Romania Monthly Focus: Master Manole’s legend

For those who don't know it, the legend of master Manole recounts the story of the building of Curtea de Arges Monastery, one of the architectural gems of Romania. The story goes that 10 master builders were hired to build the monastery, but their endeavours were fruitless, as whatever they were building during the day, collapsed during the night, up until their leader, Manole had a premonitory dream. The dream suggested that the building will only progress if a sacrifice was to be made by bricking in alive the first maid that was to set foot on the constructions site. To Manole's misfortunate, that first lady was none other than his wife, whom he tragically chose to sacrifice for the sake of completing the masterpiece that was to be dedicated to God. Tragic and cruel a story as it may be by today's standards, I believe there is something we can learn from it even in today's secular world, namely that you cannot aspire to build anything that would last unless you put (in our case not literally) at least a little heart into it. Why would this be important for Romania today? In my view not because we need inspiration to finish long lasting construction works of churches, highways and hospitals. In reality I believe we do not care so much about brick and mortar anymore, but we should care about building some lasting foundations for the institutions that define our democracy and our market economy.

Of course, one can argue that we already can display a wide array of such characteristic institutions, as we have a complex and supposedly independent judicial system, we have separate executive and legislative powers, we have competition council, central bank, consumer protection agency, financial supervisory authority, this is just to name a few. We however also have a legacy of what a 19th century great Romanian thinker called "form without a substance". Our institutions' organization has often been plagued by nepotism, as well as the so called Hubris of power syndrome2, whereby people assigned to manage these institutions have fallen prey to the belief that those institutions are theirs alone to run and dispose of at their whims and arbitrary wishes, as if we were talking about some property bestowed upon war lords in the Middle Ages.

As a matter of fact, the sort of tension between, on the one hand, the desire for modernisation and emulation of the European elite nations and on the other hand, the traditionalistic and conservative, master-servant type of worldview have been well documented for Romania, particularly since the 19th century. Romania's accelerated accession into the European Union, which came with a swift implementation of the „ acquis communautaire" and a forced adaptation to the EU's way of working have probably reinforced such tensions. To some extent, people still feel somewhat estranged from the EU, with large part of European regulations having been implemented formally without however internalising their necessity and meaning. The current European Parliament elections pre-campaign themes are a case in point: most of them relate to purely domestic politics or to how we imagine ourselves to relate to the other Europeans, while extremely little ink has been splashed over subjects related to how we want and how we can influence the ways of the European Union. As a side effect of such estranged feeling towards the EU, modern institutions seem often times as if they were devoid of substance, whereas we tend to attribute much more content to their leaders' views than what they are in reality entrusted and capable to deliver. As we all know, a face we can learn to like or dislike and we very rarely end up being indifferent to it, which cannot be said about abstract institutions, even if their logos are successfully branded or not. The problem with such personification of institutions is that in Romania, over the last 30 years, there was rarely a leader who could be perceived as NOT having betrayed the trust that people invested in him/her. Such people are naturally not superheros, although we tend to imagine them as such and when we discover the truth, we tend to become collectively depressed.

And yet the legend of Master Manole provides us a way out of this conundrum. If our institutions' authority cannot be built top down, perhaps we can try a bottom-up approach, The secret is the soul that is buried in the walls of the monastery, i.e. in the laws, bylaws and internal regulations of these institutions. Yes, dear readers,professional ethics is the name of that maid and with it I believe we can go far! The 10 years that have passed since joining the EU, on top of the almost 20 years' worth of pre-accession transition period should have been enough time for a sufficiently large class of professionals to be formed, educated and become of age and experience and for their loyalty to public service to be forged even if their leaders attitude were failing to support the cause. In the area of financial markets I have met many of such people and I am sure that they exist also in other areas. But for the financial markets and for its institutions things are bit more delicate because, on the one hand, the stakes are measured in real money and on the other hand, because perceptions play a large role, as investments are decided often times by people who have never set a foot in our country. For example, the perceptions about the credibility and the professionalism of the Finance Ministry officials can sometimes make the difference between a low and a high financing cost of the sovereign itself. Further on, the perception about the central bank's independence and its capacity to fulfil its price stability objective can make the difference between a stable and weakening currency or between steady interest rates and rising rates that can burden economic growth. Perception about a country's capital market transparency and efficiency can also make or break investments in the local equities.

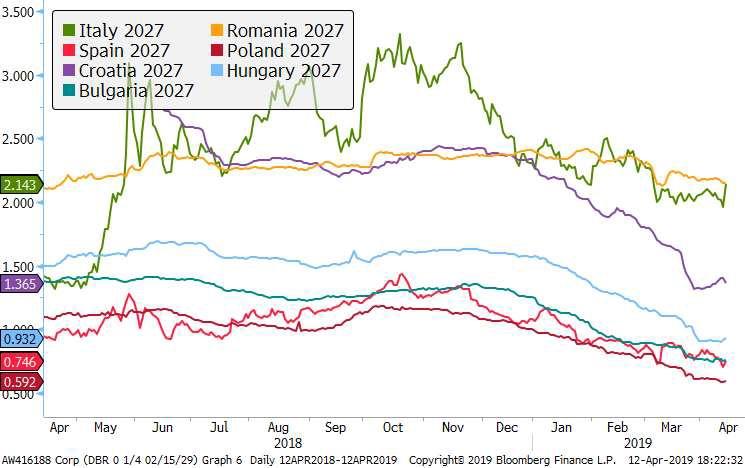

Such considerations may feel almost superfluous to many of you, but currently feel the urge to stress them nonetheless for three reasons. Reason no.1 is that the fundamentals of the Romanian economy indicate a fast increasing vulnerability, at least in comparison with other EU peers. Based on the latest Eurostat data, we have the highest inflation rate in the Union, by far the largest current account deficit and the second largest budget deficit. Such vulnerabilities are making foreign investors increasingly prudent when approaching Romanian assets, which is often reflected in higher risk premia being requested for investing in our assets (see for instance Graph 1).

Graph 1: Yields of 2027 maturities of selected European countries' EUR denominated Eurobonds: Romania among the highest, at least in the Investment Grade space

Source: Bloomberg

The second reason is that the external context, which in the last 2 years was rather on the favourable side, has been giving as of late signals of increased volatility and more troubled economic outlook. A case in point is the rollercoaster of risky asset prices from the last two quarters, with Q4 of 2018 having shown a severe correction related to US recession fears on the back of suspected excessive monetary tightening and on the back of escalating US-China trade tensions, whereas Q1 of 2019 has shown a swift comeback as the Fed and the ECB stepped back into easing mode, while bets have increased for a US-China truce. Of high relevance is also the emerging slowdown of the global economy, which translated into slower Eurozone growth will also limit the growth prospects of the Romanian economy. As a matter of consequence, the above mentioned vulnerabilities will be even more highlighted by such economic slowdown, not to mention other more severe negative economic shocks.

Reason no.3 is that in the public arena there have been a number of hasty statements and accusations aired recently, which can dent the image of key institutions for the financial markets. By coincidence or not, such institutions, such as the National Bank of Romania and the Fiscal Council, will have their Boards elected later this year. Based on the above mentioned financial stakes for the entire society, one would expect however that such an important selection process will be based on candidates' reputation, experience and competence, rather than being influenced by personal disputes.

Despite such hopes, given that we are early on in a very heavy election calendar, we shouldn't expect that the tone of arguments and the level of hostility will quiet down. In that context, when the bosses will be busy running their electoral tournaments, the heavy lifting will be on the army of masters Manole, many of which have dedicated their youths, their careers and their aspirations to the institutions which they are serving. Debates about economic changes will for sure be flying in pre-elections times and they can even lead to concrete actions with even heavy impact, as shown by the example of EGO 114. The role of professionals in this setup is to bring real content to the debates and through that content to „guard" their institutions from attacks which can weaken their founding principles. At the same time, though, public sector masters, as well as ourselves in the private sector, we should be aware that locking our gates to any criticism, as well as burying the content in loads of jargon, legislation and paperwork will not get us far, just like Manole's master builders were not getting far with building a soulless church. That is why it is our duty to search that soul hidden in the foundations of the institutions, to highlight it and if necessary to rejuvenate it. As a concrete example related to the recent EGO 114 saga, my hope is that its aftermath will bring further contentful debates as to finding the best solutions to achieve a lasting increase of financial intermediation and of real economy financing, but one which will be also compatible with the interests of the depositors, which at the end of the day are the ones financing most of the economy's borrowings.

Author

Erste Bank Research Team

Erste Bank

At Erste Group we greatly value transparency. Our Investor Relations team strives to provide comprehensive information with frequent updates to ensure that the details on these pages are always current.