The euro move on the French election news is a runaway gap

Outlook:

The euro move on the French election news is a runaway gap, differentiating it from a common gap. Common gaps get filled. Breakaway gaps do not because they are a trend continuation move. Breakaway gaps are based on hard news that promotes the existing trend and they al-ways result in a profit-taking pullback, an excellent opportunity to buy on the dip (and possibly the origin of that idea). Things are a little more complicated this time because the French election is in two-parts. We can easily see the market pull back repeatedly over the next two weeks as new polls come out. Ironically, the CFTC Commitments of Traders report on Friday had specs' net euro shorts at the highest since March.

Everyone notes that the two winners in the First round of the French election are non-Establishment, meaning not belonging to the existing mainstream political parties. This is not strictly true. LePen's party has been around so long it needs to be considered "established" if not Establishment. Macron's policy stance is thoroughly conventional and not all that different from Fillon's. Fillon has now said he will back Macron, implying his bloc of votes will go along and deliver a re-sounding Macron victory. We don't know where the far-left Melenchon voters go next. Weirdly, they could go to far-right LePen in an overall anti-Establishment move.

Political analysts are breathing a sigh of relief that Brexit and Trump were not the death of polls, after all. Some suggest that a multi-party system is better than the two-party system on the grounds that voters become accustomed to having a populist party in the mix. We doubt it. Multi-party systems have resulted in unstable coalitions and in some instance, months and months with no leadership at all.

In the US, Trump is supposed to roll out a tax plan and possibly a new health care plan as well this week, with critics saying there has not been sufficient time and staffing to deliver true plans and we are likely to get nothing more than rhetorical bluster and self-congratulation. Here's the problem: the government runs out of spending authority on Friday, which will be Trumps' 99th day in office. We probably won't get a government shut-down but only a short-term extension in the form of a "continuing resolution" that does no more than kick the can down the road. Trump insists the budget contain funding for a border wall (that he said Mexico will pay for) while the border tax is not among the tax reform proposals, a broken promise in spades.

The Treasury is already gearing up for a loss of wiggle room. It must pay some obligations before others. Remember that stupid billion-dollar coin that supposedly the president can issue and borrow against? This was a loophole dreamed up during the Obama years. Obama was too dignified and conventional ever to do such a thing, but Trump is neither. And on Saturday, the press holds its annual White House Correspondents Dinner. The host and various speakers take turns ridiculing the president and any other easy target at these events. Obama himself ridiculed Trump at one of them. It's a glorious opportunity to make fun of Trump but Trump has already said he is chickening out and will not attend.

Talk by Congress and the White House will likely override hard data this week, which is mostly about the housing market. We are worried about the Atlanta Fed GDPNow forecast due on Thursday for Q1 GDP. Last week it was a lousy 0.5%. The New York Fed, meanwhile, gets 2.7% for Q1. Granted, discrepancies be-tween forecasts is common, but this one is a doozy. If the Atlanta Fed is correct, the US economy is far weaker than we thought. If the NY Fed is right, the US economy is far stronger than we thought and providing a strong push to the Fed for the June rate hike.

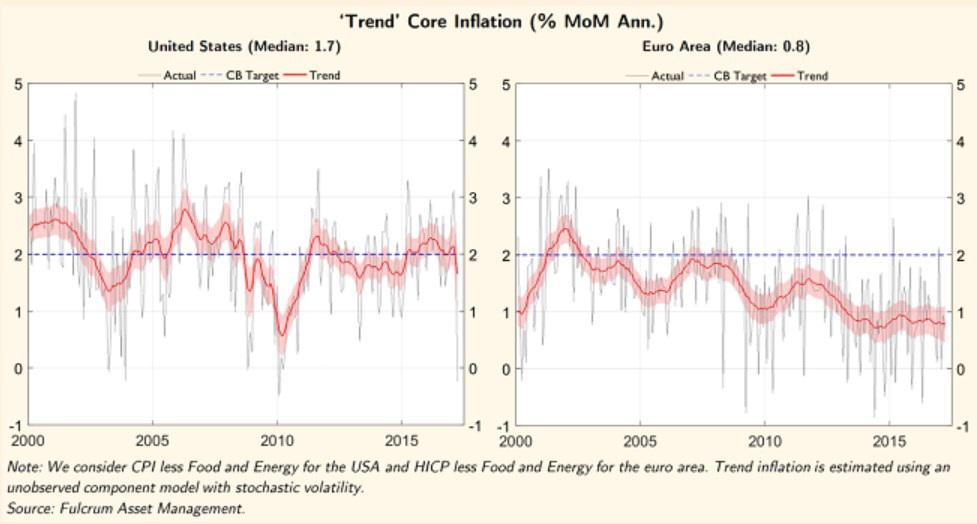

So which is it? The IMF is optimistic about a global recovery that will deliver 3.5% this year. Maybe the US will deliver 1-1.5% in Q1 but a big acceleration in Q2. The real problem is that inflation is fading back (in both the US and Europe), implying that the Trump reflation trade, while not a dead duck, will be much delayed. See the chart from the FT.

Meanwhile, N. Korea said yesterday it is prepared to strike aircraft carrier Carl Vinson, finally turned around and headed for the Sea of Japan. The NYT reports Chinese Pres Xi telephoned Trump this morning to urge him not to respond in kind to a nuclear test by N. Korea, which may still be pending despite N. Korea not acting on April 15 as expected.

For some reason, the major news outlets failed to pick up a CBS report on a series of N. Korean statements on Saturday that it will respond with nuclear war if it is attacked. It's not clear that the carrier nearing the Korean cost constitutes an "attack."

N. Korea said, among other things, Trump administration officials are "spouting a load of rubbish" and "seeking to bring nuclear aircraft carrier strike groups one after another to the waters off the Korean Peninsula." CBS reports "The recent escalation in tension will be front in center in Washington on Monday. Diplomat-ic sources tell CBS News that U.S. Ambassador Nikki Haley will escort Security Council members to Washington for a series of meetings with members of Congress before heading to the White House for a photo-op and lunch with President Trump. The high-profile visit will give U.N. diplomats an unusually high level of access to the president."

Oh, dear. We can say, again, that we don't know how big a financial market effect these matters have. But confidence in the US economy and current steward-ship has to be low and falling—although we have yet to see foreign fund managers run away from US auctions.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 110.21 | SHORT USD | 03/21/17 | WEAK | 112.51 | 2.04% |

| GBP/USD | 1.2807 | LONG GBP | 04/12/17 | STRONG | 1.2495 | 2.50% |

| EUR/USD | 1.0866 | LONG EURO | 04/13/17 | STRONG | 1.0643 | 2.10% |

| EUR/JPY | 119.75 | SHORT EURO | 03/28/17 | WEAK | 120.19 | 0.37% |

| EUR/GBP | 0.8485 | SHORT EURO | 04/12/17 | WEAK | 0.8487 | 0.02% |

| USD/CHF | 0.9947 | SHORT USD | 04/13/17 | STRONG | 1.0043 | 0.96% |

| USD/CAD | 1.3415 | LONG USD | 04/24/17 | NEW*STRONG | 1.3415 | 0.00% |

| NZD/USD | 0.7033 | SHORT NZD | 04/12/17 | WEAK | 0.7022 | -0.16% |

| AUD/USD | 0.7581 | SHORT AUD | 03/28/17 | WEAK | 0.7607 | 0.34% |

| AUD/JPY | 83.54 | SHORT AUD | 03/22/17 | STRONG | 85.20 | 1.95% |

| USD/MXN | 18.5072 | SHORT USD | 01/31/17 | STRONG | 20.8108 | 11.07% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat