US Service Sector September PMI Preview: How slow is slow?

- Service sector sentiment expected to fall in September

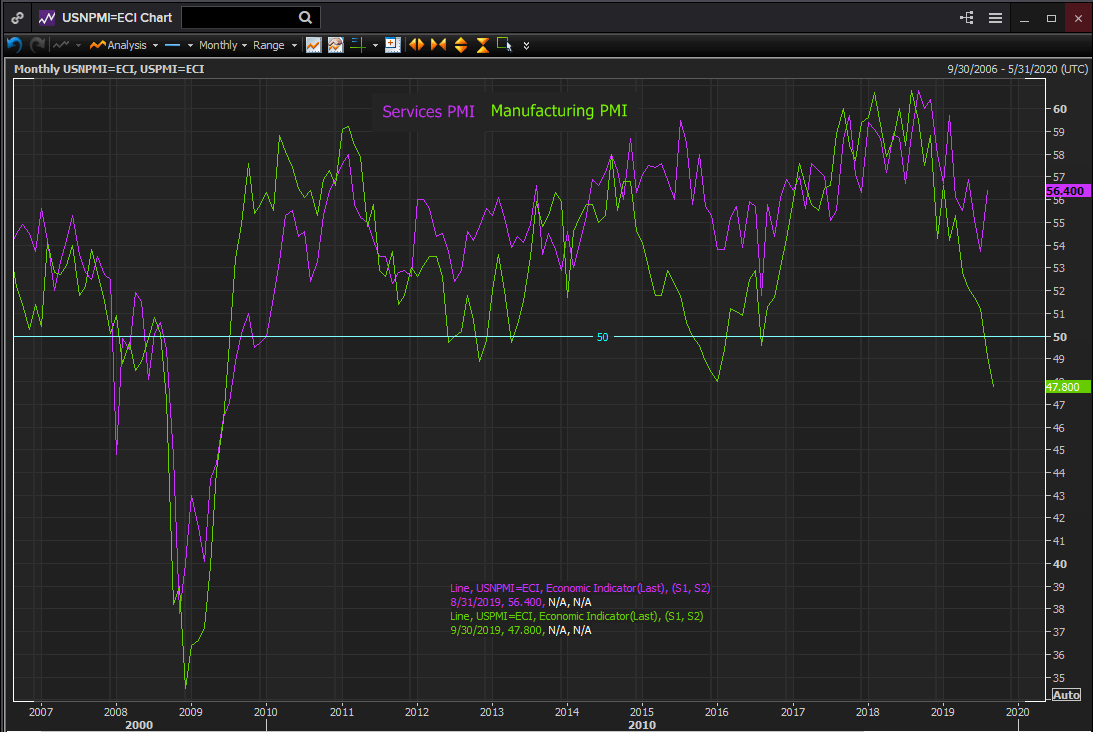

- Manufacturing PMI was much weaker than predicted, contracting for the second month

- Payrolls have declined but remain in solid expansion

The Institute for Supply Management (ISM) will release its Non-Manufacturing Purchasing Managers' Index (PMI) for September at 10:00 am EDT, 14:00 GMT Thursday October 3rd.

Forecast

The overall PMI is predicted to fall to 55.1 in September from 56.4 in August. The business activity index is expected to decrease to 59.1 from 61.5. The new orders index was 60.3 in August and 54.1 in July. The employment index was 53.1 in August and 56.2 in July. The prices paid index was 58.2 in August and 56.5 in July.

The US economy and business sentiment

After falling for more than a year the decline in the US manufacturing purchasing managers’ index moved into contraction in August and further below the 50 division in September.

The question for the markets is will the far larger service sector follow and pull the US economy into recession?

Reuters

At about 15% of the US economy a recession in the manufacturing sector alone will not place the overall economy into contraction. Though business sentiment among factory executives is generally considered a leading indicator for the economy it can provide false signals as well.

Manufacturing PMI has fallen below 50 twice since the recession, in November and December 2012 and for five months from October 2015 to February 2016. In neither instance did the service sector follow nor did GDP turn negative.

The US China trade dispute is the major cause of the year long decline in manufacturing sentiment. Export orders have fallen and business investment has been postponed pending a resolution. While the sector itself is about one-sixth of US GDP, because of the capital intensive nature of factory production its business spending has a disproportionate impact on economic activity.

The drop in business investment is one of the primary reasons for the drop in US GDP in the second and third quarters.

Consumer sentiment, retail sales and the labor market

The consumer side of the US economy has remained healthy throughout the collapse in manufacturing sentiment.

