US October Durable Goods Orders Preview: The revival in business investment is not yet in sight

- Durable goods orders expected to fall for the second month.

- Non-defense capital goods to spending to shrink for the third month.

- Ex-transport orders predicted to rise in the report’s only positive.

The US Census Bureau will release its Manufacturers New Orders for Durable Goods for October on Wednesday November 27th at 13:30 GMT, 8:30 EST.

Forecast

Durable goods orders are predicted to drop 0.8% in November after falling a revised 1.2% in October. Orders ex-transport are expected to rise 0.2% following October’s revised 0.4% decline. Orders-ex defense are projected to fall 0.3% in November after the prior month’s revised 1.3% drop. Non-defense capital goods orders ex-aircraft and parts, a proxy for business investment, is forecast to fall 0l3% after October’s 0.6% revised decrease.

Durable Goods

Durable goods are retail items designed to last three years or more in normal use. Automobiles and air conditioners qualify, but so do lawn chairs, kitchen knives, inflatable mattresses and bicycles.

Business purchases run from copiers and computers that might be replaced every few years to semi-permanent capital investments like commercial aircraft and construction equipment. Government procurement from aircraft carriers to imaging software and office furniture falls under the rubric as well.

The longer lifespan of these goods entails a somewhat different economic analysis for purchase and use, especially for businesses which amortize the cost over the productive cycle.

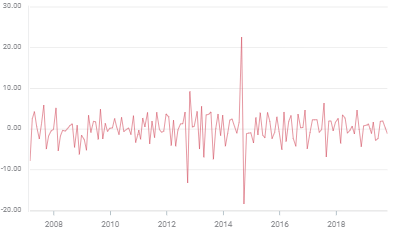

Durable goods orders have averaged -0.16% monthly year-to date, non-defense capital goods have averaged 0.11% but they have fallen in August and September.

Durable goods

Retail sales

Retail sales rose 0.3% last month reversing September’s 0.3% decline, which was the first in seven months. Overall sales have averaged a 0.54% monthly gain this year but only 0.2% in August, September and October.

The control group also increased 0.3% in October improving from -0.1% in September. Purchases in this category, which are the consumption component of the Bureau of Economic Analysis’ GDP calculation, have averaged a 0.56% this year, though only 1.67% in the last three months.

It is the recent weakness in the overall retail figures and the control group which are predictive of the expected declines in the durable goods categories in November. Retail sales in November are viewed as an indicator for the holiday season will be reported on Friday December 13th

Labor Market

The long-running energy of the labor market has been the major factor in the strong retail sales this year.

Payrolls and very low jobless rate have been underpinning consumption for three years but it was probably the 3.0% and higher monthly increase in annual wages over the past 15 months and a drop in inflation that translated directly into disposable income that had the most direct impact.

Non-farm payrolls averaged 176,000 in August, September and October and 174,000 a month on the year through October. These figures are down from the exceptionally strong 235,000 and 245,000 January numbers but they remain well above the 125,000-150,000 new workers entering the job market each month. This should add to the backlog of unfilled positions that has been building over the past three years and keep upward pressure on wages.

The 3.6% unemployment rate in October is 0.1% from a five decade year low and the jobless rates for African-Americans and Hispanics are the smallest ever recorded.

November’s consensus estimates of 183,000 for payrolls, 3% for annual wages and 3.6% for unemployment and the likely continuation of job growth into the first quarter of 2020 should continue to support retail sales.

Consumer sentiment

American consumer attitudes have recovered smartly from their government shutdown inspired plunge in December and January.

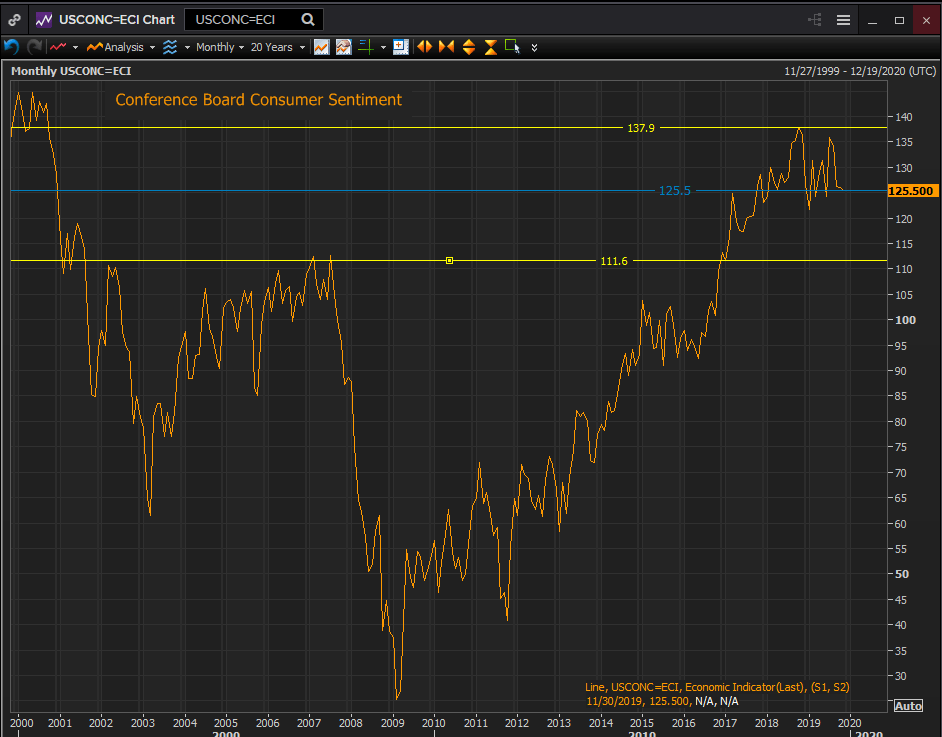

The Conference Board Consumer Sentiment Index registered 125.5 in November, slightly less than the 127.0 forecast and off from 126.1 in October.

Confidence in October was very close to the mid-point of the 111.6 to 137.9 range from January 2017 to the present though on the low side of the spread from January 2018 onwards. However, the November figure of 125.5 is better than every score prior from the sixteen plus years from January 2001 to October 2017.

Reuters

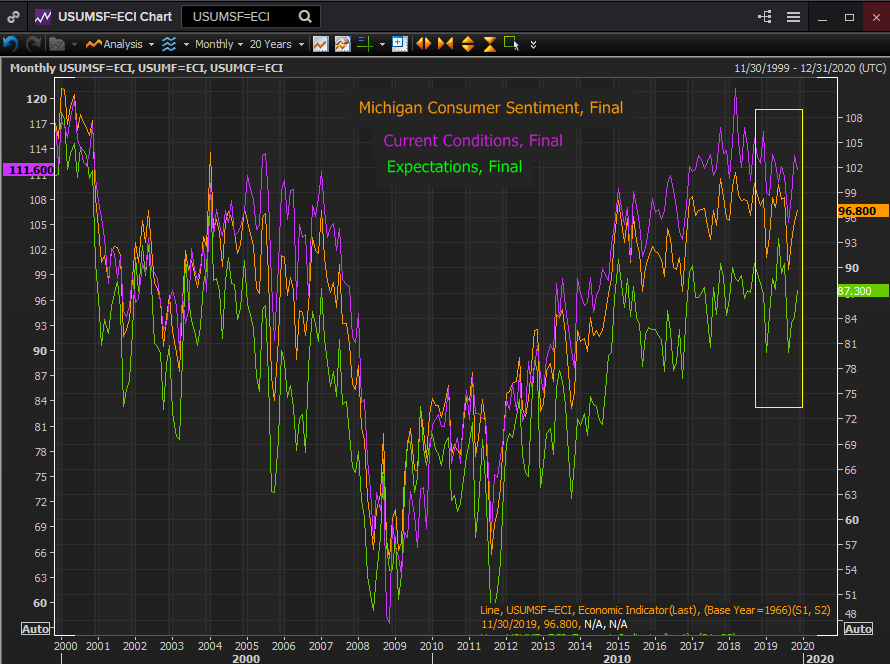

Likewise the University of Michigan Survey of Consumer Sentiment Index level of 96.8 in November places squarely in the highest reaches of the past two decades though at the lower end of the scores of the last three years.

Reuters

As with retail sales it is the extraordinary labor market that has had the largest positive impact on consumer sentiment.

Business spending

The two year old trade war with China has put a large dent in business investment. The 12-month moving average for non-defense capital goods peaked in July 2018 at 0.758%. It has declined steadily since as businesses have decided to wait out the negotiations before sanctioning new investment and averaged just 0.186% in the third quarter the weakest three month period in over a year.

Reuters

Conclusion: Federal Reserve and the dollar

The pending US China trade deal announced on October 13th may be one of the developments that persuaded the central bank to return to a neutral policy stance.

The economy through the third quarter maintained a 2% growth rate though slipping below 1% in most 4th quarter estimates. Labor market concerns from earlier in the summer have proved to be transitory.

Business spending has not yet recovered but if the agreement between the US and China is signed by President’s Trump and Xi that would be anticipated in the first half of 2020

The dollar will benefit as returning business investment will push GDP towards 3% in the first quarter. With the ECB still providing monetary accommodation through bond purchases and the fears for a global trade war diminishing, currency markets will likely jump start the dollar in the New Year.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.