Someone observed recently that the holidays are starting late this year, as the time between Thanksgiving and Christmas is shorter than usual. You could have fooled me; judging by store displays and TV advertising, the commercial side of the season is already two months old.

Not everyone observes holidays on the schedule that the United States does, and spending is very much a year-round activity (at least in my house). Nonetheless, the approach of the Christmas retail season always places focus on the fiscal and mental state of American households. The world watches these examinations closely, given the importance of U.S. consumption to global economic performance.

This year’s check-up reveals a series of encouraging strengths. But there remain some aches and pains that restrict movement and require rehabilitation. The new normal is not bad, but it is a far cry from the halcyon days of 10 years ago.

Personal consumption accounts for nearly 70% of U.S. gross domestic product (GDP) and imports are about 16% of GDP. American buying behavior is therefore central to the world outlook. Wages and wealth in the United States, the two supports of spending, were both badly damaged by the Great Recession. Both have recovered, but unevenly.

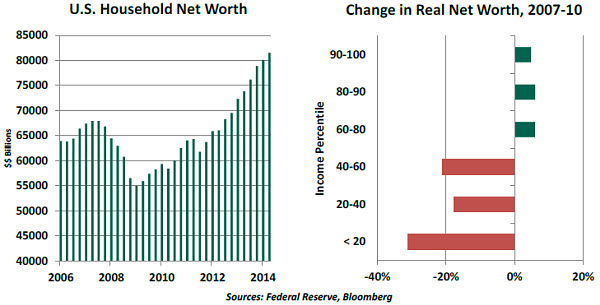

The aggregate net worth of American households has smashed prior standards, thanks to a powerful bull market in equities. This boosts spending through the “wealth effect” and should be a great base for holiday sales.

But this bounty has not been widely distributed. According to the Federal Reserve’s Survey of Consumer Finances, less than 5% of families in the lowest 40% of the income distribution own shares directly or through pooled investment products; they have therefore not benefitted as much from the rally in the S&P 500. Home equity was the main source of wealth for this cohort, but home prices have not rebounded with nearly the same vigor.

U.S. consumers have leverage under better control than they did five years ago. The ratio of household debt to income is at 10-year lows, and low interest rates make debt servicing manageable. While there are still families working hard to get their balance sheets into better order, there has been some loosening of purse strings.  But households remain fairly cautious about taking on additional leverage, which is what fueled consumption gains a decade ago. Despite credit terms that have been getting increasingly easy, credit card borrowing is essentially flat over the last 12 months. Student debt has risen sharply since the crisis and the resulting burden limits spending on the kinds of goods typically exchanged over the holidays.

But households remain fairly cautious about taking on additional leverage, which is what fueled consumption gains a decade ago. Despite credit terms that have been getting increasingly easy, credit card borrowing is essentially flat over the last 12 months. Student debt has risen sharply since the crisis and the resulting burden limits spending on the kinds of goods typically exchanged over the holidays.

U.S. unemployment has fallen sharply in the last two years, thanks to the creation of five million new jobs over that period. The restoration of income for those back at work will help consumption. But an important fraction of the newly hired are working part time, because full-time work is not available. And wages are barely keeping pace with inflation.

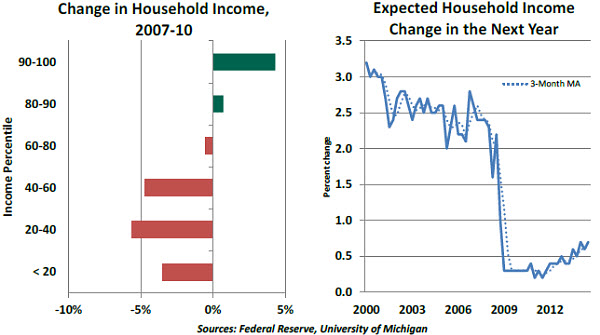

As is the case with household wealth, there is an increasing gap in income between those who have prospered since 2007 and those whose fortunes have moderated. The Survey of Consumer Finances found that families between the 40th and 90th percentiles of the income distribution saw little change in real income between 2010 and 2013. Families below this window saw continued declines. Only families in the top tiers of the distribution saw widespread gains over that time.

These developments have affected the outlook Americans have for their future incomes. Survey data suggests that earnings growth is foreseen to be much lower than was the case prior to the 2008 recession. Research has demonstrated that long-term earnings expectations have an important influence on today’s consumption, so this is not encouraging for sales.

The loss of home equity, modest income expectations and the approach of retirement for the postwar generation has led families to become somewhat more frugal. The U.S. saving rate, which hit a low of 2% in 2005, is approaching 6% today. To many, this is a welcome and overdue development. But it also suggests fewer presents under the tree.  In aggregate then, the fundamentals for U.S. consumer spending would appear to be very solid. But the unevenness of performance since the recession has had an important impact on how much people buy, and what they buy. Overall, sales gains of 4% to 4.5% are expected for this holiday season.

In aggregate then, the fundamentals for U.S. consumer spending would appear to be very solid. But the unevenness of performance since the recession has had an important impact on how much people buy, and what they buy. Overall, sales gains of 4% to 4.5% are expected for this holiday season.

I am not sure that my own activity will reach this standard. The output from my multivariate naughty/nice model suggests that my children are only deserving of a 1.412% increase in gift values from last year. But in the spirit of the season, and in the name of economic growth, I may try to do a little better than that.

Convergence and Divergence

The central banks of the United States and the United Kingdom have much in common at the moment. Both have completed their asset purchase programs. Both are expected to tighten their policy stance in the quarters ahead. Both have seen their deliberations watched closely for hints about the timing of any rate hikes.

Both also have governing councils with a wide range of views. The minutes of the most recent policy meetings of the Federal Reserve and the Bank of England (BoE), published earlier this week, reveal a considerable breadth of opinion. The leaders of the two institutions may be challenged to maintain consensus.

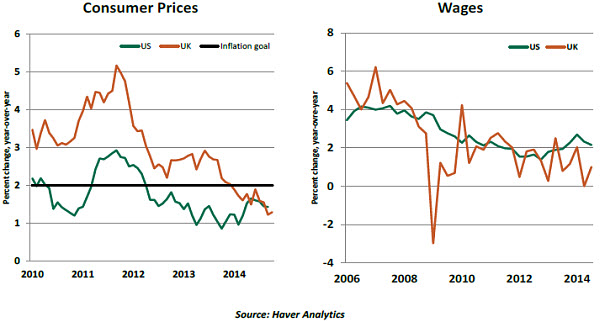

The Fed has a dual mandate of price stability and full employment, while the BoE’s remit consists of only price stability. Inflation readings at 1.5% and 1.3% in the United States and United Kingdom, respectively, are far below the 2.0% goal they share.

At its November meeting, the BoE’s Monetary Policy Committee (MPC) voted 7-2 in favor of keeping the policy rate unchanged at 0.5%. The two dissenters would have preferred to raise the policy rate 25 basis points.

Although seven members voted to stand pat, the minutes indicate that a “material spread of views on the balance of risks to the outlook” exists, as well as “materially different probabilities” attached to these risks. For some within the group, “there was a risk that growth might soften further than anticipated and inflation might persist below the target for longer than expected.” For others, the primary risk was “that the degree of spare capacity would be eliminated more quickly than assumed.”

The minutes also noted that “further increases in earnings growth would be necessary” if the central bank’s projections for output and inflation were to be realized. Average weekly earnings in the United Kingdom grew only 1.0% in the third quarter. Looking ahead, the significant pool of part-time workers and long-term unemployment in Britain will play a role in delaying wage acceleration. In light of this, the overall tone of the minutes suggests the MPC is in no rush to increase the policy rate.

At its October meeting, the Federal Open Market Committee (FOMC) voted to hold the federal funds rate unchanged and terminated its asset purchase program on schedule. Only one member dissented in favor of a more accommodative monetary policy.  The minutes of the FOMC meeting indicate a lengthy discussion about the pledge to “maintain the 0 to ¼ percent target range for the federal funds rate for a considerable time following the end of its asset purchase program.” Some members favored removal of the “considerable time” language, but others were fearful that it would signal a more significant shift in policy than might be intended. The active debate over this phrase will likely resume at the year’s final FOMC meeting next month.

The minutes of the FOMC meeting indicate a lengthy discussion about the pledge to “maintain the 0 to ¼ percent target range for the federal funds rate for a considerable time following the end of its asset purchase program.” Some members favored removal of the “considerable time” language, but others were fearful that it would signal a more significant shift in policy than might be intended. The active debate over this phrase will likely resume at the year’s final FOMC meeting next month.

