![]() KBC Market Research Desk

KBC Market Research Desk

KBC Bank

Next Report will be published on Monday 9th of May 2016

On Tuesday, the repositioning out of the dollar initially continued. USD/JPY dropped to the mid 105 area. EUR/USD jumped north of 1.16. The move was technical in nature as investors reacted to the break of key technical levels.

There was little economic news. Finally, the dollar sell-off exhausted and the dollar fully retraced the earlier losses. Fed’s Lockhart keeping the door open for a June rate hike maybe helped the intraday reversal. EUR/USD closed the session at 1.1496 (from 1.1534). USD/JPY rebounded to close the day at 106.50 (from 106.41).

Overnight, risk sentiment in Asia remains negative, with regional indices recording slight to modest losses. Japanese markets are still closed for the Golden week holidays. However, USD/JPY rebounds further in line with the overall performance of the dollar. Oil traded off the recent highs with Brent back at $45 p/b. However, the link between oil and the dollar was not tight of late. EUR/USD lost a few more ticks overnight and trades at .1485. After yesterday’s technical move, the US and EMU data might decide on the next USD move.

Ahead of Ascension Day, the eco calendar heats up. The euro zone services PMI picked up marginally in April to 53.2. We see risks for a slightly stronger outcome after a better than expected manufacturing PMI. EMU retail sales are no mover for euro trading. In the US, hiring is expected to remain on track with the ADP employment report expected to show a 195 000 increase in April. We see risks for an upward surprise following a month of very strong claims data. The US non-manufacturing ISM is expected to increase for a second straight month, rising from 54.5 to 54.8. Also here we see upside risks. Finally, the trade balance is expected to show a significant narrowing in the deficit from $47.1 billion to $41.3 billion, mainly due to a sharp drop in imports.

In a daily perspective, we look out whether the decline of the dollar has run its course. The jury is still out, but yesterday’s intraday reversal of the dollar, looks a bit like a ST exhaustion move . The dollar might enter calmer waters if the ADP report and the non-manufacturing ISM meet market expectations or print better than expected, which is our expectation. Of course a new disappointment might restart the USD sell-off. We assume a consolidation or even slight further USD gains, with the payrolls to decide on the next big move.

Technically, EUR/USD finally broke above the 1.1495 MT range top mirroring broad-based USD weakness. This break was an important technical warning for further dollar losses and opened the way for a retest of the key 1.1712 (2015 high). We maintain the view that the US economy is strong enough to allow the Fed to implement the two pre-announced rate hikes later this year. This is not discounted in the interest rate markets and the currency market. However, for now there is no trigger for the market to really change course. Friday’s payrolls are the next milestone. The soft Fed approach, pockets of risk aversion and the Treasury report on currencies pushed USD/JPY to a new correction low at 106.14 on Friday and this level was again broken this morning. The inaction of the BOJ keeps the downside in USD/JPY fragile. Verbal interventions from Japan to stop the rise of the yen are likely, but we doubt they will change the trend.

USD/JPY remains some kind of a falling knife.

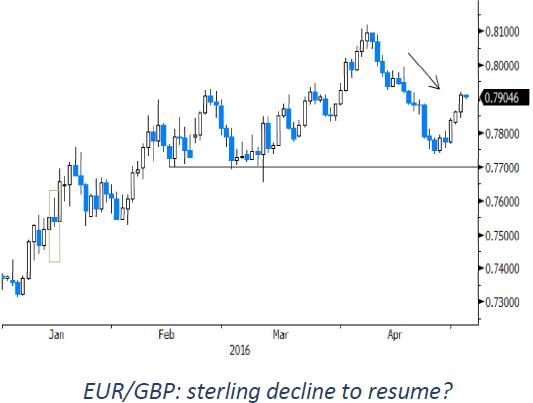

Sterling hammered after poor manufacturing PMI

On Tuesday, sterling was initially driven by the sharp swings in the dollar. In this move cable was also squeezed sharply higher. The pair set a multi-month top around 1.4770. EUR/GBP initially traded relatively stable in the mid 0.78 area.

However, the UK manufacturing PMI unexpectedly dropped in contraction territory (49.2) while a marginal improvement to 51.2 was expected. The report triggered a protracted intraday sterling downtrend, both against the dollar and the euro . EUR/GBP filled offers above 0.79 and closed the session at 0.7909 (from 0.7861). The decline of cable was even more impressive as the dollar rebounded later on. The pair closed the session at 1.4535 (from 1.4673).

Today, UK April construction PMI is expected to decline slightly from 54.2 to 54.0. This report is not so important from a market point of view. However, recently, there were already signs of a loss of momentum in the sector.

Additional negative news could trigger further sterling losses. Of course, the focus will be on the services PMI expected tomorrow. That said, we see risk for sterling to remain weak or even decline further short-term.

The technical picture of EUR/GBP improved as the pair broke above the mid 0.79 area. A counter move occurred over the previous weeks and threatened to deteriorate the picture. However the sterling rebound has apparently run its course. Sterling sentiment will remain fragile as long as the referendum outcome isn’t clear. More sterling gains might be difficult from current levels.

This non-exhaustive information is based on short-term forecasts for expected developments on the financial markets. KBC Bank cannot guarantee that these forecasts will materialize and cannot be held liable in any way for direct or consequential loss arising from any use of this document or its content. The document is not intended as personalized investment advice and does not constitute a recommendation to buy, sell or hold investments described herein. Although information has been obtained from and is based upon sources KBC believes to be reliable, KBC does not guarantee the accuracy of this information, which may be incomplete or condensed. All opinions and estimates constitute a KBC judgment as of the data of the report and are subject to change without notice.

Recommended Content

Editors’ Picks

AUD/USD gains ground on hawkish RBA, Nonfarm Payrolls awaited

The Australian Dollar continues its winning streak for the third successive session on Friday. The hawkish sentiment surrounding the Reserve Bank of Australia bolsters the strength of the Aussie Dollar, consequently, underpinning the AUD/USD pair.

USD/JPY: Japanese Yen advances to nearly three-week high against USD ahead of US NFP

The Japanese Yen continues to draw support from speculated government intervention. The post-FOMC USD selling turns out to be another factor weighing on the USD/JPY pair. Investors now look forward to the crucial US NFP report for a fresh directional impetus.

Gold lacks firm near-term direction, remains stuck in a range ahead of US NFP

Gold price struggles to gain any meaningful traction amid mixed fundamental cues. The Fed’s less hawkish outlook drags the USD to a multi-week low and lends support. Bets for a delayed Fed rate cut and a positive risk tone cap gains ahead of the US NFP.

Solana price pumps 7% as SOL-based POPCAT hits new ATH

Solana price is the biggest gainer among the crypto top 10, with nearly 10% in gains. The surge is ascribed to the growing popularity of projects launched atop the SOL blockchain, which have overtime posted remarkable success.

NFP: The ultimate litmus test for doves vs. hawks

US Nonfarm Payrolls will undoubtedly be the focal point of upcoming data releases. The estimated figure stands at 241k, notably lower than the robust 303k reported in the previous release and below all other readings recorded this year.