UK jobs market tight despite surprise rise in unemployment rate

We can tentatively say that UK worker shortages have stopped getting worse, but high levels of sickness and lower inward migration mean they are unlikely to improve dramatically in the near term. This is further ammunition for Bank of England hawks this Thursday, though we still suspect the overall committee will favour another 25bp hike over a 50bp move.

The UK’s unemployment rate surprisingly increased in the three months to April, bucking more than a year’s trend of repeated decline. But big picture, the story is essentially the same as it has been for months. While the unemployment rate is at 3.8%, which still equates to pre-Covid lows despite the latest increase, total employment is still down by roughly a third of a million people – though that deficit has narrowed this year. The number of people inactive – that is neither in employment nor actively seeking it – is up by a similar amount.

The result is that there is still more than one worker for every unfilled role, albeit the sharp rise in vacancies we saw through the second half of last year does appear to be levelling out. We can tentatively say that worker shortages are no longer actively getting worse.

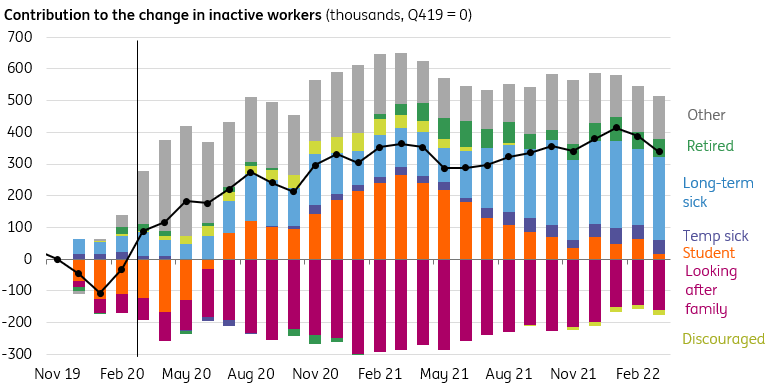

That said, long-term sickness rates are still the overwhelming reason behind lower participation rates. While the underlying drivers of this trend are not fully clear – it doesn’t appear to be entirely a Covid story, for instance – we can probably say that it’s unlikely to improve dramatically in the near term. Lower inward migration from the EU has also exacerbated the problems with sourcing labour, and again this is a trend that's unlikely to change quickly.

Long-term sickness has driven up inactivity levels through the pandemic

Source: ONS

Assuming these shortages persist, at least for certain sectors, then firms have a strong incentive to retain staff as much as possible even if economic demand slows considerably later this year, amid concerns about rehiring when conditions improve. With margins under pressure, we suspect firms are more likely to reduce individual worker hours in periods where demand slows, rather than reducing the size of the workforce.

All of this provides ammunition for the Bank of England’s hawks to continue arguing for a 50bp hike this week. The ball is undoubtedly in their court, with an increasing number of global central banks considering more aggressive rate rises.

But the Bank of England’s forecasts from May showed that, based on market interest rate expectations from the time, inflation would undershoot target in 2024 – a not-so-subtle way of saying that policymakers thought investors were pricing in too much. A 50bp hike risks adding further fuel to that fire, so we still suspect the committee as a whole will come down in favour of another 25bp hike this week. But as was the case in May, we’re likely to get a split vote with at least three officials voting for a faster move.

Read the original content: UK jobs market tight despite surprise rise in unemployment rate

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.