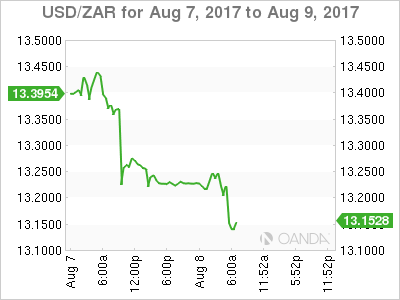

South African Rand Higher on Expectations Zuma is Removed

Capital markets appear to be in a holding pattern, with investors seeking an incentive amid the summer slowdown.

The focal point of this week looks set to be Friday’s U.S inflation data (CPI 08:30 am EDT), which could be key to the interest-rate outlook for the U.S.

Note: Two Fed officials (Kashkari and Bullard) indicated yesterday “soft U.S inflation remains a problem,” but played down the risk of market disruption when the Fed begins shrinking its balance sheet.

Last week’s stellar U.S jobs report is encouraging a number of renewed bets that U.S reflation is back in vogue.

Despite the odds for further tightening by the Fed remaining under +50%, dollar ‘bulls’ continue to search for evidence from Fed speakers this week to the contrary.

1. Stocks mixed results

Yesterday, the Dow posted an all-time high for the ninth consecutive session, touching 22,121, before closing slightly lower.

In Japan overnight, the Nikkei share average slid -0.3% as a stronger yen (¥110.55) hurt exporters, offsetting gains in the steel sector based on a solid earnings outlook. The broader Topix shed -0.2%.

In Hong Kong, shares rallied as strong company earnings and surging prices for steel and other building materials convinced the market that China’s economy remains solid despite weaker-than-expected trade data.The Hang Seng index ended up +0.6%, while the China Enterprises Index gained +0.2%.

Note: Trade data showed that China’s import and export growth slowed more than expected in July – ¥321.2B vs. ¥297.4Be; exports y/y: +11.2% vs. +15.2%e, imports y/y: +14.7% vs. +22.6%e

In China, stocks edged slightly higher overnight in quiet trading as investors shrugged off the disappointing trade data. The blue-chip CSI300 index rose +0.2%, while the Shanghai Composite Index gained +0.1%.

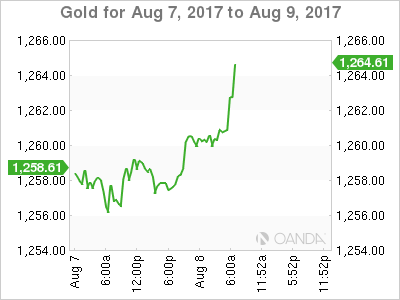

In Europe, equities opened down, but have since turned around with support from commodities (gold and oil). It seems macro data is having little impact on direction, as too is risk sentiment.

U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx50 flat at 3,503, FTSE -0.2% at 7,520, DAX -0.1% at 12,250, CAC-40 flat at 5,206, IBEX-35 +0.1% at 10,690, FTSE MIB -0.1% at 22,011, SMI -0.1% at 9,146, S&P 500 Futures -0.1%.

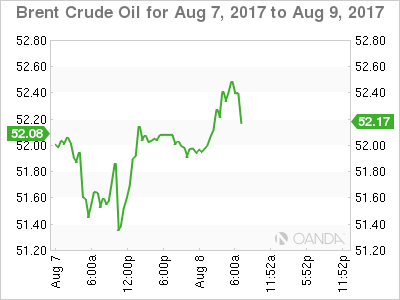

2. Oil prices steady as Saudi cuts next months supplies, gold higher

Oil prices steadied overnight on news of lower crude supplies from Saudi Arabia offset higher production from other large exporters.

The Saudi’s are expected to cut allocations worldwide in September by at least -520k bpd – inline with OPEC’s previous pledge to boost oil prices.

However, despite their pledge, global oil production remains relatively high.

Benchmark Brent crude is up +5c at +$52.42 a barrel, while U.S light crude (WTI) is +10c cents higher at +$49.49.

Crude bulls cite a stabilizing U.S rig count, falling domestic inventories and the Saudi cut in exports as support, while the ‘bears’ are leaning on robust production growth from the U.S, Libya and Nigeria.

Note: Production from Libya’s Sharara field is returning to normal after a disruption caused by protesters.

OPEC output hit a 2017-high in July and its exports were at record levels.

Officials from a joint OPEC and non-OPEC technical committee are meeting in Abu Dhabi today to discuss ways to increase compliance with the deal to cut -1.8m bpd in production.

Gold prices (+0.2% at +$1,259.41 per ounce) have edged up overnight as the ‘big’ dollar eased slightly, with the market waiting for Friday’s U.S inflation numbers for hints on the pace of monetary tightening by the Fed.

3. Yields mixed results

German 10-year Bund yields (-1 bps to +0.46%) continue to trade atop of their one-month low yield, supported by expectations that any withdrawal of ECB stimulus will be gradual. This view is supported by yesterday’s data showing industrial output in the eurozone’s biggest economy unexpectedly fell -1.1% in June m/m.

In Japan, JGB’s prices were mostly steady overnight after an auction of 30-year debt proceeded smoothly and drew ample investor demand. The two-year yield was flat at -0.11% and the 10-year yield inched down to +0.07%. The 30-year yield was flat at -0.875%.

Elsewhere, the yield on U.S 10-years has backed up less than +1 bps to +2.26%, while U.K Gilts are trading at +1.14%.

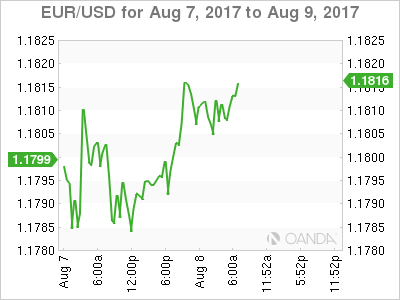

4. Dollar little changed in slow trading

The USD is trying to hold on to its small gains registered after last week’s stellar payrolls report. However, this task is becoming more difficult with the markets pricing in less than a +50% chance that the Fed will hike overnight rates at least one more time this year.

Current price action remains somewhat non-committal as market participants look ahead to Friday’s U.S CPI data for more guidance on rates. The EUR/USD (€1.1810) is steady and holding above the psychological €1.18 handle despite some disappoint data out of Germany (see below).

South Africa’s secret ‘no confidence vote’ against President Zuma is expected to keep ZAR ($13.1482) volatility high. Yesterday, ZAR firmed over +1.5% after the Parliamentary speaker announced the secret ballot. Dealers believe that if the vote does oust President Zuma (he has survived six previous no-confidence votes), then the ZAR could be pushed significantly higher in the short-term. If the ‘no-confidence’ fails, expect the rand to come under renewed pressure.

To remove Zuma from office, the opposition needs 201 votes and at least 50 parliament members of the governing party need to vote against him.

5. German exports and imports slump in June

Data this morning showed that German exports fell more than expected in June and imports sank even more sharply, widening the trade surplus in Europe’s biggest economy.

Seasonally adjusted, exports dropped by -2.8%, the sharpest fall in 24-months that ended five consecutive months of growth.

German imports were down -4.5%, the biggest drop since January 2009.

Note: Both headline figures confounded expectations that had pointed to exports edging down -0.3% and imports rising by +0.2%.

Author

Dean Popplewell

MarketPulse