Tensions in Middle-East, strong US inflation, interest rate cuts delay expected, UK

Previous week’s events (week 15 - 19.04.2024)

Announcements

On April 13, Iran launched a large salvo of missiles and drones at Israel. Designated “Operation True Promise,” the attack reportedly included around 170 drones, 120 surface-to-surface ballistic missiles, and 30 cruise missiles.

A few days after, Israel launched an attack on Iran, US officials said on the 19th of April. US officials said overnight that an Israeli missile struck Iran in the city of Isfahan in central Iran while Iranian media also reported explosions. Israel has not officially commented on the attack, while Iran downplayed the reports. “Israel will defend itself”, " Netanyahu says, as the West calls for restraint.

In both cases, commodity markets, including Gold and Crude oil, were shaken experiencing highly volatile conditions.

US economy

U.S. retail sales increased more than expected in March, further evidence that the economy ended the first quarter on solid ground.

Despite higher inflation and borrowing costs, spending is continuing to hold up, thanks to the resilient labour market.

Strong retail sales prompted economists at Goldman Sachs to boost their gross domestic product (GDP) growth estimate for the first quarter to a 3.1% annualised rate from a 2.5% pace. The economy grew at a 3.4% rate in the fourth quarter.

WorldView: The stronger economic activity remains, the later the Fed is to respond with cuts. Financial markets and most economists have pushed back their expectations for the first rate cut to September from June, and anticipate two rate cuts instead of the three envisaged by policymakers.

UK economy

The labour market in the U.K. still experiences wage growth. Regular wages excluding bonuses – which BoE is watching as it considers when to start cutting interest rates – grew by 6.0% compared with the same period a year earlier, only slightly weaker than a 6.1% rise in the November-to-January period. Core wages rose by the least since mid-2022 in the three months to February but remained strong by historical standards.

The unemployment rate rose by more than expected to 4.2% from 3.9%, also suggesting a loss of momentum in the jobs market.

Yael Selfin, chief economist at KPMG UK, said the rise in the unemployment rate and the latest slowing of pay pressure suggested the labour market was generating less inflation.

U.K.’s retail sales growth was reported at 0% in March despite high inflation easing recently, representing the first time that they have not grown in monthly terms since December.

Australia economy

Australian employment fell in March after an enormous gain the month before, while the jobless rate resumed its uptrend. Net employment dropped 6,600 in March from February when it rose to a revised 117,600. The jobless rate climbed slightly to 3.8% from 3.7% the previous month, although that was under a forecast of 3.9%

Inflation

Canada

Canada’s annual inflation rate ticked up as expected to 2.9% in March. The acceleration in headline inflation was driven by costlier gas at the pump as supply concerns and voluntary production cuts pushed global crude prices higher.

Excluding gasoline prices, inflation slowed to 2.8% from 2.9% in February. Month-over-month, the consumer price index rose 0.6%, the largest increase since July 2023, but less than a forecast 0.7% gain. Inflation has stayed under 3% since January and is in line with the Bank of Canada’s forecast for it to remain near that level in the first half of 2024.

Bank of Canada (BoC) Governor Tiff Macklem: “As expected headline inflation came in close to 3%. … Importantly, though, measures of core inflation did tick down again and that does suggest that underlying inflationary pressures are continuing to ease,” he said.

United Kingdom

Inflation was reported lower for the U.K. but higher than the forecast. The slowdown in the fall in Britain’s inflation rate follows an acceleration of headline price growth in the United States which rose for a second month in a row to 3.5% in March.

Bank of England (BoE) Governor Andrew Bailey, who said British inflation was “moving in the right direction” for a rate cut last month, also said last week that different inflation dynamics in the U.S. and Europe could lead to other paths for interest rates.

“The chances of interest rates being cut for the first time in June are now a bit slimmer,” she said.

Services inflation, an indicator of domestic price pressures which the BoE also watches closely, eased only slightly to 6.0% from 6.1%.

International oil prices climbed last month amid growing tensions in the Middle East.

The BoE is concerned that the rapid wage growth, which makes up much of the inflation rate in the services sector, could sustain inflationary heat across the economy.

“Inflation is in retreat but the Bank of England cannot yet be sure that it is beaten,” said Ian Stewart, chief economist at Deloitte

Currency markets impact – Past releases (week 15 - 19.04.2024)

Server Time / Timezone EEST (UTC+02:00)

Currency markets impact

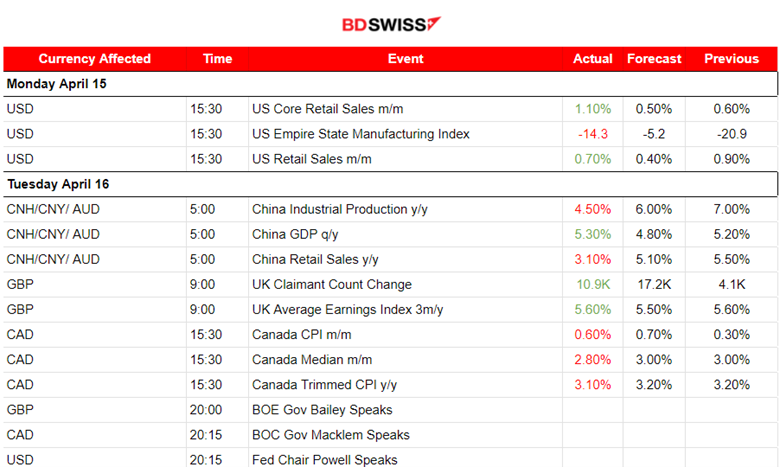

- On the 15th of April, Retail Sales figures for the U.S. showed that sales jumped 0.7% in March, much higher than expected. American consumers continued with orders despite rising inflation. Core retail sales change jumped to 1.10% from 0.60%. The USD gained after the release. EURUSD dropped to near 20 pips at that time before experiencing retracement to the intraday mean.

- According to the GDP (q/y) figure released on the 16th of April, China’s economic growth beat expectations in the first quarter, as factory output led the expansion bolstering expectations the government can hit its ambitious annual target. Gross domestic product increased 5.3% in the January-to-March period from a year earlier. Retail Sales annual change dropped to 3.10%.

- At 9:00 the employment data ( Claimant Count change) and labour market report for the U.K. were released. Unemployment rate increased to 4.2% from the previous 3.9%. The Change in the number of people claiming unemployment-related benefits during the previous month (Claimant Count) was reported higher, near 11K. Payrolled employees in the UK fell by 18,000 (0.1%) between January and February 2024 but rose by 352,000 (1.2%) between February 2023 and February 2024. The GBP appreciated at first but the effect reversed soon. The GBPUSD overall fell to nearly 27 pips after the release.

- At 15:30 the inflation report for Canada showed that the Consumer Price Index (CPI) rose 2.9% on a year-over-year basis in March, up from a 2.8% gain in February. Gasoline prices contributed the most to the year-over-year headline acceleration. The USDCAD jumped 60 pips, as the CAD depreciated greatly at the time of the release.

- According to the report on the 17th of April, the March inflation for New Zealand was reported to be higher than what RBNZ expected. New Zealand’s annual inflation rate dropped to 4% in March, from 4.7% in December. The Consumers Price Index (CPI) increased just 0.6% in the March quarter, up from 0.5% in the previous period. An intraday shock occurred at the time of the release. The NZD depreciated at first. The NZDUSD dropped to near 30 pips before immediately reversing and continuing with a steady movement to the upside.

- At 9:00 the Consumer Prices Index in the U.K. was reported to have risen by 3.2% in the 12 months to March 2024, down from 3.4% in February. At the time of the release, the GBP appreciated heavily causing the GBPUSD to jump near 60 pips.

- According to the employment data for Australia on the 18th of April, employment dropped more than expected and the unemployment rate jumped to 3.8% from 3.7%. The market reacted with AUD depreciation but the impact was moderate. The AUDUSD dropped just 10 pips.

- At 15:30 the U.S. Unemployment Claims figure was released and it was not far off from the standard figures the market has been experiencing lately as mentioned in our previous analysis. Claims were reported lower coinciding with the recent strong labour market data. An improvement in the Philly Manufacturing Index had a positive impact on the USD. In general, the USD saw a strengthening yesterday overall.

- On the 19th of April, the monthly retail sales report of the U.K. showed that Retail sales volumes (quantity bought) were estimated to be flat (0.0%) in March 2024, following an increase of 0.1% in February 2024 (revised from 0.0%). The market reacted with GBP appreciation during that time and the effect has not faded yet.

Forex markets monitor

Dollar Index (US_DX)

The index moved to the upside on the 15th of April after the retail sales figure releases since they had a positive impact on the U.S. dollar. Since then though, with the absence of further major news related to the dollar, volatility levels started to drop and a triangle formation took place as depicted on the chart. The higher-than-expected U.S. inflation figure release had already caused the dollar index to reach high levels last week and a less volatile period followed after that event, for this index.

