Tax reform is not going to boost growth by much

Outlook:

We do not like to admit it, but TreasSec Mnuchin is right to say the market will take in stride any signs of wage inflation and a higher public debt burden. He told Bloomberg "There are a lot of ways to have the economy grow. You can have wage inflation and not necessarily have inflation concerns in general." We have had bouts of excessive debt before, and the buyers keep coming.

A week away from a narrow focus is a fine thing. We read newswires for the first time last night and a blinding insight come thundering through. At least we hope it's an insight. Here it is: the US is not going to get much wage inflation or inflation in general, and is fact is likely to see inflation contained at or be-low 2.00-2.25% for the foreseeable future. One factor reining it in is oil, which "should" be priced far lower than $65. But the Fed is still going to unload paper from its QE days, masses of it, and rates will be going up in March and then at least one more time this year, if not two.

Rising rates in the absence of scary inflation data is normalization on drugs. In fact, it's the best possible scenario for the Fed, because now it can sound cheery and hawkish at the same time while in the back-ground, the supply of Treasury paper to fund the Trump deficit will keeps rising, suppressing yields in the belly of the curve as well as the long end.

Reports on the Fed minutes from Yellen's last policy meeting universally report the Fed feels increas-ing confident about the health of the US economy and some see the 2% inflation target hit in no time at all. The WSJ reports markets "gyrated" Wednesday on release of the minutes. "Investors appeared to initially welcome the Fed minutes, relieved that they didn't signal the central bank was poised to ramp up its tightening efforts. But stocks and bonds fell after it became clearer the Fed might move more aggressively than anticipated later this year." Here's the key sentence: "A majority of participants noted that a stronger outlook for economic growth raised the likelihood that further gradual policy firming would be appropriate."

To be fair, many analysts agree that tax reform is not going to boost growth by much, because compa-nies are populated by selfish bastards who will pay themselves and shareholders before paying workers or making capital investment. This will probably be true at the beginning, by which we mean this year and into Q1 next year, but at some point, authentic skilled labor shortages and strained capacity will deliver higher wages and capital investment. It could actually be a boom (and three guesses who will claim credit for it).

So, we could start out with a soft landing but as the year progresses, a boom would scare the Fed. It would also scare the stock market. The Fed know this. The FT picks out from the minutes this tidbit: "FOMC members considered market valuations at that point to be ‘elevated' and the product of ‘broad-based appetite for risk among investors.' Some members cautioned that the Fed should be careful that ‘imbalances in financial markets may begin to emerge' as growth improves, and that the central bank also should monitor financial stability particularly against the prospects for lowered regulations." What happened Wednesday can likely be repeated and repeated and repeated. "After an initially muted reaction, the benchmark 10-year Treasury yield rose 5 basis points to 2.94 per cent. The sell-off in bonds was accompanied by a sharp move lower in the stock market, with the S&P 500 erasing its 1.2 per cent gain — reached after the minutes were released — to trade down 0.4 per cent at 2,705. Real yields on the 10-year Treasury, which subtract for inflation, rose to their highest level since September 2013, indicating that investors anticipate rising interest rates in spite of moderate inflation expecta-tions."

NY Fed chief Dudley has said repeatedly that equity market gyrations will not change the Fed's trajec-tory. This doesn't mean the Fed is not watching. "Given the high asset valuations at the time of the meeting — the US stock market set a new record the previous week — several officials cautioned that ‘imbalances' in financial markets might begin to emerge as the economy operates above potential. ‘Increased use of leverage by non-bank financial institutions might be difficult to detect in a timely manner,' Fed policymakers noted."

So, whether we have a stock market bubble or not, we should probably expect repeated new mini-crashes as the year progresses. This doesn't necessarily favor the dollar, as it did so far this year. The inverse correction of the S&P and the dollar index is there, but it's unreliable and inconsistent.

What is more important is real yields starting to reflect real conditions. And real yields are only about 1%, which is inconsistent with a cheery and aggressive Fed and an improving, perhaps booming, economy.

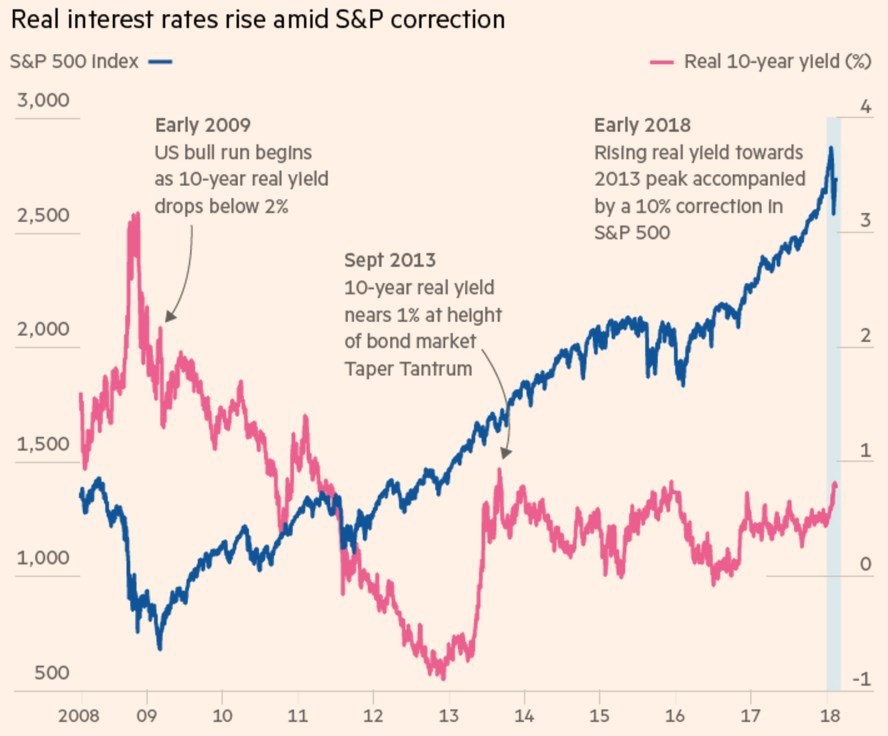

We are not even close to real yields going where they need to go. The FT wisely shows that high-growth equities, the equity market darlings for the past few years, are about to get come competition. "The 10-year real yield loiters around 0.8 per cent, up from 0.44 per cent at the start of the year and within sight of September 2013's peak of 0.92 per cent seen at the height of the bond market taper tan-trum. Importantly for equity market investors, 10-year real yields have not yet broken out of their longstanding range. During a long period of very low real yields, which has reflected lacklustre eco-nomic growth prospects, equities have been the asset class to own, led by tech. Hence the importance for broader markets if real yields take another leg higher, should bond traders demand a higher risk pre-mium that reflects the prospect of higher real growth expectations and the risk of a more active Federal Reserve."

Bravo.

If the outlook is as the Fed and analysts agree, real yields have justification to move higher—a lot high-er. They have been rangebound for five years. See the first chart. Granted, you have to get some real inflation—wages, commodities, capacity constraints—for the real yield to move. That's not going to happen for some months and can be interrupted and derailed by any number of thing, including war. But when the general market sentiment moves in that direction—boomy economy, rising inflation, higher nominal and real yields, the stock market had better look out. We are not even close, but the cost of speculation in equities is about to go up, way up. See the second chart. These two lines need to be brought back into sync, and it will not be a pretty picture.

Does the dollar benefit from this scenario? Maybe. It depends on how the eurozone economy performs (not so hot on recent data like IFO) and how strong is the resolve of Mr. Draghi to emulate the US in normalization. He has a bunch of zombie banks with nonperforming loans to worry about that the US did not have (or took care of), so there could be quite a delay, as he has already suggested. Never mind—if traders think they hear a whisper of a suggestion of ending ECB QE, they will pounce. We get another COT report this afternoon that might be fun.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes. To see the full report and the traders’ advisories, sign up for a free trial now!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat