US economy is faltering, most visible cause is Trump trade wars

Outlook:

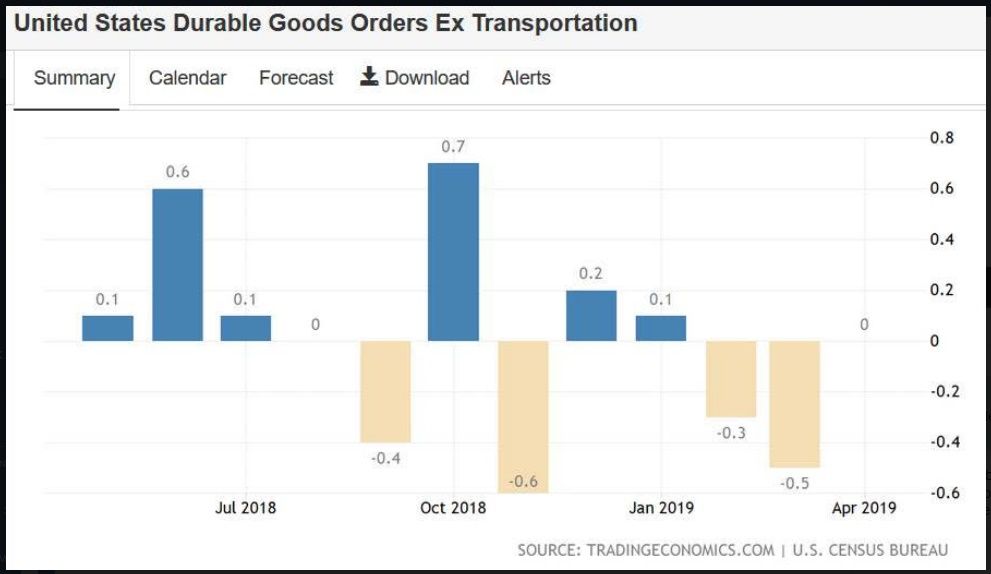

The big data today is durables, or rather durables ex-transportation, the long-accepted proxy for business investment (since actual business investment is almost impossible to capture). See the chart from tradingeconomics.com. In April durables ex-transportation were flat after falling 0.5% in March. As the chart shows, five months have been flat or negative in the past year. Another lousy number today is not exactly a tipping point, but certainly evidence for the Fed to see unfavorable outcomes developing. How much can be attributed to various Trump trade wars is not known, but doesn’t have to be. If the number is a small gain, as expected (+0.1%), it won’t necessarily help.

Bottom line: the US economy is faltering and the most visible cause is the Trump trade wars.

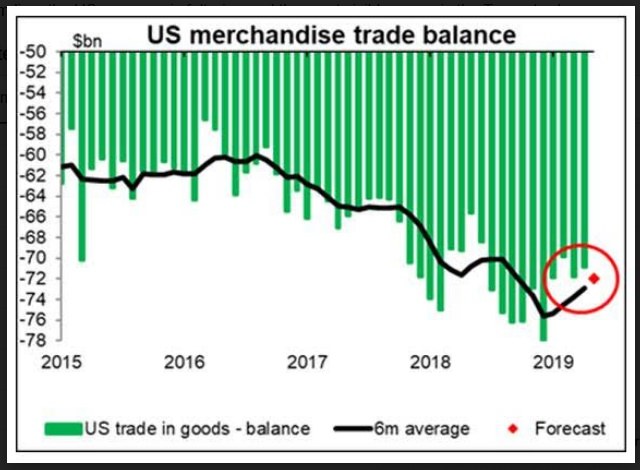

We also get something named the “advance goods trade balance,” showing merchandize but not services. Here is the chart from Gittler at ACLS. The widening deficit is negative for the US economy but not necessarily negative for the dollar if we expect Trump to dig in his heels at G20. Besides, tariffs on Chinese goods are so easily circumvented. When governments impose trade bans and costs, you get a black market. This is a hard rule from history. Today the WSJ reports Chinese goods are being shipped to places like VietNam and exported to the US from there, as though trade cheats should be a surprise. How do you think Iranians get cellphones? There’s no point in getting Miss Grundy about it, but it’s also a fact of life that folks formerly honorable will become dishonest if they face going out of business and starving their children otherwise.

As for the prospect of a China trade deal, Mnuchin’s comment this morning about being “90% there” is ridiculous and not credible. The US demands basic structural change, like a halt to subsidization of state industries, and the Chinese fully reject these demands. There is no wiggle room, not that Trump know how to make compromises, anyway. The US blacklisting additional Chinese companies—and strong-arming others (Canada) into joining it—is insulting. The US wants to “contain” China, a seriously confused effort to combine what passes for foreign affairs “policy” with economic and financial relationships. The containment idea is why analysts speak of a cold war, but that is to give the Trumpies too much credit.

Nobody knows the outcome of the G20 meeting, assuming it happens, but it’s likely China will demand a pushback to 10% tariffs and a commitment to leave the next $300 billion alone. This would be wildly favorable for everybody’s economic outlook. What China can offer to induce Trump to do that is not known. China might be able to offer something on North Korea. China might be able to commit to bigger purchases from the US. At a guess, China doesn’t have anything that will cut the mustard.

The best-case scenario is resumption of talks but after Trump makes some concessions, like the next $300 billion in tariffs off the table—to control the trade hawks, specifically Lighthizer. Since Trump breaks deals and disrepects contracts, the Chinese may not buy it. The worst-case scenario is no meeting at all, China pulling out at the last minute because it cannot trust Trump. Almost as bad is a brief meeting at which China tells Trump to start treating it respectfully or go pound sand. Xi needs, perhaps, Trump to treat him like the super-power that China really is. Would Trump bow and scrape? You bet. He needs the deal. Most analysts say the US has the upper hand. We don’t see it that way. Trump needs a deal with China to impress everyone, not only his base, that he can make deals. He pretends to be a successful deal-maker. He’s not, and everyone is starting to see that. A deal now is critical to him and less critical to Xi, who is, after all, a dictator for life. If Chinese citizens don’t like, too bad.

So we have the same balancing act as before, just with some redistribution of weights. The Fed is cutting rates at end July but by only 25 bp. The market had gotten ahead of itself projecting 50 bp and perhaps another cut after July, as well. This is less dollar-negative. At the same time, anxiety and risk aversion is on the upswing because it seems so unlikely anything good can come of the Trump-Xi meeting next weekend. This is outright dollar-favorable. It’s even possible Mnuchin made the optimistic comment this morning specifically to jawbone the dollar higher, not because the US wants a stronger dollar but because it wants to avoid a face-losing rout engineered inadvertently by Trump.

We hate to give credit to the repulsive Mnuchin, but he may see that the dollar is indeed at some risk of losing stature. The dollar was dumped because of the rate cut outlook and the resulting falling yields, but it seems as though the dumping went farther than yield can explain.

The dollar as money for transactions—the global numeraire—may not be affected much by Trump’s mismanagement. As a unit of account, it’s safe. But as a store of value, money’s third function, Trump us rapidly chipping away at the dollar’s reputation and credibility. This may well be a reason behind the rise of gold and cryptocurrencies. Everyone hates Zuckerman but Facebook’s Libra crypto has a real chance of upending the world financial system. The Economist magazine ran some scare comments about what central banks are going to do about it (nothing much), being managed by a committee in Switzerland as a basket of currencies (has never worked before but you never know, viz. the SDR), and Facebook’s privacy and security issues (massive). Still, the dollar is out of favor for some reason, and the falling yield is not sufficient to explain it.

It's better to have the dollar fall, Mnuchin may be thinking, because a China trade deal reduces global anxiety and risk aversion—than because the US is mismanaging its power. And to a certain extent, bolstering the dollar takes some heat off the Fed, something the Treasury has done in the past but is unexpected in today’s environment.

We had expected a Tuesday pullback because the drop last week was excessive and caused by hysteria more than realistic outlooks and facts, but what we are getting is weak. This gives pause. It’s possible the dollar is indeed getting its Trumpian comeuppance.

Tidbit: The Congressional Budget Office projects the federal deficit rising from 78% of GDP this year to 144% by 2049, an unprecedented number and an unsustainable one. And we will not be able to grow out way out of it because of demographics and because labor productivity is stuck as low levels. The new normal of pernicious slow growth for a decade predicted back during the 2008 crisis is longer-lasting than we thought.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat