Waking up the giants

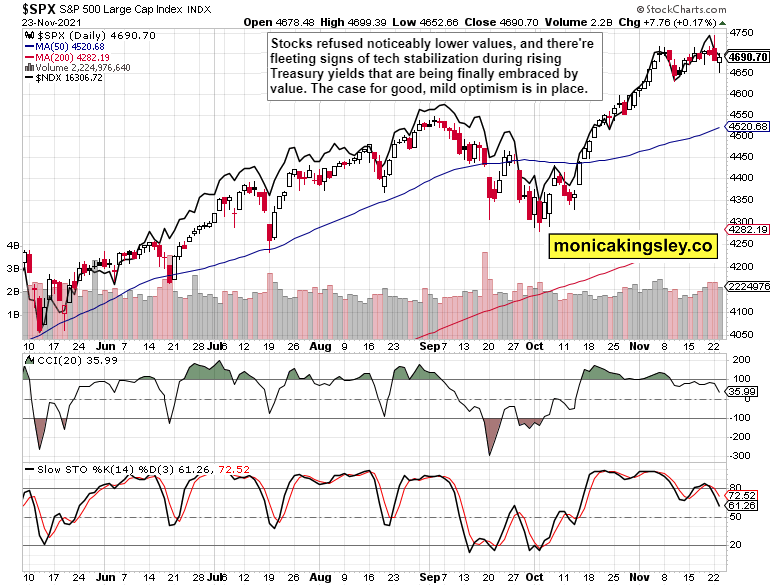

S&P 500 recovered from session lows, and is likely to keep chopping around in a tight range today. Tech found solid footing in spite of sharply rising yields, which value (finally) embraced with open arms. The riskier end of credit markets doesn‘t yet reflect the stabilization in stocks, which is a first swallow. Make no mistake though, the fresh Fed hawkish talking games are a formidable headwind, and animal spirits aren‘t there no matter how well financials or energy perform. These are though clearly positive signs, which I would like to see confirmed by quite an upswing in smallcaps. All in all, this is still the time to be cautiously optimistic, and not yet heading for the bunker – that time would probably come after the winter Olympics (isn‘t it nice how that rhymes with the post 2008 summer ones‘ price action too?).

Market reaction to today‘s preliminary GDP data will likely be a non-event, and we‘ll still probably make fresh ATHs before stocks enter more turbulent times. In spite of the cheap Fed talk still packing quite some punch, let‘s keep focused on the big picture and my doubts as to the Fed‘s ability to carry out the taper, let alone (proactive? No, very much behind the curve) rate raising plans – as said the prior Monday or yesterday:

(…) The Fed is still printing a huge amount of money on a monthly basis, and it remains questionable how far in tapering plans execution they would actually get – I see the risks to the real economy coupled with persistently high inflation as rising since the 2Q 2022 (if not since Mar already, but most pronounced in 2H 2022.

(…) True, the bullish argument for the dollar stepped to the fore as yields differential between the U.S. and the rest of the world got more positive, and at the same time, various yield spreads keep compressing. That‘s a reflection of less favorable incoming economic data. Just as much as Friday‘s reaction was about corona economic impact projections, yesterday‘s one was about monetary policy anticipation.

Inflation expectations though barely budged – the decline doesn‘t count as trend reversal. CPI isn‘t done rising, and the more forward looking incoming data (e.g. producer prices) would confirm there is more to come. All in all, it looks like precious metals (and to a smaller degree commodities), are giving Powell benefit of the doubt, which I view to be leading to disappointment over the coming months. Should Powell heed the markets‘ will, the real economy would weaken dramatically, forcing him to make a sharp dovish turn – and he would, faster than he flipped since getting challenged in Dec 2018.

Inflation expectation indeed held up during the day, marking modest, lingering doubts about Fed‘s ability to execute. Its credibility isn‘t lost, but would be put to a fresh test over the nearest weeks and months. The real economy can still take it, and not roll over – we are in the very early tapering stage so far still. Commodities are pointing the way ahead, and it‘s time for precious metals to shake off the inordinately high levels of fear, which mark capitulation more than anything else. Just when I was writing that it‘s as if the PMs bulls didn‘t trust the latest rally...

Let‘s move right into the charts.

S&P 500 and Nasdaq outlook

S&P 500 bulls stepped in, the volume is semicredible. I like the lower knot, and would look for increasing market breadth to confirm the short-term reversal. It‘s my view we haven‘t made a major top on Monday.