EUR/USD

This pair is experiencing a triangle formation, mirroring the USD path, since volatility levels dropped and the U.S. dollar is not affected much by the news after the 18th of April. U.S. dollar depreciation from the 17th of April to the 18th of April, caused the pair to move to the upside heavily until it reached the resistance at 1.06880. After that, a reversal took place, the triangle started to form and a period of less volatile conditions started. It is obvious that the dollar is the main driver, however, as June gets closer the central banks, especially the ECB could make statements about interest rate cuts that could push the EURUSD to drop further. Eyes though should be on the technicals as well and to consider the triangle breakout in future price/pair direction speculation.

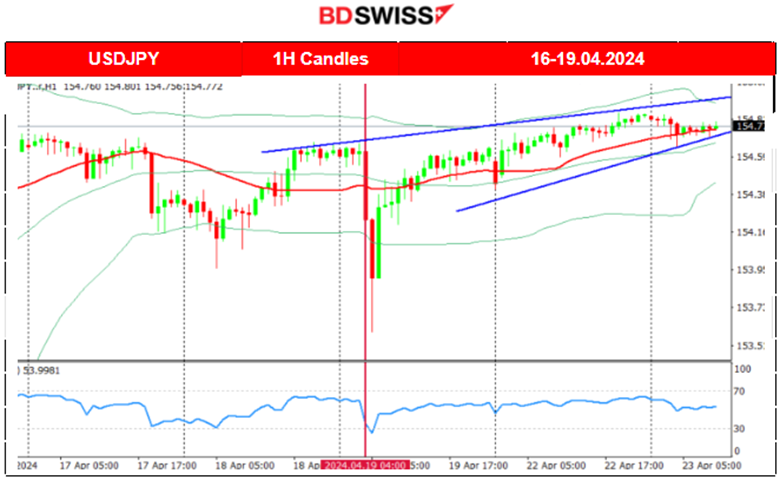

USD/JPY

JPY weakening and USD strengthening with a stable path sideways last week kept the USDJPY in the uptrend. On the 19th of April, Israel’s attack caused the markets to shake starting around 4:00. The USDJPY dropped 100 pips before reversing to the upside. Eventually, the pair remained above the 30-period MA showing that the path is likely to remain an uptrend.

Crypto markets monitor

BTC/USD

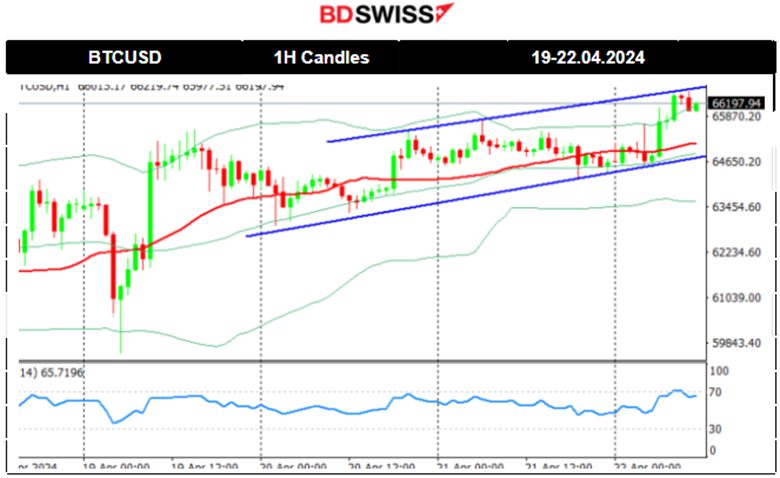

Bitcoin halving took effect late on Friday 19th April, cutting the issuance of new bitcoin in half. It happens roughly every four years, and in addition to helping to stave off inflation, it historically precedes a major run-up in the price of Bitcoin.

Its price started slowly to move to the upside and experienced an uptrend during the weekend with 66K USD being the critical resistance level for now.

This week’s events (week 22 - 26.04.2024)

Coming up

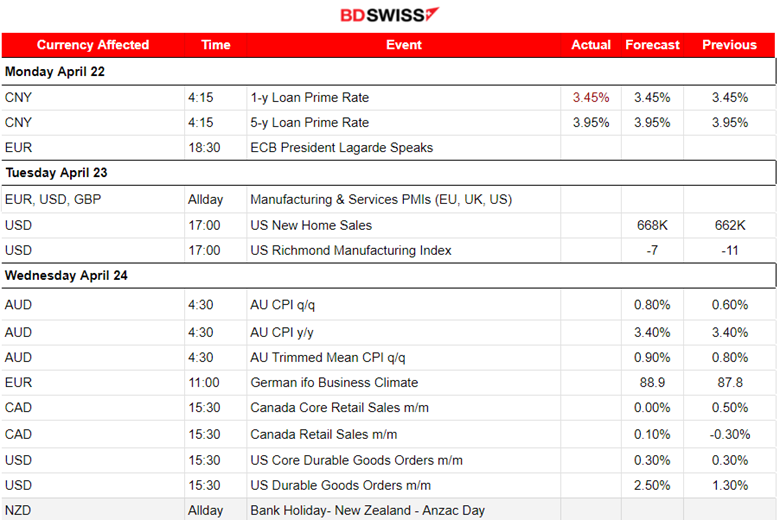

The Bank of Japan will decide on interest rates.

Manufacturing PMI releases will shake the markets a bit during the European session on the 23rd of April.

Inflation report for Australia

Canada’s retail sales report and U.S. Durable goods orders report.

Currency markets impact

- On the 23rd of April, the Manufacturing and Services PMI figures for the Eurozone, the U.K. and the U.S. will be released causing some impact on the market early affecting the EUR, GBP and USD. Since we have no interest rate policy change, the economic business conditions are expected to remain roughly the same in all these regions.

- On the 24th of April, inflation figures for Australia will be released. It is expected that the annual inflation will remain steady. It has remained steady since the last release in January this year, however during that time the AUD pairs are usually affected greatly.

- Canada retail sales figure release might have a great impact on the CAD pairs. The expected core and normal figure have different directions. The core monthly change is expected to drop to 0% instead of rising like the normal figure. On a monthly basis Canada’s inflation is rising, according to the past 3 readings.

- The U.S. Durable goods figure releases at 15:30 could have a big impact on the market with USD pairs to be affected by a moderate intraday shock. These are expected to be reported higher since the U.S. economy looks to get stronger this year.

- On the 25th of April, the Advanced GDP figure (q/q) for the U.S. will be released shedding some light on how the U.S. economy is growing. It could be the case that the market will experience a moderate intraday shock at the time of the release affecting the USD pairs.

- On the 26th of April, the annual Tokyo Inflation figure will be released and it is expected to drop. Japan's core inflation actually slowed in March.

- The BoJ is expected to keep short-term interest rates unchanged at its next policy meeting this week. However, the JPY pairs and even the USD pairs could be affected greatly at the time of the release. The interest rate differential is still high between these two. The question is, will the JPY continue weakening? Another important question, will the USD continue strengthening? The likelihood that the Fed will change the Federal target rate at the upcoming FOMC meeting on the 1st of May is 1.9% according to the CME’s FedWatch tool.

Commodities markets monitor

US Crude Oil

Since the 16th of April, the market has shown that volatility lowers and this was the cause of a triangle formation to appear. A breakout occurred on the 17th of April eventually causing the drop of the price to 82 USD/b. On the 18th of April, the price broke the support end and reached the next support at 81 USD/b before retracement took place. On the 19th of April the news regarding the Israel attack in Iran, caused the commodity prices (Gold and Oil) to jump but only to reverse soon after fully. Currently, lower volatility levels form a triangle formation, and a breakout to the upside (which is possible considering the apparent bullish divergence) could lead the price to reach the 83.5 USD resistance. The 50-period Bollinger Band's upper band supports the possible next target resistance to be at that level.

Gold (XAU/USD)

On the 17th of April Gold moved lower as it broke the apparent upward wedge formation reaching the intraday support at 2,355 USD/oz before returning to the 30-period MA. On the 18th of April, Gold stayed in range, flirting with the 2,390 USD/oz at some point but remaining close to the MA. On the 19th of April the news regarding the Israel attack in Iran, caused the commodity prices (Gold and Oil) to jump but only to reverse soon after fully. Gold retreated eventually lower reaching the support at 2,350 USD/oz and it is estimated to continue sideways.

Equity markets monitor

S&P 500 (SPX500)

Price movement

After a period of consolidation, on the 17th of April, it broke the support at 5,040 USD and moved lower to the next support at 5,000 USD before retracing. On the 18th of April, the market remained below the 30-period MA but a breakout did not occur. The breakout of the 5,000 USD level eventually caused a sharp drop on the 19th of April as mentioned in our previous analysis. Volatility levels dropped until the end of the day and week with an apparent triangle formation in place. It seems that on the SPX500 the critical resistance is at 5000 USD. The index was on a downtrend recently as borrowing costs are expected to remain high, plus geopolitical tensions having an impact on expectations and a change to a risk-off mood. A breakout to the upside could lead to a jump of 130 USD while a breakout of the triangle to the downside can lead to the reach of the depicted support levels below.

Author

BDSwiss Research Team

BDSwiss

BDSwiss is a leading financial institution, offering bespoke CFD trading and investment products to more than 1.7 million registered clients, in over 180 countries.