US Retail Sales Preview: Return to spender

- Retail sales expected to return to growth after a disappointing April

- Wage increases remain strong, but payrolls have slipped in the last four months

- Positive consumer sentiment and spending caution not incompatible

The US Census Bureau will release its advance Monthly Sales for Retail and Food Services for May at 8:30 am EDT, 12:30 GMT on Friday June 14th.

Forecast

Retail sales are expected to rise 0.6% in May after falling 0.2% in April. Sales excluding automobiles are forecast to gain 0.3% after the April 0.1% increase. The control group, sales minus building materials, motor vehicles and parts and gasoline and food service receipts, which is used to calculate the personal consumption expenditure component of GDP, is predicted to rise 0.4% after a flat April.

Retail Sales, economic growth and the labor market

Economic growth in the US has, according to the Atlanta Fed’s GDPNow model, slowed appreciably in the second quarter. From 3.1% annualized January through March, the Atlanta track is but 1.4% in April and May, which includes statistical releases thought June 7th.

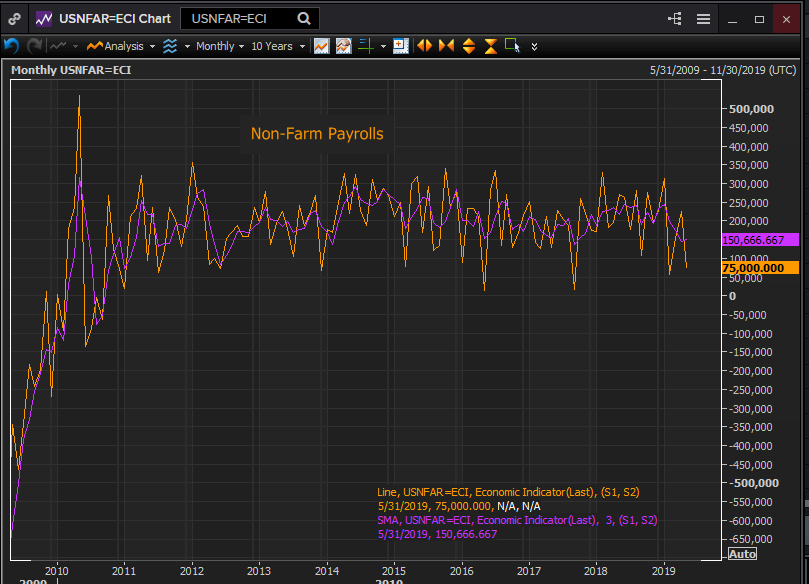

Non-farm payrolls have also diminished with the 3-month moving average declining from 245,000 in January to 173,700 in March and 150,700 in May with two less than 100,000 results in the last four months.

Reuters

The unemployment rate has continued at its 50 year low of 3.6%. Likewise initial jobless claims at 215,000 in the 4-week moving average at the end of May give no indication of pending layoffs.