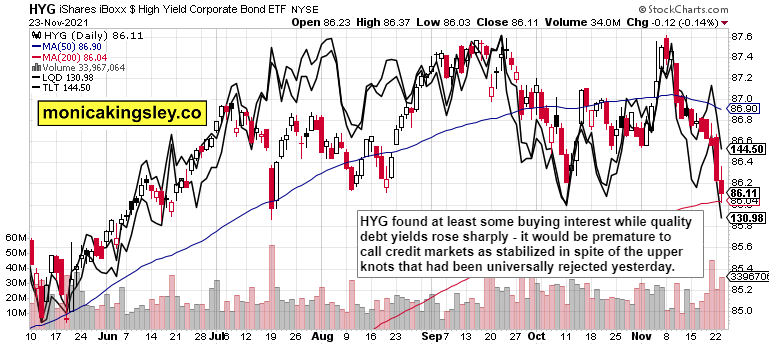

Credit markets

It‘s too early to call a budding reversal in credit markets – HYG needs to pull its weight better.

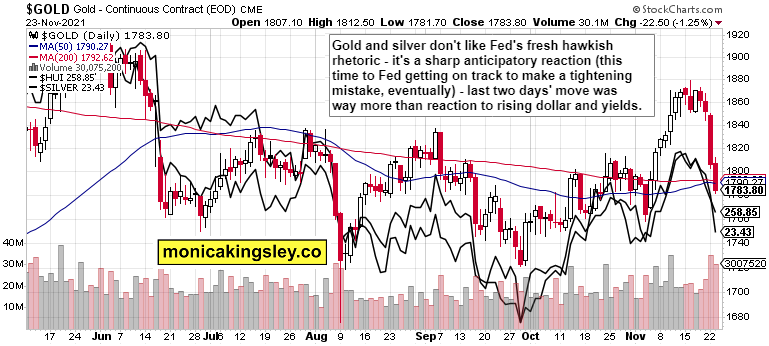

Gold, silver and miners

Precious metals haven‘t yet regained footing, but that moment is quickly approaching – in spite of the above bleak chart. Compare to the Jun period – Fed‘s talk was more powerful then.

Crude oil

Crude oil bulls have made a good move, and more strength did indeed follow. The bottom is in, and many countries tapping their strategic reserves, proved an infallible signal. I look for consolidation followed by further strength next.

Copper

Copper springboard is getting almost complete, and I think the drying up volume would be resolved with an upswing. The daily indicators are positioned as favorably as the CRB Index is.

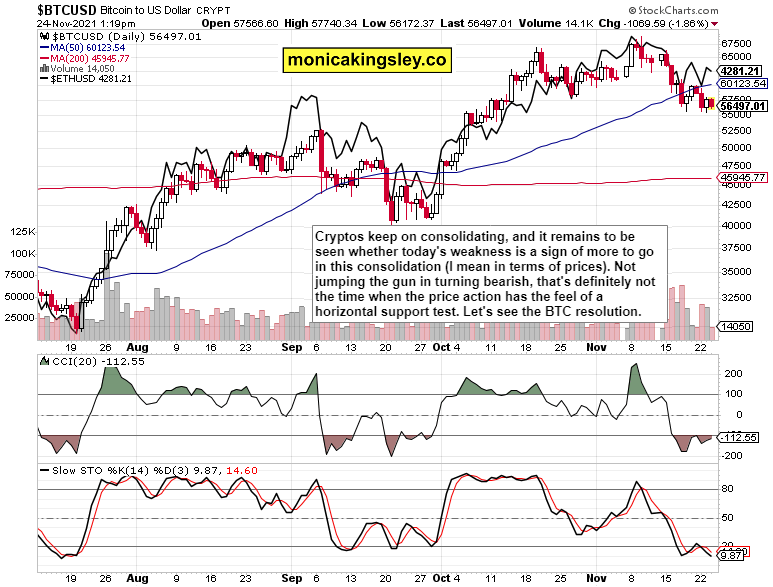

Bitcoin and Ethereum

Bitcoin and Ethereum are still correcting, and the upcoming Bitcoin move would decide the direction over the next few weeks. The takeaway from cryptos hesitation is that real assets can‘t expect overly smooth sailing yet.

Summary

S&P 500 bulls would ideally look to value outperforming tech on the upside, confirmed by HYG at least stopping plunging. A brief yields reprieve would come once the Fed steps away from the spotlight, which is another part of the bullish sentiment returning precondition set. Overall, the very modest S&P 500 moves keep favoring the bulls within the larger topping process. Keep in mind that the Fed isn‘t yet in a position to choke off the real economy through slamming on the breaks, it‘s just the forward guidance mind games for now. We are waiting for the bit more seriously than last time meant, but still a bluff, getting questioned again, as inflation expectations haven‘t broken down, and are facilitating the coming PMs and commodities runs.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.