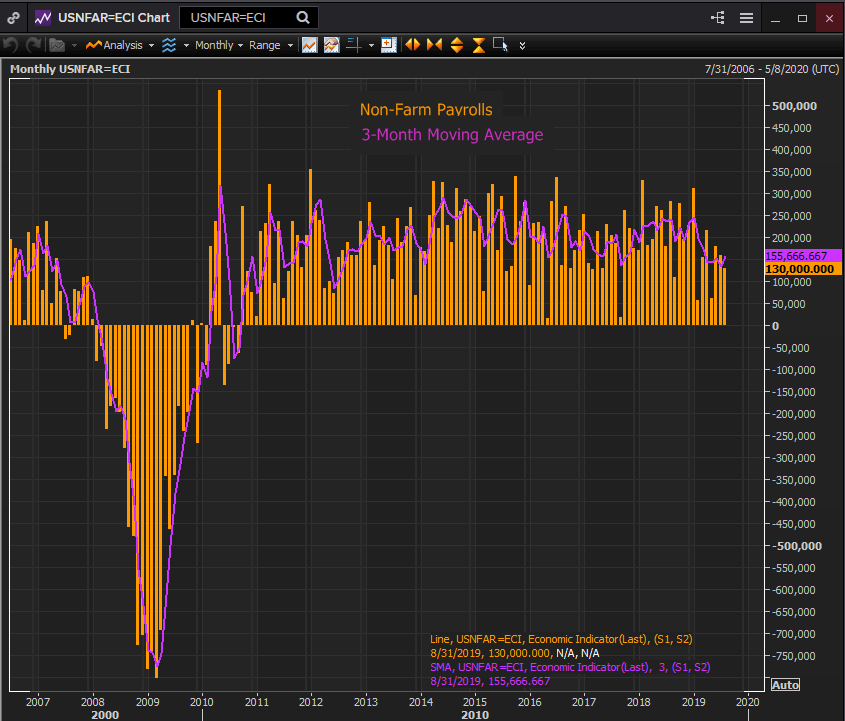

Monthly payrolls have fallen about 100,000 in the three month moving average from January to August from 257,000 to 156,000. But that drop is a function of the very high levels of job creation last year. It is not a sign that the labor economy is beginning to falter.

Reuters

At the August average the economy is still producing more jobs than new workers and when combined with the surplus of unfilled positions from the last two years, the help wanted signs and the pressure on wages have remained steady.

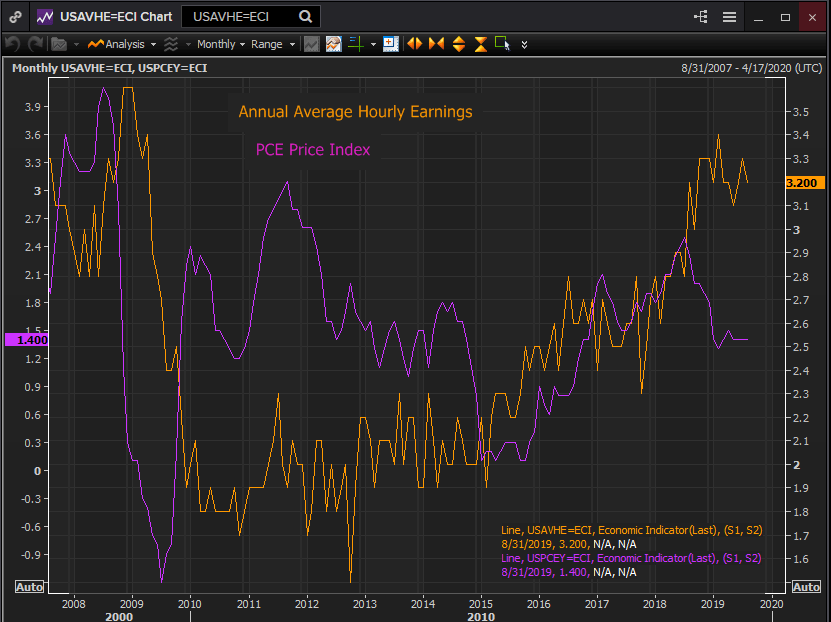

Average annual earnings have risen 3% or more annually for 13 months and are expected to do so in September. With the PCE price index falling over the past year to 1.4% consumers have opened a sizable increase in disposable income.