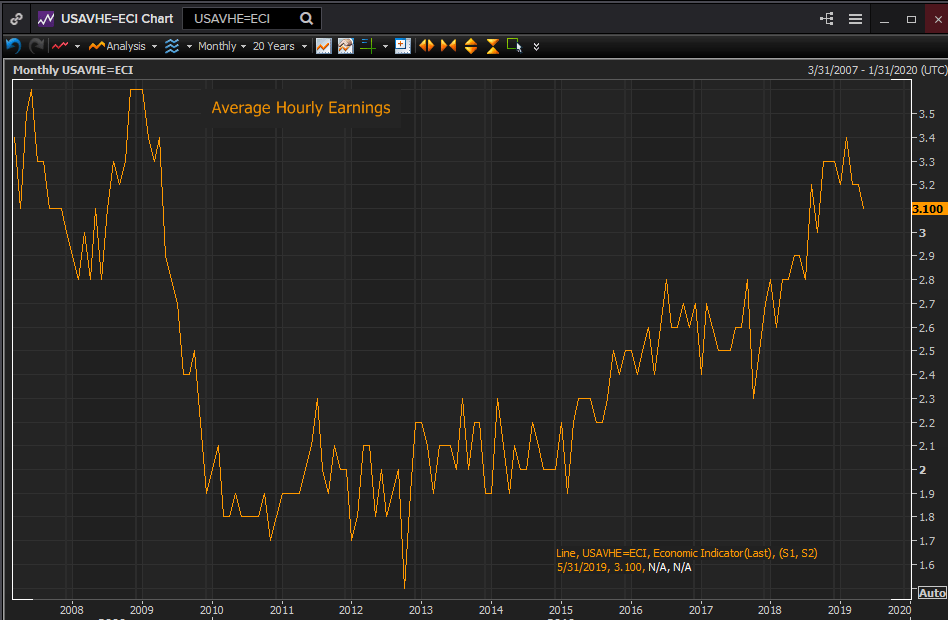

Average hourly earnings over 12 months maintained their near decade high at 3.1% in May.

Reuters

Business Employment Sentiment

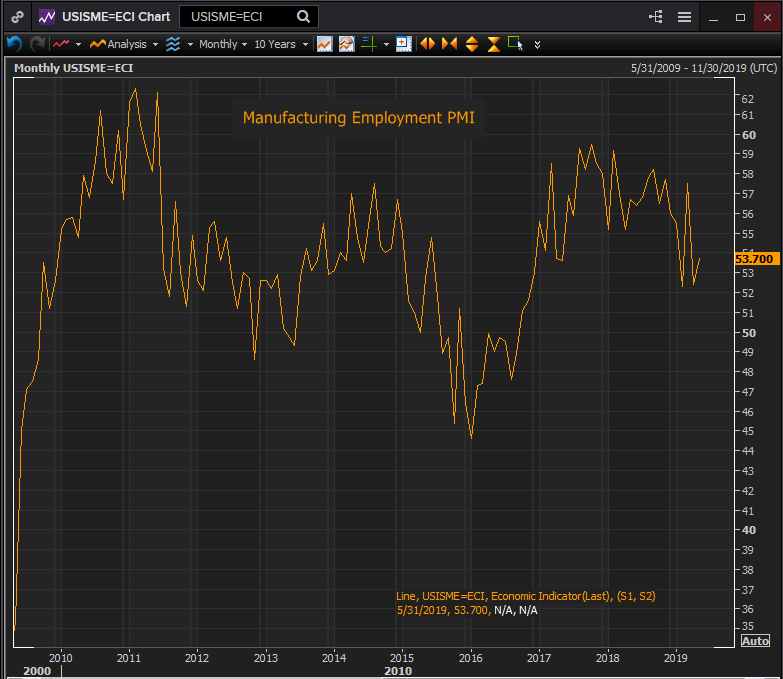

Business optimism in the service sector over hiring and employment recovered sharply to 58.1 in May after declining for almost seven months. Attitudes in the manufacturing sector also rebounded though at 53.7 they are at a lower level.

