Trump aims to be no Mr. Scrooge

In the last full trading week of the year, global equities are kicking off on a positive note after Friday’s Republican Senate caucus agreement on the shape of U.S tax cuts aimed at boosting growth in the world’s largest economy.

The vote is expected to take place Tuesday – which will almost certainly pass – with passage onto a Senate vote later in the week and possibly allow President Trump to sign into law ahead of Christmas.

The Bank of Japan (BoJ) will meet mid-week (Dec. 20), and is expected to maintain its current policy.

Elsewhere, it is a relatively light week for economic data. November merchandise trade data will be released for Japan, while Q3 final GDP estimates will be released for the U.K, U.S, France and New Zealand.

Tomorrow, in Germany, the December Ifo survey will be posted, while Spain’s Catalonia votes on Thursday in a regional election for the second time on independence.

Note: The Czech Republic, Hungary, Taiwan and Thailand also set interest rates this week.

In China, President Xi Jinping kicks off China’s Central Economic Work Conference. The market will focus on whether officials will cut the growth target from this year’s +6.5% or actually increase it. In the U.K, PM Theresa May addresses parliament today and meets with her cabinet tomorrow to begin work on a trade wish list. The E.U will unveil its position on Wednesday.

Finally, the market is also waiting for the outcome of South Africa ruling ANC party leadership elections – the two presidential candidates are Nkosazana Dlamini-Zuma and Cyril Ramaphosa.

1. Stocks get the green light

In Japan, equities scored their biggest rally in four-weeks overnight with financials and exporters in demand. The Nikkei share average finished +1.55% higher while the broader Topix was up +1.36%.

Down-under, Aussie shares finished higher overnight, with broad-based gains driven by stronger commodity prices, financials stocks and optimism around U.S tax reform. The S&P/ASX 200 index rose +0.7% at the close, ending a two-day losing streak. On the year, the index is up +7% this year, which would actually be its best performance since 2013.

In Hong Kong, equities closed firmer, with regional sentiment boosted by expectations that U.S lawmakers will pass the tax bill. *At close of trade, the Hang Seng index was up +0.7%, while the Hang Seng China Enterprises index rose +0.43%.

In China, Shanghai stocks slipped overnight, amid concerns over tight year-end liquidity after the People’s Bank of China (PBoC) lifted interbank market rates. The Shanghai Composite index was down -0.13%, while the blue-chip CSI300 index was unchanged.

Note: The PBoC raised interest rates on reverse repos by +5 bps for the 14-day tenor.

In Europe, regional indices start the week on the front foot, trading atop of six-week highs as optimism over the U.S tax plan continuing to support markets.

U.S stocks are set to open in the black (+0.3%).

Indices: Stoxx600 +0.8% at 391.2, FTSE +0.3% at 7512, DAX +1.2% at 13258, CAC-40 +1.2% at 5413, IBEX-35 +0.7% at 10217, FTSE MIB +0.8% at 22274, SMI +0.3% at 9425, S&P 500 Futures +0.3%

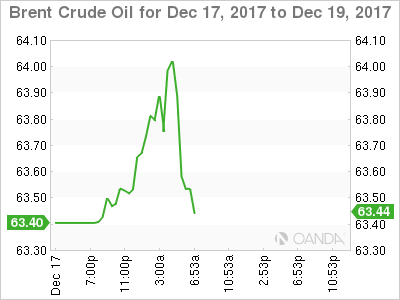

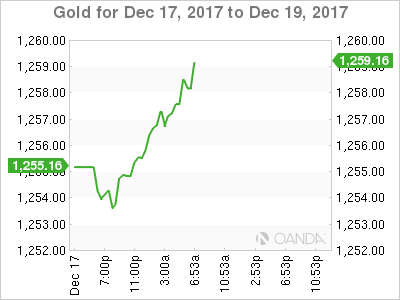

2. Oil prices rise on ongoing North Sea outage, Nigeria strike, and gold higher

Oil prices remain better bid amid an ongoing North Sea pipeline outage and because a strike by Nigerian oil workers threatened its crude exports. Also, signs that booming U.S crude output growth may be slowing is also supporting the market.

Brent crude futures are at +$63.72 a barrel, up +49c or +0.8%, from Friday’s close. U.S West Texas Intermediate (WTI) crude futures are at +$57.70 a barrel, up +40c or +0.7%.

