US business activity slows in May, survey shows

USDINR 77.52 ▼ 0.08%.

EUR/USD 1.0712 ▼ 0.20%.

GBP/USD 1.2535 ▲ 0.05%

India 10-Year Bond Yield 7.338 ▼ 0.29%.

US 10-Year Bond Yield 2.770 ▲ 0.37%.

ADXY 103.69 ▼ 0.14%.

Brent Oil 111.89 ▲ 1.08%.

Gold 1,860.49 ▼ 0.26%.

NIFTY 50 16,196.35 ▲ 0.44%.

Global developments

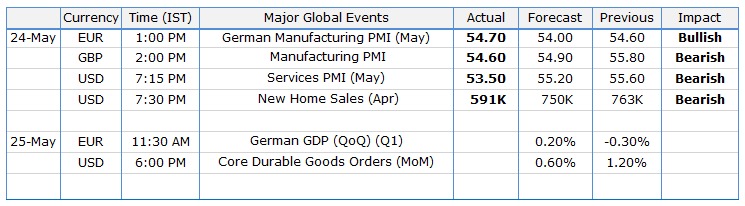

As a sign of how tightening monetary policy is impacting demand, new home sales in the US fell 16% MoM in April. Both Manufacturing and Services PMI for May too came in below expectations. Services PMI in fact fell to a four-month low.

After ECB president Lagarde comments yesterday that the ECB would look to come out of negative rate territory by September, more ECB members sounded hawkish with one member even saying the ECB should not rule out a 50bps hike.

UK services PMI came in much lower than expected at 51.8 (exp 57.6). It was the lowest print since Feb'21 and raised fears of a recession.

Focus today will be on the Fed meeting minutes due late evening India time.

Price action across assets

Disappointing US data caused US treasuries to rally. Yields are lower by about 10bps across the curve with a yield of 10y at 2.76%. The Dollar is flat overall. Euro has strengthened on hawkish comments from ECB members. The pound dropped about 100pips from highs yesterday post a huge miss on PMI. US equities ended lower with S&P500 losing 0.8% and Nasdaq 2.4%. Crude prices have inched higher with Brent close to USD 115 per barrel.

Eurozone business growth slowed in May but still resilient –PMI.

Domestic developments

After the wheat export ban and hike in export duty on certain steel products, there are reports India may look to cap sugar exports to keep domestic prices in check.

USD/INR

The Rupee underperformed amid broad Dollar weakness. We have seen off-late that during bouts of Dollar strength Rupee does not weaken as much and during phases of Dollar weakness, the Rupee does not appreciate as much. For now, Rupee's underperformance is helping correct overvaluation. CNHINR has appreciated to 11.64 from 11.40 a few sessions ago.

3m ATMF vols ended around 6.25% while 1y forward yield ended flat at 3.84%.

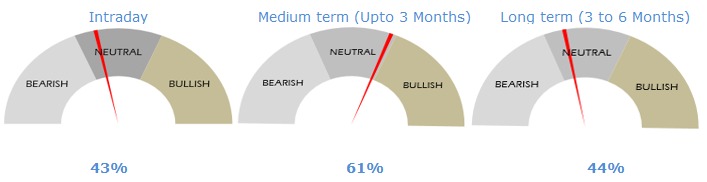

The rupee is likely to open around 77.53 and trade in a 77.45-77.70 range with sideways price action.

Bonds and rates

Rates rallied with 5y OIS ending 13bps lower at 6.87%. While the benchmark 10y yield ended 3bps lower at 7.36%, the belly of the curve saw a bigger drop of around 6bps. 10y SDL cutoffs came in around 7.70%.

Equities

Domestic equities gave up gains from earlier in the session with the Nifty ending 0.5% lower at 16125. SGX is indicating a flat open for Nifty.

Strategy

Exporters are advised to cover on upticks towards 77.90. Importers are suggested to cover on dips towards 76.50. The 3M range for USDINR is 75.50–78.30 and the 6M range is 75.00–78.90.

The U.S. to allow the Russian debt payment license to expire.

FX outlook of the day

USD/INR (Spot: 77.53)

The Indian rupee underperformed amid broad Dollar weakness. We have seen off-late that during bouts of Dollar strength Rupee does not weaken as much and during phases of Dollar weakness, the Rupee does not appreciate as much. For now, Rupee's underperformance is helping correct overvaluation. Disappointing US data caused US treasuries to rally. The Dollar is flat overall. Focus today will be on the Fed meeting minutes due late evening India time. The pair is expected to trade with a sideways bias amid broad dollar weakness and other global cues. The intraday range of the pair is expected to be between 77.45-77.70.

EUR/USD (Spot: 1.0706)

EUR/USD dribbles around a one-month high, after rising for the last two consecutive days, as the US dollar selling pauses ahead of FOMC meeting minutes. ECB President Christine Lagarde's hawkish comment to portray the economic resilience of the bloc and positive data from Germany supported the common currency. Further, some of the ECB policymakers have spread direct comments on the 50 bps rate hike in July and offered notable strength to the Euro. On the data front, German composite PMI was firmer for May at 54.6 (exp of 54) while the Eurozone numbers were softer-than-expected (54.9 against ex of 55.3). The market will be looking forward to German GDP and gfk data and Christine Lagarde's speech. The pair is expected to trade in the range of 1.0670 to 1.0760.

GBP/USD (Spot: 1.2520)

After the release of the UK's PMI data, the British pound witnessed a steep fall of 120 pips from a high of 1.2600 and later recovered marginally in the US session on the weaker dollar. On the economic data front in the UK, the Services PMI landed at 51.8 vs. 57.3 as expected while the Manufacturing PMI was recorded lower at 54.6 vs. 55.1 forecasts. Analysts have highlighted the likelihood that soaring inflation is likely to prompt even worse figures in the coming months. In absence of any macro data from the UK, investors are focusing on the release of the FOMC minutes, which will dictate the strategic development behind the announcement of the 50 basis points interest rate decision by the Federal Reserve. The pair is expected to trade in the range of 1.2470 to 1.2580.

USD/JPY (Spot: 126.96)

The USDJPY ended the day with a sharp decline, the pair broke under 127.00 and tumbled to 126.34, the lowest level in a month. It remains near the lows, under pressure amid risk aversion, a drop in US bond yields, and weak data from the US. US bond yields dipped by 12-13 bps across the 2-30y curve. The US Manufacturing PMI (57.5) remained at par while Services PMI tumbled sharply to 53.5 against an expectation of 55.2. New Home Sales in the US have also dipped sharply on the back of rising interest rates. The number for Apr came in at 591k against an expectation of 750k. The market will be looking forward to BOJ governor, Kuroda's speech later in the day. The pair is expected to trade in the range of 126.40 to 127.30.

A sharp slowdown in UK business activity rings recession alarm.

Economic calendar

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.