Reuters

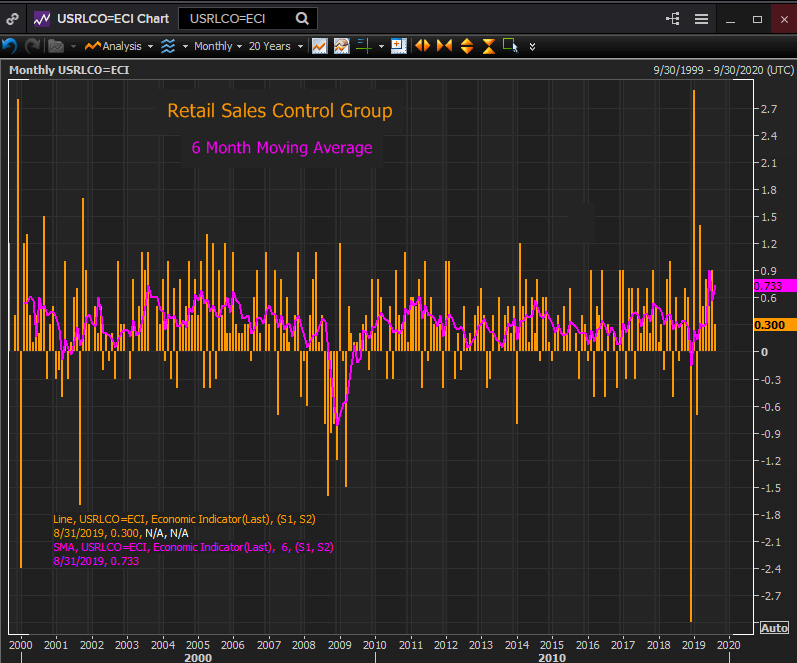

Retail sales have responded to this confidence with consumers spending for the last six months at the fastest pace in 16 years.

Reuters

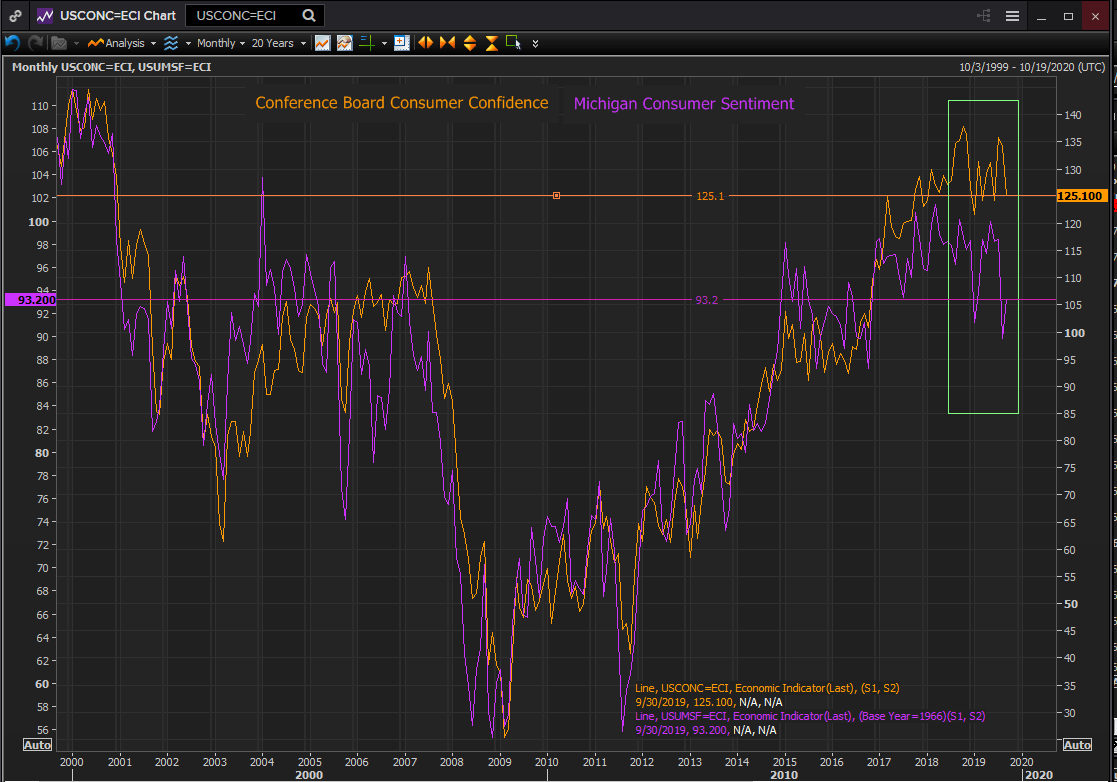

Consumer sentiment in the Conference Board and Michigan Surveys has dropped sharply in August and September, falling to the bottom of the range for the last two years. But even at that level its remains above the vast majority of reading for both polls over the last two decades.

Reuters

Conclusion

The US economy is being carried by consumer spending. The most important component of the near historic levels of consumer confidence over the last three years has been the excellent and continuing performance of the labor market.

Direction and sentiment in the services sector is derived from the consumer economy. With jobs, wages and spending yet plentiful it is unlikely that the confidence of the sector will fade substantially while the consumer is still rampant.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.