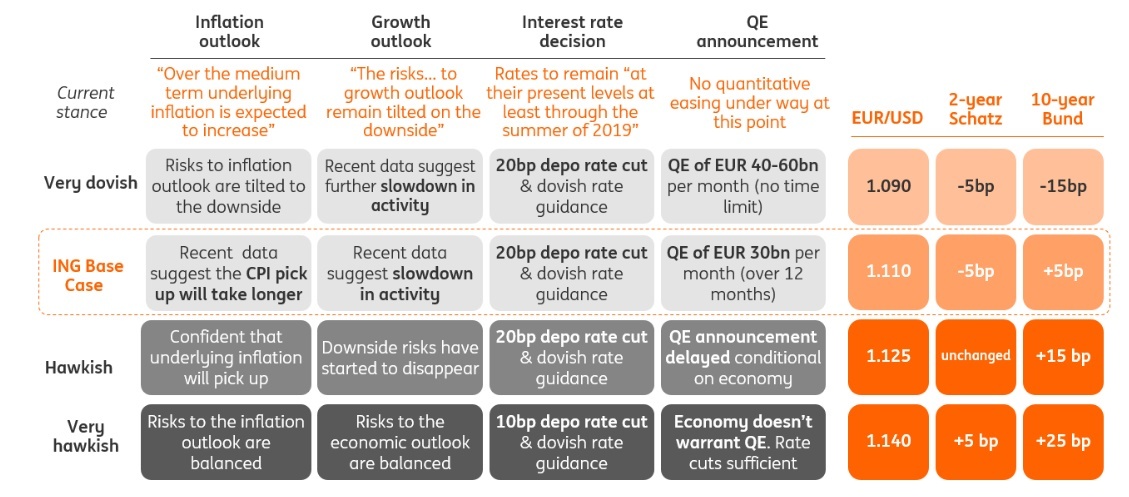

The ECB Dashboard: a question of delivering

Given the chance that the ECB fails to match market expectations for easing policy, the balance of risks favours higher EUR/USD and European FX outperformance on the day. But any spike in EUR/USD and EU FX should be temporary, as growth concerns will eventually kick in. A disappointing level of QE could also point to higher European rates and bond yields

Rate cut set in stone, but what about QE?

Following the recent comments of various ECB Governing Council members about the lack of urgency in re-starting QE and strong market expectations for this, the risk to EUR/USD after the meeting are tilted to the upside. Another deposit rate cut (likely 20 basis points) and generous pricing of Targeted Longer-Term Refinancing Operations (cheap loans) seem to be set in stone, but it will be the QE (non-)announcement and size of the programme that will determine the EUR/USD price action. As per our ECB Preview, we look for a 20bp depo rate cut, a small tiering system, a repricing of TLTROs and the restarting of QE (EUR 30 billion per month).

The balance of risks suggests higher EUR/USD…

Unless the ECB goes big (EUR 40-60 billion per month) we expect either limited euro reaction or a spike in EUR/USD higher – the former being a response to the EUR 30bn QE size, the latter a responce to a delay of the bond buying programme (as per the ECB Dashboard above). In the case of the ECB delaying the QE announcement, we look for EUR/USD to converge to the 1.1250 level as this would materially disappoint markets. While the balance of probabilities favours higher EUR/USD (particularly after the USD gains over the past two months), we expect EUR/USD strength to be temporary.

… but not for long

This is because disappointing ECB monetary stimulus will likely increase market concerns about the eurozone's economic outlook and lead to a further deterioration in growth and inflation expectations. This could lead to an even bigger need for subsequent ECB easing. Hence, a potential EUR/USD rebound this week from lower-than-expected ECB easing should be seen as an attractive entry point to prepare for lower EUR/USD levels later this year. We discuss our bearish view on EUR/USD in detail in EUR/USD: Lower for longer as dollar is king and expect the cross to move into a 1.05-1.10 range for the rest of the year.

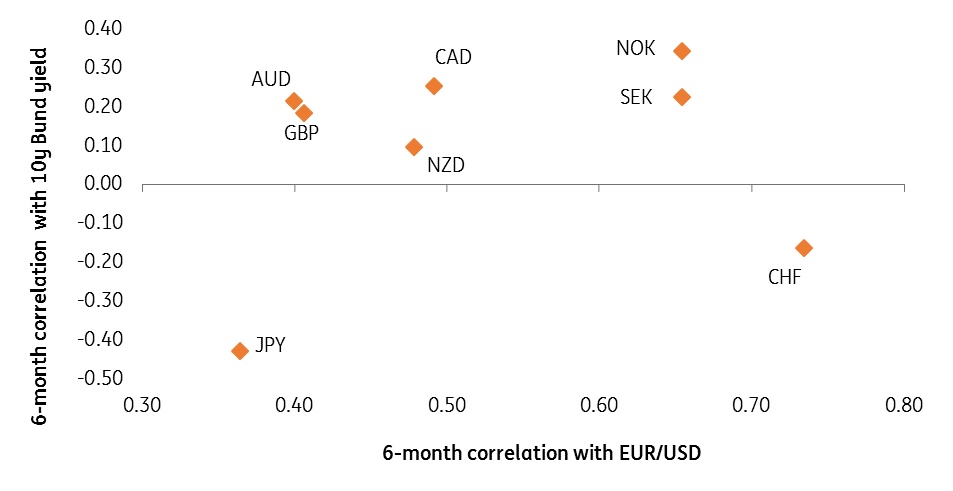

Figure 1: NOK and SEK set to benefit from possible ECB disappointment

European FX to outperform on the day, but this won’t last

Possible dissapointment over the ECB's package also suggests that other European currencies will outperform on the day (vs the US dollar and the USD-block currencies) as they tend to show high correlation with EUR/USD (bar the idiosyncratic driven British pound). The Norwegian krone (NOK) and Swedish krona (SEK) should do well. This is depicted in Figure 1, which shows that SEK and NOK are the main beneficiaries in the G10 FX space from the mix of higher EUR/USD and higher bund yields.

Although the Swiss franc (CHF) exerts high correlation with EUR/USD, the reasons behind the possible rise in EUR/USD (i.e. the lack of QE) should, in fact, be negative for CHF and lead to higher EUR/CHF (particularly when CHF shows a negative correlation with bund yields which would increase in such a scenario). The potential lack of a dovish surprise from the ECB should also benefit SEK and NOK via the reduced market expectations of more dovish polices from their domestic central banks. However, given the European economic slowdown, the upside to NOK and SEK should not be long lasting, as is likely to be the case for EUR/USD itself.

Rates view: We are sceptical that tiering can be a game change

Disentangling market reaction to the various parts of a policy package is notoriously difficult, and might indeed be one of the points of unveiling them as a package in the first place. We would warn for example of the detrimental effect a 20bp deposit rate cut would have on banks and so, on risk sentiment. Even this is hard to ascertain before the announcement because the magnitude of this reaction depends on the credibility of mitigating measures. We, for one, are sceptical that tiering can be a game changer.

More than ever, details matter as much as the headline measures. Nevertheless, the key variable to look out for in Thursday’s policy announcement is whether asset purchases are restarted. We think market expectations are still skewed towards a fairly aggressive QE programme so any signs that the General Council's preference is shifting towards rate cuts/ guidance, or towards supressing credit spreads rather than outright rates, would all be negative for long-end swap rates and EGB yields. For front-end rates, a 20bp deposit rate cut or more generous TLTRO III pricing would be a positive that could be mitigated by tiering measures.

Read the original analysis: The ECB Dashboard: A question of delivering

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.