US Conference Board Consumer Confidence Preview: Is sentiment enough?

- Confidence continues to recover from its January drop.

- Consumer attitude has sustained at levels reached only twice in 52 years.

- Q1 GDP estimates at odds with consumer sentiment.

The Conference Board will release its Consumer Confidence Index for March at 10:00 am EDT, 14:00 GMT Tuesday March 26th.

Forecast

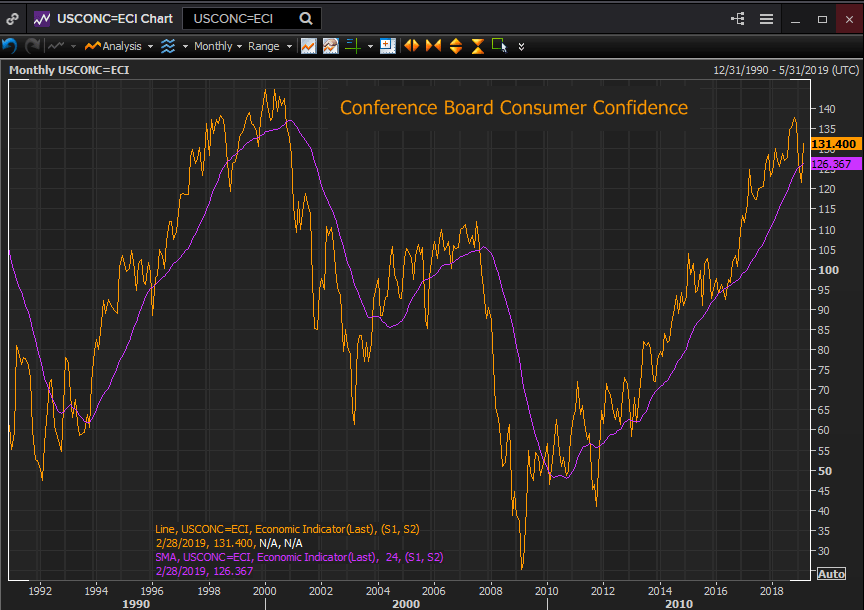

The Consumer Confidence Index from the non-profit business group the Conference Board is projected to rise to 132.0 in March from 131.4 in February. The Present Situation Index was 173.5 in February up from 170.2 in January. The Expectations Index was 103.4 in February increasing from 89.4 in February.

US Economic Growth

The US economy slowed in the final quarter of 2018. Annualized GDP was listed at 2.6% in the second revision from the Bureau of Economic Analysis. Quarterly expansion averaged 3.27% in the first nine months. The final revision will be issued on Mach 28th, with the median consensus at 2.4%. That would leave the quarterly average at 3.05%.

Growth forecasts for the 1st quarter are running far below last year. The Atlanta Fed GDPNow estimate is currently1.2% with the next update due on March 26th. The estimate will be updated as data becomes available with the final version on April 25th. The New York Fed’s current Nowcast GDP estimate is 1.29%

Consumer Confidence

Conference Board sentiment had begun to ebb last November from October’s 18 years high at 137.9. By December it had fallen to 126.6. The partial closure of the federal government pushed it to the January low. After falling to its weakest reading in 16 months at 121.7, the third straight negative result, consumer confidence rebounded smartly in February to 131.4.

Consumer confidence over the last two years has been its best in almost two decades. The 24 months moving average in February was the highest since October 2001. The four years of the final Clinton term were the longest period of consumer optimism in the 52-year record of the series.

Reuters

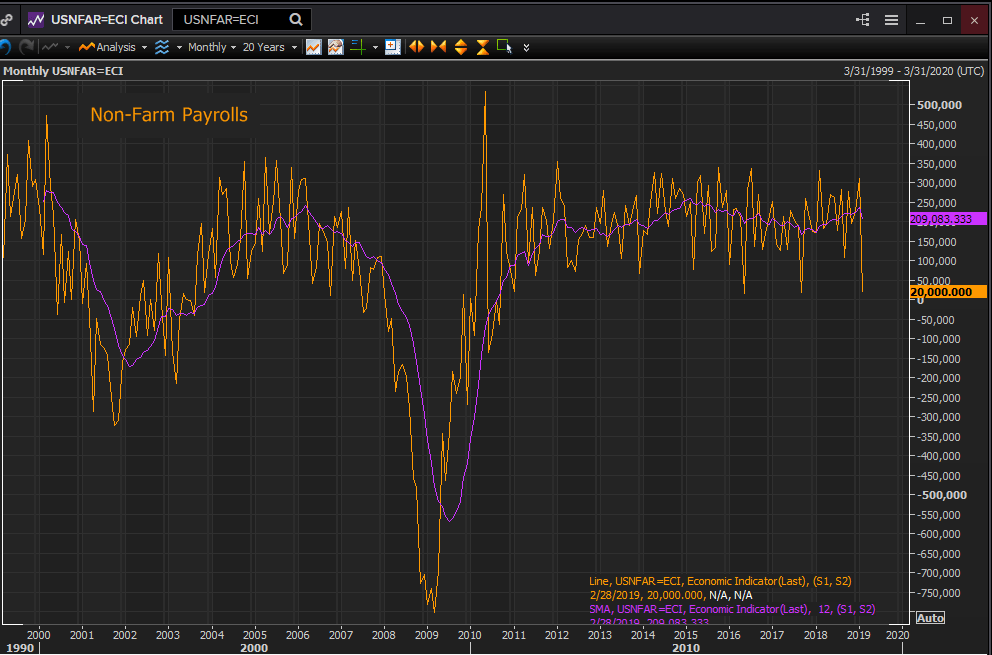

Optimism has been supported by the booming labor market particularly rising compensation. Annual wage gains rose to 3.4% in February the highest since April 2009. Jobless claims are at levels in the past associated with elusive full employment and might have had prior Fed boards tilting toward preventative rate increases.

February’s unexpected plunge to 20,000 in the non-farm payrolls, far below the forecast and the running averages is until there is more information, an anomaly.

One month disappointments in the midst of strong job creation are not unknown. In September 2017 NFP came in at 18,000 after the August 12-month moving average was 188,700. In May 2016 NFP was 15,000 the lowest since September 2010, after a 221,500 average in April. In each occasion, payrolls rebounded the next month, in October 2017 to 260,000 and in June 2016 to 282,000.

Reuters

The inexplicable drop in the December retail sales statistics, in contravention to most private accounting of holiday sales, reversed sharply in January, leaving economists still uncertain exactly what occurred with the December numbers. Retail spending has not collapsed.

Consumer Sentiment and the US Economy

The US economy is driven by domestic consumption. More than 70% of economic activity is derived from the choices of American consumers. Their direction guides the investment decisions of business. As long as the main consumer engine continues to run at a high capacity the economy runs smoothly.

Will Americans take their sentiments from the job market and surrounding economy or have global worries and politics sapped the inherent optimism of US consumers?

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.