Reuters

Consumer Sentiment

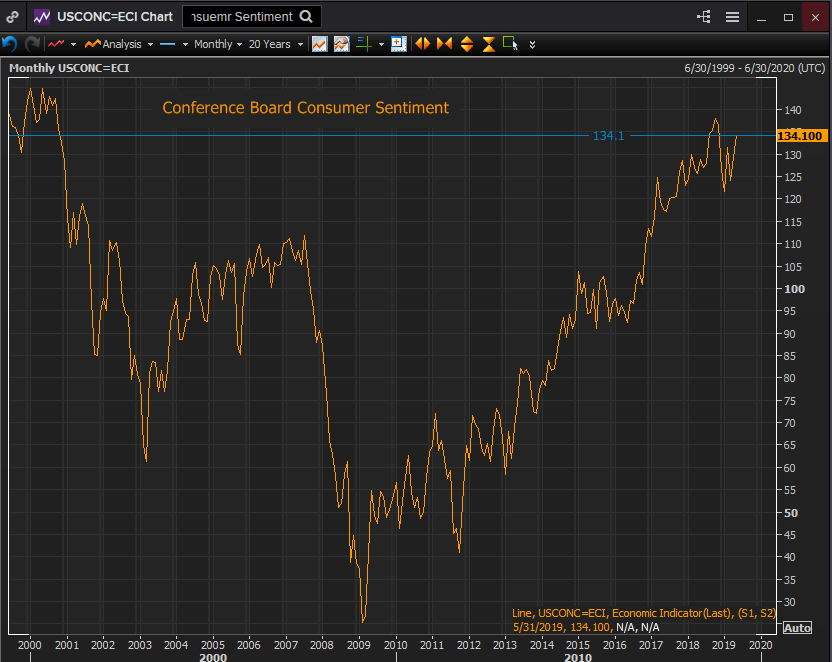

The University of Michigan Sentiment Index preliminary reading for May at 102.4 was a 15 year high. The revision to 100 is not a record but still among the highest scores of the past decade. The Conference Board Survey climbed to 134.1, with exception of August, September, October and November last year that is the highest reading since November 2000.

Reuters

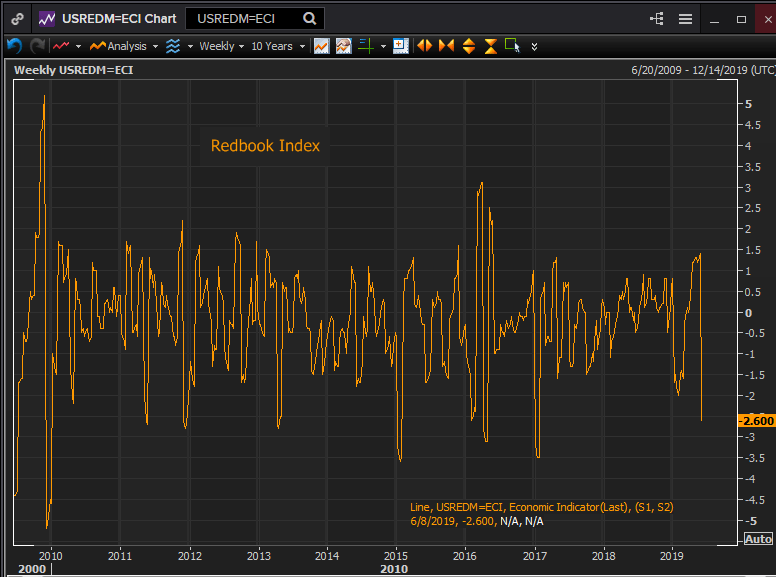

Redbook Index

This index tracks changes in consumer purchases based on same store sales in about 9,000 general merchandise outlets, representing about 80% of the Census Bureau’s retail base.

Weekly sales plummeted 2.6% in the latest reporting in June the largest one week decline since early February 2017. This is a normally volatile series with regularly occurring plunges and recoveries.

Reuters

Conclusion

Employment and wages, even with the weak results in payrolls in two of the last four months, are at robust levels of job creation and remuneration.

Employers seem to have recovered some of their prior optimism and this should work to return payrolls to the footing of the last two years rather than the last four months.

The Fed has been fretting about the effects of various global conditions on the US economy since January even though it has until very recently not shown any sign or inclination of retreat.

The major determinants of consumer spending, employment and wages remain buoyant and the surveys of consumer sentiment indicate a very pleased electorate. Judging from the coincident indicators consumers should return to the stores in May.

But consumption is not a linear function and there are also plenty of reasons for consumers to be wary of where the economy may be headed. The potential impact of the still unsolved China and Brexit conflicts may be enough to restrainthe evident optimism.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.