US CPI Preview: Backing up the pause

- US annual core inflation stable

- Headline CPI expected to be unchanged

- Consumer prices will provide little direction for Fed policy

The Bureau of Labor Statistics will issue its February consumer price index on Tuesday March 12th at 8:30 am EDT, 12:30 GMT

Forecast: A flat horizon

Overall consumer prices are expected to be 0.2% higher in February up from flat in January. Annual prices are predicted to be unchanged at 1.6%. Core CPI, excluding food and energy costs could be 0.2% higher on the month and 2.2% on the year both unchanged from January.

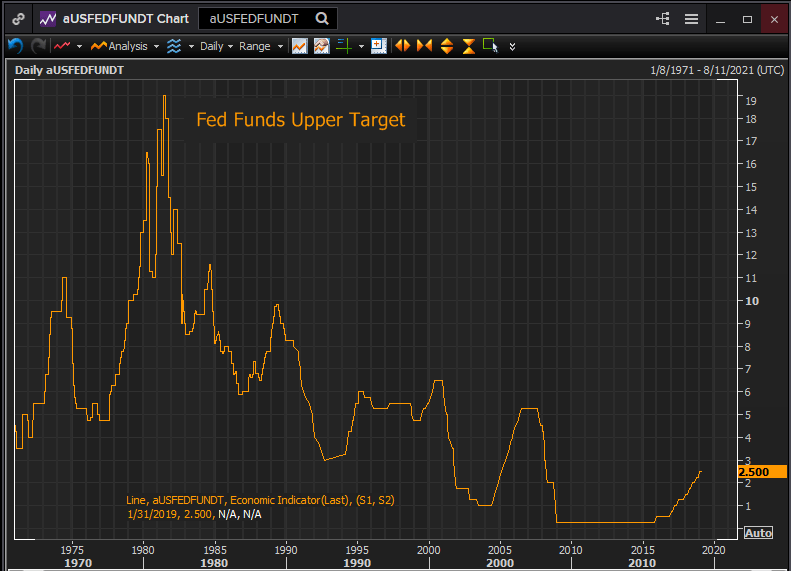

Inflation, Growth and the Federal Reserve

One of the Federal Reserve’s two Congressional policy mandates is price stability; the other is employment. The Fed has defined stability as 2% core inflation and has struggled over much of the decade since the financial crisis to instill upward pricing in the US economy.

The Fed governors have revised the policy that instituted four 0.25% rate increases last year. The new watchword is patience. The bank's December Projection Materials reduced the year end Fed Funds rate to 2.9% from 3.1% and thus the prospective 2019 rate increases from three to two. The economic growth estimate for this year was dropped to 2.3% from 2.5%. The PCE core inflation projection was dropped to 2.0% from 2.1%.

Reuters

New materials are due at the FOMC meeting on the 19th and 20th of this month. Any further reduction in the Fed Funds projection, the GDP assessment or the inflation forecast will reinforce and probably extend the market estimate for the Fed rate pause.

The Fed’s caution in December was not primarily based on the American economy which then appeared to be in good condition. That may have changed. December’s plunge in retail sales, however anomalous it may seem, and the drop in first quarter growth estimates to below 1% is will have secured Fed attention.

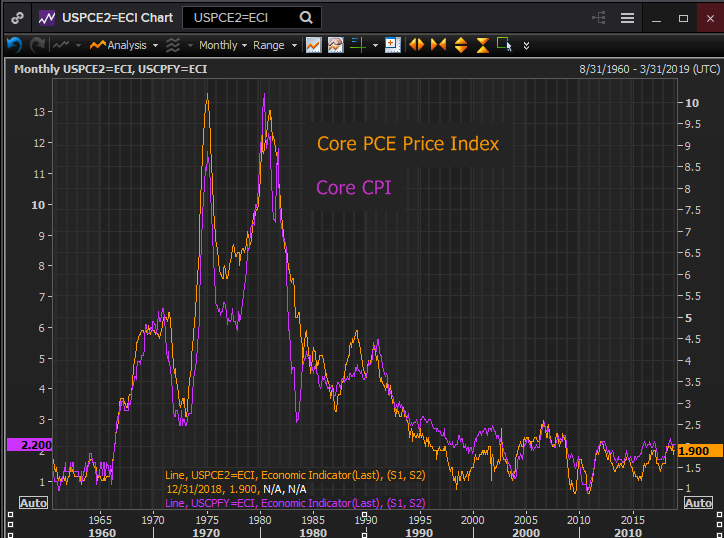

Core PCE versus Core CPI

The Fed’s preferred inflation measure is the core personal consumption expenditures price index, core PCE for short. The target is 2%. Core PCE is an updated version of the consumer price index, CPI. Its different composition results in a lower inflation rate. The PCE index has price data back to 1960. The consumer price index returns to 1958.

Reuters

CPI, PCE, the Fed pause and the dollar

Inflation was not one of the Fed’s main concerns at the December FOMC or the press conference explanations provided by Chairman Powell and it was not the source of the Fed policy change.

The market interest is in CPI is as a predictor of the core PCE rate. The correlation between the two rates is strong though the CPI level tends to be higher. If CPI weakens PCE will likely also and the Fed will have gained another justification for its new policy. If CPI is stronger than anticipated the chance of a second half rate hike will have gained a small fillip.

The annual core PCE rate was 1.9% in December down from 2.0% in September but up from 1.8% in October. Core CPI was 2.2% in January.

The dollar has been largely range bound against its major counterparties for close to five months. One of its supports in its run higher over the prior seven months was the disparity between the Fed’s rate increases and the ECB’s rate accommodation.

If falling US inflation begins to confirm that a restrictive Fed policy is history then that will eventually tell on the dollar. The CPI result will not move markets but it may point to their future direction.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.