US Fourth Quarter GDP Preview: The fourth quarter marks time

- Economic growth expected to be stable for the third quarter in a row.

- Business investment remains below par, sentiment has improved.

- Consumer spending is healthy backed by the labor market.

The Bureau of Economic Analysis, a division of the Commerce Department will release its preliminary estimate for annualized gross domestic product (GDP) for the fourth quarter on Thursday January 30 at 13:30 GMT, 8:30 EDT.

Forecast

Annualized GDP is predicted to be 2.1% in the fourth quarter. It was 2.1% in the third quarter, 2.0% in the second and 3.1% in the first.

Consumer spending, confidence and the labor market

Consumer spending slipped somewhat in the fourth quarter. The retail sales control group category that enters the Bureau of Economic Analysis’ GDP estimate averaged a 0.23% monthly gain down from 0.37% in the third quarter. The last month with robust growth was July at 0.9%. The figures for January and revisions for December will be released on February 14th.

Retail Sales Control Group

FXStreet

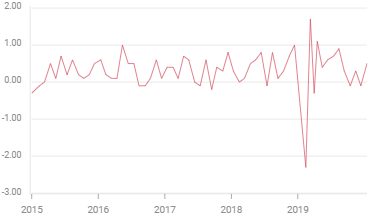

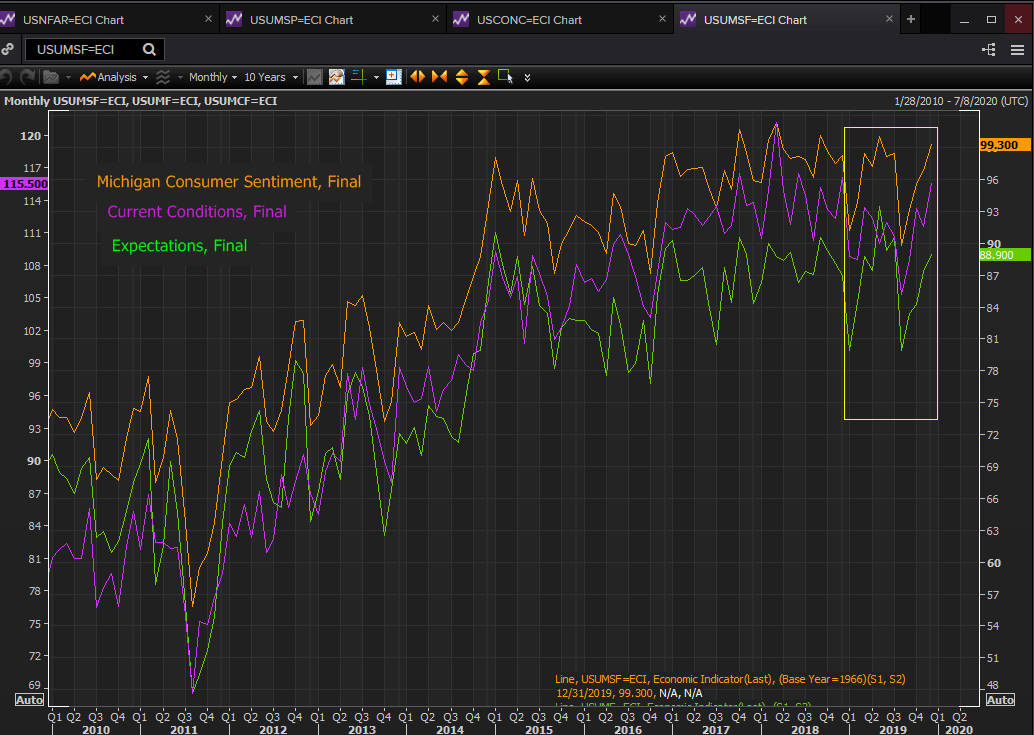

Consumer confidence climbed from its late summer plunge in August to 89.8. The third quarter average in the Michigan Consumer Sentiment Survey of 93.8 improved to 98.5 in the final three months of the year. That puts the outlook of US consumers in the top rank of the last three years and among the best scores on record for this poll.

Reuters

Payrolls edged higher in the final quarter adding 17,000 to the monthly average from 169,000 to 186,000. Though job creation has declined for 235,000 in the 12-month moving average last January to 174,000 in December this is well above labor force new entrant level and with a 50-year low in employment wages gains have remained firm.

Non-Farm Payrolls

Business confidence and investment

Brexit and the US-China trade dispute, the two great concerns of the last few years have been settled or at least their potential negative impact on the global economy have been much diminished.

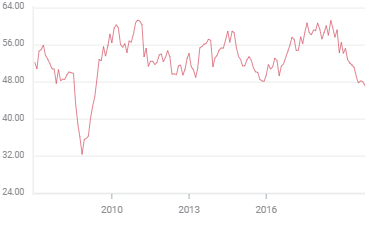

In the US the detriment has been mostly limited to the manufacturing sector with new payrolls falling from 264,000 in 2018 to 46,000. On the business side sentiment in the executive suite has been dropping since September 2018. The purchasing managers’ index from the Institute for Supply Management sank below the 50 expansion-contraction line in August and has remained there for five months. The December score of 47.2 is the lowest of the run. The employment and new orders component indexes are equally weak.

Reuters

Sentiments in the services industries, by far the larger sector have declined as well but have stayed well clear of the indicative boundary at 50.

Business investment in the second half has reflected the concerns of its managers.

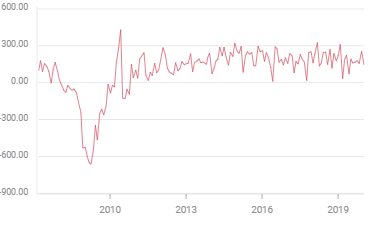

Non-defense capital goods excluding aircraft, a category of durable goods used as a proxy for business spending, dropped 0.9% in December on expectations for a flat result. The November figure was unrevised at 0.1%.

Investment was far weaker in the second half of the year averaging -0.13% per month than the initial six months which averaged 0.35%. But within the last half year there was quarterly improvement. The third quarter monthly average was -0.37% but the final three months returned to positive at 0.1%. These orders fell 1.5% in 2019 in contrast with the 0.8% gain the previous year.

China trade has been the biggest driver of negative sentiment in the manufacturing sector, its damage is cited time and again in the comments included in the ISM survey.

Conclusion

Fourth quarter GDP is marking time for the US economy. Consumer spending was lower but still expanding supported by jobs and wages and historically low levels of unemployment. Government expenditures are at near record levels enabled by trillion dollar deficits. Business investment the third general category improved slightly but remains well below its normal contribution to GDP.

The decline in consumption from the third to the fourth quarter tilts the risk to the down side for Thursday’s GDP number. The consensus estimate from the Reuters Survey is 2.1% but the Atlanta Fed’s final GDPNow estimate for the period is lower at 1.9%. Either way the rate of growth will not be far from the prior half year.

A steady US economy is priced into the dollar, and into the Fed’s economic projections though the greenback’s recent strength is somewhat susceptible to a weaker than expected GDP figure. The question trader’s will ask is--Weaker than what?

The US-China trade deal holds considerable promise for spurring economic growth in both countries though its impact, depending as it does largely on Chinese actions, may be delayed by the current health crisis in the nation. The impact may not appear in the statistics until the end of the first quarter or into the second, but it is the change markets anticipate.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.