Reality not as silky as ideal

As early as the end of 2018, there was sign that the Fed was shifting to dovish monetary policy. Fed Chairman Powell said, in a speech at the end of November 2018, that interest rates were "just below" the neutral range, as opposed to a former statement that "it is a long way before the neutral interest rates." The subtle changes in his rhetoric, however, elevated concern in the market. Institutional investment banks almost immediately recognized that the Fed's tightening monetary policy was coming to an end. At that time, the prevailing view among institutional analysts was that the Fed would raise rates two more times in 2019 following the one in December 2018, and that this would mark the end of the interest-rate rise cycle.

The truth, however, is that reality can never be as silky as ideal.

Since January 2019, almost all of the Fed's policymakers have given speeches or published papers that were more cautious and dovish than their original positions. Among them there are former New York Federal Reserve Bank President Williams, who previously was a monetary hawk, advocating that "slowdown is the new normal, and QE and negative interest rates will be considered if necessary"; Cleveland Federal Reserve Bank President Mester, whose argument was that "if inflation doesn't pick up, the Fed could stop raising interest rates this year," and Boston Federal Reserve Bank President Rosengren, who said, "Whether more rate hikes are needed depends on the economy."

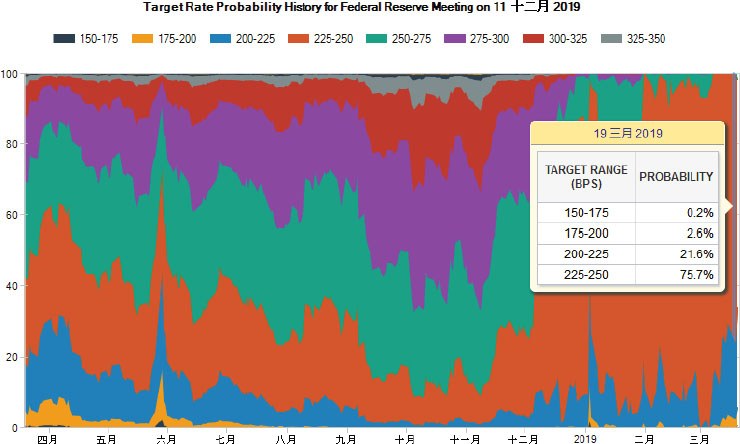

Market expectations of the number of the Fed's rate hikes for this year and next have cooled sharply. A look at the probability charts reflected by the CME FedWatch tool shows that the market had all but downplayed the likelihood of a Fed rate hike in 2019 on the eve of the Fed's March meeting. The boldest analysts even pointed out that the Fed's next move would not be a rate hike but would instead be a cut.

Expectation of an interest rate cut may sound like aggressive speculation, but the suspension of interest rate increases has become a consensus among the Fed and the market. At the Fed's March meeting, policymakers firmly put the brakes on tightening. Most fed officials expected the number of rate hikes to fall from two to zero in 2019 and at most once in 2020. They lowered GDP and inflation expectations for this year and next, and raised unemployment expectations. Thus, a plan was made to halve the scale of Treasury bond reduction from May 2019 to the end of September, and plans were made to continue reducing its holdings of agency bonds and mortgage-backed securities (MBS) so as to align with its longterm goal of primarily owning U.S. bonds.

The threshold for dovish modification of the Fed funds rate is undoubtedly higher than that of the conventional monetary policy instrument, and the signal of a shift in monetary policy is stronger.

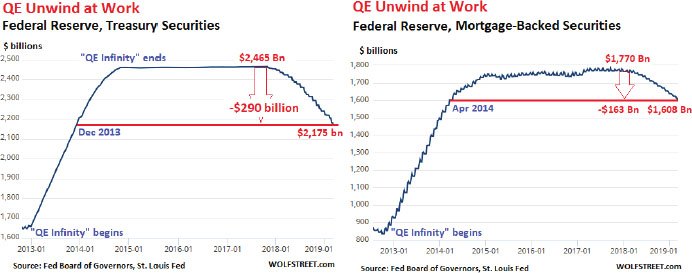

By the time QE stopped at the end of 2014, the Fed's balance sheet had reached a frightening $4.5 trillion. According to the Fed's balance sheet released on March 7, 2019, Fed had cut $290 billion in Treasury bonds, $163 billion in MBS and $48 billion in other assets since October 2017, when its downsizing was rolled out. Such asset reductions are unprecedented in its history.

The Fed's position is clearly one in which it will end its 24-month balance-sheet "squeeze plans" at the end of the third quarter. Certainly, this represents an early time node in all the mainstream market expectations. The result, in other words, is that the Fed's balance sheet will be "fuller" than previously expected.

The information contained in this website is of general nature only and does not take into account your objectives, financial situation or needs. Please ensure that you read the Financial Services Guide (FSG), Product Disclosure Statement (PDS), and Terms and Conditions which can be obtained on our website https://www.aetoscg.com.au, and fully understand the risks involved before deciding to acquire any of the financial products listed on this website.

AETOS Capital Group Pty Ltd is registered in Australia (ACN 125 113 117; AFSL No. 313016) since 2007 and is a wholly owned subsidiary of AETOS Capital Group Holdings Ltd, carrying on a financial services business in Australia, limited to providing the financial services covered by the Australian financial services licence.

Trading margin FX and CFDs carries a high level of risk and may not be suitable for all investors. You are strongly recommended to seek independent financial advice before making any investment decisions.

This commentary is owned by AETOS, and copying, reproduction, redistribution and/publishing of this material for any purpose in whole or in part without the prior written consent of AETOS is prohibited.

Recommended Content

Editors’ Picks

EUR/USD trades with negative bias, holds above 1.0700 as traders await US PCE Price Index

EUR/USD edges lower during the Asian session on Friday and moves away from a two-week high, around the 1.0740 area touched the previous day. Spot prices trade around the 1.0725-1.0720 region and remain at the mercy of the US Dollar price dynamics ahead of the crucial US data.

USD/JPY jumps above 156.00 on BoJ's steady policy

USD/JPY has come under intense buying pressure, surging past 156.00 after the Bank of Japan kept the key rate unchanged but tweaked its policy statement. The BoJ maintained its fiscal year 2024 and 2025 core inflation forecasts, disappointing the Japanese Yen buyers.

Gold price flatlines as traders look to US PCE Price Index for some meaningful impetus

Gold price lacks any firm intraday direction and is influenced by a combination of diverging forces. The weaker US GDP print and a rise in US inflation benefit the metal amid subdued USD demand. Hawkish Fed expectations cap the upside as traders await the release of the US PCE Price Index.

Sei Price Prediction: SEI is in the zone of interest after a 10% leap

Sei price has been in recovery mode for almost ten days now, following a fall of almost 65% beginning in mid-March. While the SEI bulls continue to show strength, the uptrend could prove premature as massive bearish sentiment hovers above the altcoin’s price.

US economy: Slower growth with stronger inflation

The US Dollar strengthened, and stocks fell after statistical data from the US. The focus was on the preliminary estimate of GDP for the first quarter. Annualised quarterly growth came in at just 1.6%, down from the 2.5% and 3.4% previously forecast.