The drop in US yields is a problem

Outlook: US data is, on the whole, better than forecast and does not warrant an expectation of the Fed retreating from its strong hint that tapering is about to begin because of inflation now appearing longer-lasting and higher than thought. GDP for Q3 can easily meet the gloomiest forecast (0.5% by the Atlanta Fed) without changing the Big Picture. Note that Bloomberg now has 2.6%.

Durables were better than expected and if we choose to deduce, as most analysts do, the non-defense capital goods ex-aircraft number was a nice 0.8% (from 0.5%) and the 7th month of gains. This is the proxy for business investment and while we’d prefer a Japanese-style “Capex intention,” we’ll take this one. Core shipments are up a very hefty 10.6% annual rate. This affirms the nice PMI last week and bodes well for GDP.

Something that takes away from GDP is merchandise exports, down 4.7% in Sept from Aug, while imports remained okay, up 0.5% overall but 3.6% for capital goods. What happened to port congestion depriving us of Christmas toys? The trade deficit widened to $96.3 billion from $87.6 billion in August, a new record high and far more than Bloomberg had forecast ($88.3 billion). This is just goods and doesn’t include services, an increasingly important component of the trade balance–we get that next week (Nov 4).

We have gone from “transitory” inflation to “persistent” inflation in a very short period of time. We can’t recall a time when central banks were so quickly responsive to data. Historically they drag their heels, get accused of being behind the curve, and only reluctantly admit they need to change their minds but not for several months. The only other time a central bank was so responsive was the ECB rate hike back as the 2008-09 crisis was in full swing, which everyone said was a mistake (and so it was).

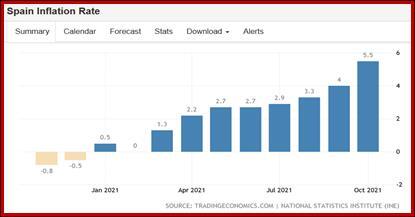

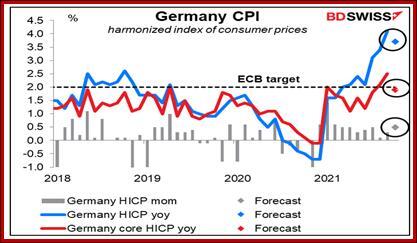

But this time the ECB is universally expected to keep everything the same, in the face of a trend toward ending QE and higher rates all over the place, starting with Norway and New Zealand and spreading to Brazil and Canada, plus the UK and US. And this will be the in the face of inflation rising and substantially. So far today we have Spain (5.5% from 4.0% instead of the 4.6% expected) and later today it will be Germany. See the chart of German inflation borrowed from Gittler at BDSwiss. We get the eurozone version tomorrow.

This puts the ECB on the back foot, as the British put it, with QE persisting to March and no change in policy attitude expected until December. This is the summary of the various commentaries, which can give you a headache with all its qualifications and potential modifications far out on the margin. Traders tend to be more brutal–are you part of the crowd or not? The ECB is not, and will be punished for non-conformity, probably in the form of a falling currency.

Meanwhile, G20 meets in Rome and the UN climate summit COP26 is held this weekend in beautiful Glasgow, with nobody prepared to keep any promises given the energy shortage. Pres Biden had imagined he could assert global leadership but is embarrassed by having no climate plan approved by Congress, only two ambassadors out of the 20 in G20 because the Senate Republicans are withholding approval, and gridlock within his own party overpaying for infrastructure spending.

The blow to the US reputation is not as bad as when the previous president was making blunders all over the place, but a whiff of anti-US sentiment remains in the air. Does this affect the markets? How can it not? Still, expectations are for a better growth outcome in Q4 and Q1, even if the supply chain problems are not fully resolved. The drop in US yields is a problem and we could get a pullback in the dollar near-term before things are seen to be getting better.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat