exp -0.2% (Previous -0.4%)

- Japanese National CPI Ex. Fresh Food (May) 0.1% y/y vs. Exp 0.1% (Previous -0.1%)

- Japanese National CPI Ex. Fresh Food & Energy (May) -0.2% y/y vs. Exp -0.3%

The only thing to say is that there is no change to the perspective that the Bank of Japan is ready to step in to support Japanese equity markets if they are needed to. Aside from this, there is no change expected for the foreseeable future. Be aware that the JPY continues to operate as a safe haven currency and in times of financial stress and worry the JPY tends to find buyers. The AUDJPY is the go-to risk-on / risk-off currency pair.

Reserve Bank of New Zealand, Governor Adrian Orr, 0.25%, Meets July 2021

The interest rate at the last RBNZ rate meeting was unchanged, the interest rate was kept at 0.25%, but crucially a rate hike was signalled for 2022. Remember that the name of the RBNZ rate decision has changed from OCR (Official Cash Rate) to MPR (Monetary Policy Review). The reason for the change is that other tools such as forward guidance and LSAP, not just the OCR, are being deployed to achieve the Monetary Policy Committee’s (MPS) mandate of low and stable inflation and full employment. So, if you see an MPS/MPR announcement that is referring to what used to be the OCR statement. Confusing and annoying? Yes, but that’s a name change for you.

This policy shift resulted in some immediate upside in the NZD. Governor Orr took the view that some of the more extreme risks were off the table. However, there was a tentative note to his decision where he stated that the rate hike projection for September 2022 was highly conditional. The reason for the caution was what you would expect. COVID-19 containment dependent. Much of what was said can be summarised by one simple quote from the MPS statement, “The sustainability of the global economic recovery remains dependent on the containment of COVID-19”.

Inflation

The RBNZ were very unconcerned about inflation. Inflation was put down to the usual suspects of higher commodity prices, higher oil prices, and pressure on shipping arrangements. The RBNZ expect these pressures to alleviate over the course of this year.

The takeaway

This does open up a central bank divergence between the RBA and the RBNZ. The RBA is on hold after their last interest rate meeting and wants to see unemployment move down to 4%. The RBNZ, by contrast, now see a rate hike in 2022. The bond yield spread has moved lower and this makes a sell on rallies for the AUDNZD the obvious trade. If the risk tone remains positive a very deep NZDJPY long makes sense as does an NZDUSD long as long as the Fed don’t look like tapering.

Author

Giles Coghlan LLB, Lth, MA

Financial Source

Giles is the chief market analyst for Financial Source. His goal is to help you find simple, high-conviction fundamental trade opportunities. He has regular media presentations being featured in National and International Press.