US Consumer Sentiment Preview: Finally an update on coronavirus resurgence damage, S&P 500 on alert

- The University of Michigan's Consumer Sentiment Index for July is projected to remain stable.

- US COVID-19 cases picked up only in mid-June and recent data has been unable to capture the shift.

- Investors seemed to shrug off June's retail sales figures and are likely to react to this figure.

- The last publication of the week may set the tone for the S&P 500's close.

Back to the fast lane – hard data has become stale once again and only the freshest figures seem to be relevant. Retail sales leaped by 7.5% in June , smashing the already high expectations of a 5% increase and rising by 1.1% from June 2019 – a V-shaped recovery.

Consumption is central to the US economy, the figures exceeded estimates and the sales returned to pre-pandemic levels – yet investors shrugged it off. Why?

In mid-June, US coronavirus cases began rising, most prominently in the Sun Belt. The early reopening of the economy triggered elevated expenditure – potentially some deferred shopping – but then turned down again. The hard data failed to capture the rapid change. Jobless claims for the week ending on July 10 remained stubbornly high and better reflected the new downturn.

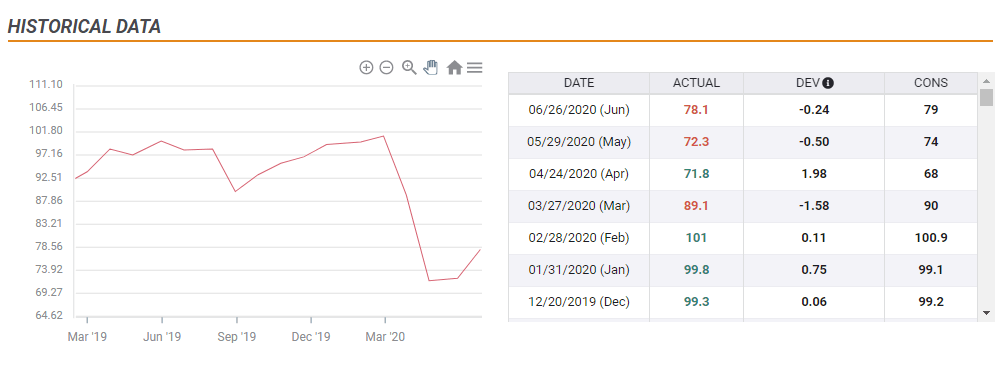

A better picture of the US pulse – albeit based on a survey and not on sales data – comes from the University of Michigan. Its preliminary Consumer Sentiment Index for July is set to show a minor increase to 79 points from the final read of 78.1 in June.

As the chart shows, consumer confidence roughly floated between 90 to 100 before the COVID-19 crisis, then plunged to a low of 71.8 in April before partially recovering to 78.1 in June.

Expectations and reactions

Economists' estimates reflect stability – no further improvement nor deterioration. That makes the potential reaction straightforward.

1) Within expectations: Anywhere between 78 – close to June's figure – and 80 would be considered within forecasts and would likely leave S&P 500 unchanged, leaving the focus on other developments such as updated COVID-19 statistics, Sino-American relations, and companies' earnings. The dollar would trade differently against each currency.

2) Above expectations; Scores above 80 and potentially closer to 90 would already show that Americans are brushing off the recent deterioration – or perhaps that it has not affected all consumers. The greater New York area continued seeing infections fall during this period. The S&P 500 could close the week on a positive note and the greenback could pare some of its gains.

3) Below expectations: Any read under 78, and especially closer to the trough of 71.8 would already show that shoppers have become shy and concerned – potentially plunging the economy. In this scenario, the S&P 500 would struggle and decline while the safe-haven dollar would shine.

Conclusion

The UoM Consumer Sentiment has the last word week with up-to-date on a crucial part of the economy – which may be about to turn down. The reading has the potential to set the tone for stocks and the dollar as the week draws to a close.

More Central banks make way for governments to act and move markets, but there is only one real boss

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.