The Fed is finally talking about AI – Here's why it matters for the US Dollar

For much of 2024 and into early 2025, Artificial Intelligence was framed as an equity market theme, something for Nasdaq bulls and venture capital decks. That is now changing fast. AI is moving from earnings calls into the heart of monetary policy discussions, forcing Federal Reserve officials to confront a new question: How to act if AI reshapes inflation, employment and interest rates at the same time?

By late 2025, it started to pop up in Federal Reserve speeches, almost tentatively. Now, in early 2026, it has moved firmly into the policy debate.

The transition has been subtle, but it is hard to ignore. What began as cautious curiosity has turned into a far more serious discussion about how AI might alter productivity trends, reshape labour markets, shift inflation dynamics and even nudge the neutral rate of interest.

This is no longer a story about tech enthusiasm but about how the Fed reacts. And this is crucial for the US Dollar and the entire Forex board.

From “too early to tell” to potential tension in the dual mandate

The Federal Reserve’s view of Artificial Intelligence has evolved rapidly from cautious observation to recognition of it as a potential macroeconomic force with real policy implications.

In late 2025, Fed officials largely treated AI as an emerging topic requiring study rather than action, emphasising the lack of concrete evidence that it was materially affecting employment or productivity. The tone was cautious, almost academic, with policymakers focused on understanding possible long-term effects rather than incorporating AI into economic decision-making.

By late 2025 and into early 2026, however, the narrative shifted as AI began appearing in labour market dynamics and investment behaviour.

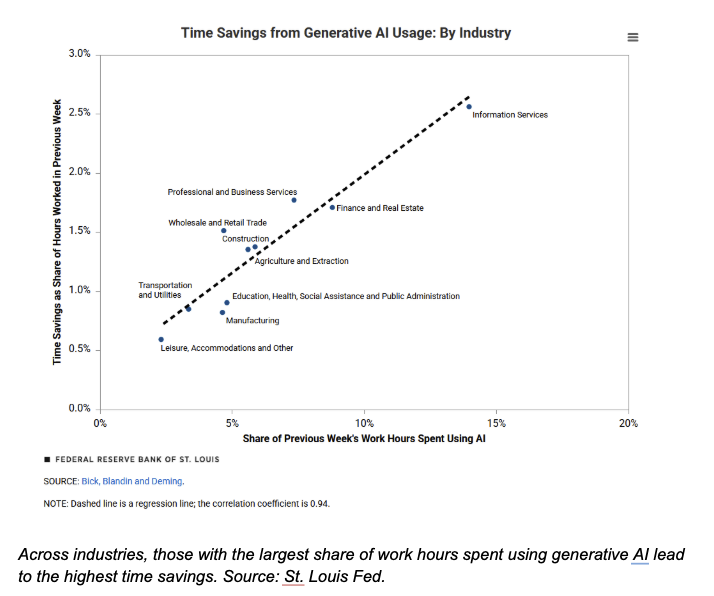

Governor Lisa Cook described AI as potentially the most significant reorganisation of work in generations. She warned that job displacement could come before new roles are created and suggested the neutral rate could rise in the short run due to investment demand. Crucially, she noted the Fed may not be able to offset an AI-driven rise in unemployment without risking inflation.

That is a dual mandate dilemma, and the common thread around it is uncertainty.

Productivity promise, policy headache

The debate inside the Fed is no longer about whether AI will matter. It is about timing and transmission.

If Artificial Intelligence delivers a genuine lift to productivity, potential output could expand and inflation pressures might ease over time. On paper, that is a gift for policymakers.

But the path may not be so clean. If companies hold back on hiring to finance AI investment, or if job displacement runs ahead of new roles being created, unemployment could edge higher even while headline growth looks resilient. In that kind of mix, inflation may not slow quickly enough to open the door to aggressive rate cuts.

Then there is the neutral rate dilemma.

If AI unleashes a new wave of capital expenditure and nudges up trend growth, the equilibrium rate of interest could rise, at least for a while. That would complicate the comforting narrative that the post-pandemic neutral rate is quietly drifting lower.

In short, AI could simultaneously:

- Support growth via productivity and investment.

- Unsettle the labour market.

- Alter inflation dynamics.

- Affect the neutral rate.

That is not an easy environment for the Fed.

Why markets should care

Markets currently price AI primarily through equities and long-term productivity optimism.

The Fed is beginning to price it through labour, uncertainty and structural change.

If productivity genuinely accelerates, the long end of the Treasury curve may not fall as easily as many expect. Stronger trend growth tends to anchor yields higher, even if the policy rate eventually comes down.

If, instead, hiring softens without a broader slowdown in activity, the labour market's data could become trickier to read. Unemployment might drift up for reasons that are more structural than cyclical, blurring the signal policymakers usually rely on.

For the US Dollar (USD), the implications are straightforward. If AI adoption spreads more quickly across the US economy than elsewhere, relative productivity gains could translate into relative growth outperformance, and that tends to be US Dollar supportive.

At the same time, the Fed itself is moving carefully. Officials have signalled they are cautious about deploying AI internally, a reminder that they are still trying to understand the shock before fully incorporating it into their toolkit.

Productivity, policy and the US Dollar

For currency markets, this is not a side story. It could become a core driver.

If AI-led productivity gains take hold more decisively in the US than in other major economies, relative growth differentials would likely widen. In FX, that matters. Stronger trend growth in the US would tend to favour the Greenback, especially against currencies where productivity improvements are slower to arrive or where policy settings remain tightly constrained.

There is also the rates channel. If AI investment keeps capital expenditure elevated and gradually pushes the neutral rate higher, US yields, particularly at the long end, may stay firmer than consensus assumes. A structurally higher equilibrium rate would make it harder to sustain a broad USD bearish narrative.

Conversely, if labour displacement emerges more quickly than productivity gains, and unemployment rises without a corresponding inflation slowdown, the Fed could face a more delicate balancing act. In that environment, rate volatility would likely increase, and with it, US Dollar volatility.

In short, AI is not just an equity story. It has the potential to reshape yield differentials, rate expectations and, ultimately, the US Dollar’s medium-term trajectory.

Bottom line

The AI has moved from the sidelines to the centre of the Fed’s macro conversation.

Officials are no longer asking whether AI matters. They are asking how it will interact with productivity, the labour market, the neutral rate, and whether monetary policy will be able to respond cleanly if displacement and inflation pressures collide.

The AI boom may yet prove productivity-enhancing and disinflationary. But for policymakers, the transition phase could be the real challenge.

And that means AI is no longer just a technology story but a monetary policy variable.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.