FOMC participants expect inflation to move toward the Fed’s 2.0% target “in coming years,” after being held down by lower energy prices and other factors in the near term. A few expressed concern that inflation may linger below the target for some time. An extended debate about inflation expectations concluded with the assessment that they remain well anchored. It was decided that “the Committee should remain attentive to evidence of a possible downward shift in longer-term inflation expectations.”

Economic weakness abroad and the dollar’s strength were seen to have a limited effect on the U.S. economy. The FOMC minutes also included discussions about the Fed’s exit strategy, with members suggesting more communication about the path of interest rates after the first hike, as opposed to a sole focus on the timing of the first hike.

Both the Fed and the BoE are close to reducing policy accommodation. Within both, proponents of higher rates fear inflation, while advocates of steady policy worry about the consequences of premature tightening. For now, the latter has the upper hand in both realms.

But both could be facing tests of governance and communications as incoming data feeds alternative views of the outlook. Maintaining a unified front while allowing for healthy give-and-take behind the scenes will remain a transatlantic challenge.

Stronger, But Not Strong

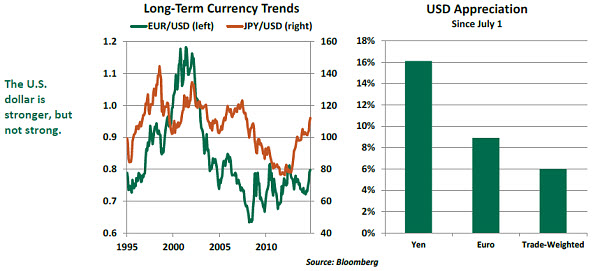

The value of the U.S. dollar has been in the news quite a bit lately. At the same time the Fed was ending its asset purchases, central banks in Europe and Japan have been accelerating their quantitative easing. This combination has caused an appreciation in the greenback.

Nations around the world are hoping that this will facilitate exports to the United States, still seen as the world’s consumer of last resort. On the other side of this trend, some have wondered whether U.S. exports could be unduly impeded, and lead the Secretary of the Treasury to take corrective action. Neither is likely, however, because the dollar really is not that strong.

To gauge the standing of a currency, it is helpful to put it into two perspectives. The first is a historical one; as shown in the left-hand panel below, the dollar is at or below its 20-year averages against the yen and the euro.

The second is a global one, in which the dollar’s performance is weighted by the trade volumes the United States shares with others. (A third of U.S. exports and 26% of U.S. imports are with Canada and Mexico.) When viewed in this light, the dollar’s appreciation since mid-year has been more modest.

To be sure, recent currency market trends could be extended. But it could be a while before a stronger U.S. dollar creates a substantial impact on the terms of trade. Some contracts and hedges have locked currency values in place, buffering firms from the market’s realignment. And companies often choose to absorb some currency changes in their profit margins to keep up market share.

As a final thought, U.S. exports make up only 13% of our GDP, less than half the level seen in other developed countries. So at this point, currency realignment is unlikely to have much of an impact on American economic growth.

Recommended Content

Editors’ Picks

EUR/USD holds firm above 1.0700 ahead of German inflation data

EUR/USD trades on a firm footing above 1.0700 early Monday. The pair stays underpinned by a softer US Dollar, courtesy of the USD/JPY sell-off and a risk-friendly market environment. Germany's inflation data is next in focus.

USD/JPY recovers after testing 155.00 on likely Japanese intervention

USD/JPY is recovering ground after crashing to 155.00 on what seemed like a Japanese FX intervention. The Yen tumbled in early trades amid news that Japan's PM lost 3 key seats in the by-election. Holiday-thinned trading exaggerates the USD/JPY price action.

Gold price bulls move to the sidelines as focus shifts to the crucial FOMC policy meeting

Gold price (XAU/USD) struggles to capitalize on its modest gains registered over the past two trading days and edges lower on the first day of a new week, albeit the downside remains cushioned.

Ripple CTO shares take on ETHgate controversy, XRP holders await SEC opposition brief filing

Ripple loses all gains from the past seven days, trading at $0.50 early on Monday. XRP holders have their eyes peeled for the Securities and Exchange Commission filing of opposition brief to Ripple’s motion to strike expert testimony.

Week ahead: FOMC and jobs data in sight

May kicks off with the Federal Open Market Committee meeting and will be one to watch, scheduled to make the airwaves on Wednesday. It’s pretty much a sealed deal for a no-change decision at this week’s meeting.