North Sea operator Ineos has declared “force majeure” on all oil and gas shipments through its Forties pipeline system, while in Nigeria, the Petroleum and Natural Gas Senior Staff Association have started industrial action after talks with government agencies ended in deadlock.

While in the U.S, data on Friday (Baker Hughes) indicated that energy companies have cut rigs drilling for new production for the first time in six weeks – 747 rigs in production in the week ended Dec. 15.

Gold prices remain range-bound as the ‘big’ dollar holds firm on U.S tax bill hopes. The ‘yellow’ metal has increased +0.1% to +$1,257.21 an ounce, the highest in more than a week.

3. Sovereign yields mixed results

Expectations that the Bank of Japan (BoJ) may tighten policy and steepen the yield curve sooner rather than later are lifting long-dated Japanese interest rates.

In recent weeks, some BoJ officials have dropped hints that it could tweak its policy, but this week is expected to come too soon. Many investors think officials could eventually lift its 10-year bond yield target, currently around zero, by +25 bps in H1, 2018. Japan’s 10-year JGB yield has dipped less than -1 bps to +0.042%, the lowest in two-weeks.

Elsewhere, the yield on 10-year U.S Treasuries has climbed +2 bps to +2.37%, while Germany’s 10-year Bund yield has gained less than +1 bps to +0.31%. In the U.K, the 10-year Gilt yield has fallen -1 bps to +1.146%, the lowest in almost 14 weeks.

Note: Portuguese bond yields have fallen sharply this morning after a two notch ratings upgrade from Fitch on Friday – the country now holds an investment grade from two of the three major rating agencies and could soon return to major bond indices.

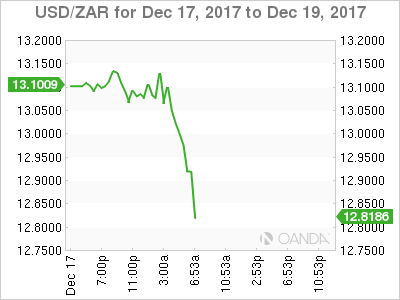

4. South Africa wait for ANC election results

The ZAR ($12.9504) remains better bid as South Africa’s ruling ANC party votes for a successor to President Jacob Zuma today. The recent rally would suggest that the market is betting on a win for the pro-reform candidate Dlamini-Zumail Ramaphoosa. A win for Mr. Zuma’s ex-wife Nkosazana Dlamini-Zuma would be negative for the rand.

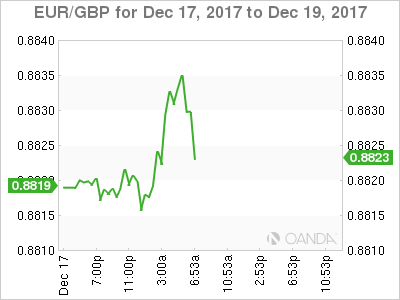

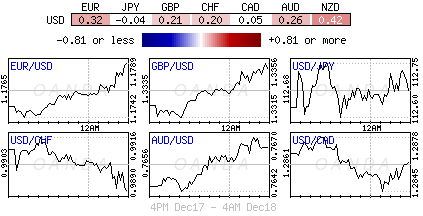

The USD trades mixed against the majors as the U.S tax reform bill moves closer to ratification. EUR is higher by +0.3% at €1.1791, but holding below the psychological €1.18 level. USD/JPY is little changed at ¥112.60 area.

Note: Republicans are confident Congress will now pass the tax bill this week, with a Senate vote as early as Tuesday and President Trump aiming to sign the bill by week’s end.

5. Annual inflation up to +1.5% in the Euro area

Data this morning from Eurostat shows that Euro area annual inflation was +1.5% in November 2017, up from +1.4% m/m. In November 2016, the rate was +0.6%.

The E.U annual inflation was +1.8% in November 2017, up from +1.7% m/m. A year earlier the rate was +0.6%.

Digging deeper, the lowest annual rates were registered in Cyprus (+0.2%), Ireland (+0.5%) and Finland (+0.9%), while the highest annual rates were recorded in Estonia (+4.5%), Lithuania (+4.2%) and the U.K (+3.1%).

Note: Compared with the previous month, annual inflation fell in four Member States, remained stable in nine and rose in fifteen.

Author

Dean Popplewell

MarketPulse