Bond market still not on board with a March rate hike

Outlook:

It's hard not to worry about Trump as president because he is erratic. But except for the occasional jumpiness—tax reform coming soon! buy equities! buy dollars!—the market grinds on in the background on very much the same factors as in pre-Trump days.

This time we have two Fed presidents saying a March hike is a good idea. Yields rise. Dollar follows.

We might complain that the yield recovery is not proportional to the news. Yields should be higher. The bond gang is still not on board with a March rate hike.

But it's not the same-old, same-old because Trump is a factor, not only for US securities but also be-cause of a new kind of contagion—to France and maybe Italy. Just as Trump said "let's get out of bad deals that don't serve our self-interest," politicians in Europe are saying the same thing—the eurozone doesn't serve our self-interest, let's get out. Brexit is somewhat different. Brexit was a vote against economic self-interest in favor of a different kind of self-interest—sovereignty.

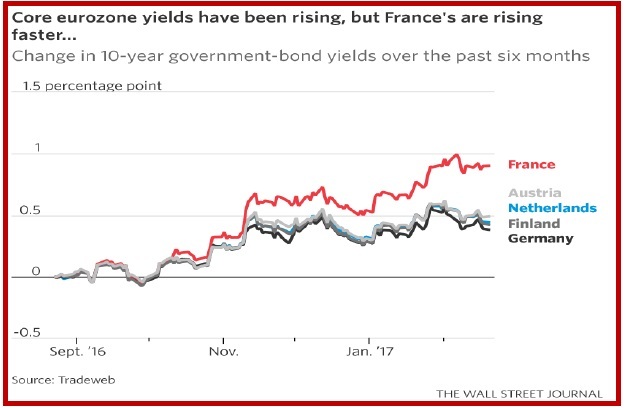

A majority thought Brexit was silly and would never happen. But it did. A majority thought Trump was ridiculous and he could never get elected. But he did. Observers are licking their wounds and wondering if they should not be giving greater credibility to the idea of a LePen (or Grillo) victory at the polls and thus an actual exit from the EU and/or eurozone. Grexit looks like small potatoes compared to a French exit.

Fear is a perfectly sensible development. The WSJ reports that after the 2010-12 crisis, "French bonds traded with Germany's. On Monday, a poll showing Ms. Le Pen comfortably in the lead for April's first round of the presidential election drove yields on French 10-year bonds to jump to 1.064%... The spread with German bond yields hit 0.84 percentage points during the day on Monday, the highest in more than four years, before settling at 0.75 percentage points as European markets closed. Six months ago, this gap was only 0.22."

Bloomberg reports a slightly different number but never mind. "The yield differential between France and Germany has now hit 81 bp, the highest since the debt crisis of 2011/12. "The latest poll numbers show that the National Front leader Marine Le Pen is set to win the first round of French Presidency with a much higher margin than previously estimated. She is set to get 27 percent of the votes, whereas her closest rivals, both Emmanuel Macron and Francois Fillon are expected to receive 20 percent of the votes. All the polls released so far, predict that Madame Le Pen is set to lose big in the second round." But by now we all know about the unreliability of polls.

Right now the betting market has Macron ahead of LePen, if with lower odds than a week ago. Lad-brokes has 15/8 for both top runners in the final, final (after two rounds of preliminaries), although a lot depends on the preliminaries. See the Ladbrokes table.

Bloomberg notes that last time there was an existential eurozone crisis, "the problems faced back then by Europe were essentially about monetary architecture. Governments lacked a fiscal union and a central-bank backstop, exposing them to the whims of bond vigilantes. Mario Draghi solved the problem in 2012 with his "whatever it takes" speech. This time, the stresses building in Europe are perceived as more political. Anti-euro factions are on the rise while mainstream center-right and center-left parties are seeing their support melt away. As risk transfers from the monetary realm to a political one, these problems won't go away with three simple words from a central banker."

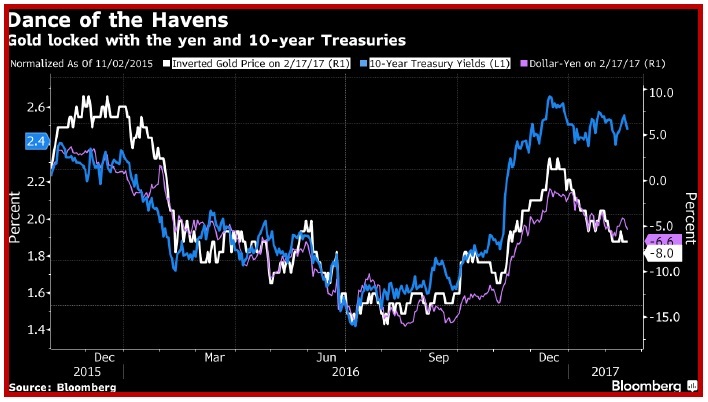

Political uncertainty should push gold up. Rate hikes in the US should push gold down, if only because any return is better than none. But that's not what we are seeing, suggesting that political fears are overwhelming the rate of return/inflation factors. Bloomberg remarks that the last three rate hikes saw gold rise in the following months, not fall. "Gold is up about 7 percent since the Federal Reserve raised rates on Dec. 14. It jumped 13 percent in the two months following the last increase in December 2015 and 6 percent the previous time way back in June 2006."

What's getting in the way now of gold falling back on the Fed's plan is Trump. We got that response initially, but it faded in favor of uncertainty outweighing fiscal stimulus. "Investors in the largest ex-change-traded fund backed by gold have bought more than 40 metric tons this month, helping to boost prices 6.8 percent this year to $1,236.86 an ounce. There were seasonal gains in the run up to Lunar New Year in January when the Chinese typically purchase gold as gifts." One analyst, who rejoices is the name Dahdah, says there might be a big manager on a buying spree. We already know Druckenmil-ler has been a big buyer "because of the lack of clarity on U.S. government policy."

But the yen and the 10-year are havens along with gold. Now to get the bond gang on board. The chart here is from Bloomberg.

The FT uses an interesting phrase—the "normalization" of Trump. After several rounds of near-hysterical criticism of Trump, not only for the Muslim ban but also bad trade policy ideas and more lies, the only we got in the last 48 hours is the Sweden terrorist attack that never happened.

The absence of extraordinary statements for two days hardly qualifies as normalization, but after the first month, perhaps it's fitting that everyone calm down. Just as the Trump reflation rally was built on thin air, the doom-and-gloom was also built on smoke. Sometimes smoke is just smoke and doesn't mean there is a fire. After all, we know Trump likes to disrupt. He will disrupt again, too, but like the boy who cries "wolf" too often, at some point the financial markets will just ignore Trump.

So, while a trade and currency war with China is not exactly off the table, fear of China and other re-serve holders dumping Treasuries is just a scenario, not a certainty and not a reasonable justification to dump dollars in advance. And the Trumpies may cheat on trade and budget data, trying to disguise a giant jump in the US deficit to come, but realistically, economists have been warning for decades about the too-big deficit. Except when Congress decides not to fund the government and outright default looms, the US deficit is not a key factor in the level of the dollar. The Tea Party, in essence, failed.

Remember what Citibank chief economist Buiter said a few days ago—the robust, flexible US economy and a hawkish Fed combine to give serious support to the dollar, especially with the rest of the world still in the grip of "extraordinary" monetary policy. The US is normalizing. Europe and Japan are not. Simple.

Note to Readers: Thank you for voting for me "Best Analysis" at FXStreet.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 113.69 | SHORT USD | 01/05/17 | WEAK | 115.93 | -0.74% |

| GBP/USD | 1.2422 | LONG GBP | 01/24/17 | WEAK | 1.2451 | -0.23% |

| EUR/USD | 1.0536 | LONG EURO | 01/10/17 | WEAK | 1.0587 | 1.01% |

| EUR/JPY | 119.78 | SHORT EURO | 02/03/17 | WEAK | 121.56 | 1.46% |

| EUR/GBP | 0.8481 | LONG EURO | 02/06/17 | WEAK | 0.8605 | 0.11% |

| USD/CHF | 1.0097 | SHORT USD | 01/05/17 | WEAK | 1.0113 | 0.73% |

| USD/CAD | 1.3155 | SHORT USD | 01/05/17 | WEAK | 1.3253 | 0.74% |

| NZD/USD | 0.7137 | LONG NZD | 01/10/17 | STRONG | 0.7014 | 0.67% |

| AUD/USD | 0.7658 | LONG AUD | 01/05/17 | WEAK | 0.7343 | 4.29% |

| AUD/JPY | 87.06 | LONG AUD | 10/06/16 | WEAK | 78.48 | 1.33% |

| USD/MXN | 20.4182 | SHORT USD | 01/31/17 | WEAK | 20.8108 | 1.89% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat