Risk appetite is in serious jeopardy

Outlook:

Today we get the US ISM manufacturing index and construction spending, with ADP employment on Wednesday, jobless claims on Thursday and the monthly jobs report on Friday. There is a lot of other data, too, but these are likely the market-movers. Outside the US, the Reserve Bak of Australia meets tonight, the Bank of Canada meets on Wednesday (with new Gov Tiff Macklem), and the ECB on Thursday. The ECB is the only one expected to do anything, probably expand bond buys.

Not a mover is the Atlanta Fed GDPNow model, which gets revised again today after delivering a horrific forecast of a 51.2% contraction in Q2 on Friday. That’s seasonally adjusted and annualized, but a terrible number. A few days earlier the forecast was -40.4%, so a big increase in a short time, attributed to the personal income and spending data. That led the Atlanta Fed to expect Q2 real personal consumption expenditures growth to fall from -43.3% to -56.5%. Eeek. Meanwhile, exports’ contribution to GDP remains negative.

Risk appetite is in serious jeopardy. The cold war between the US and China can only heat up, not only because China can’t lose face by pulling back on Hong Kong but because Trump believes it’s in his political self-interest (aka re-election) to escalate. Markets have Trump’s number by now, but expecting negative outcomes doesn’t always weaken their effect when they are realized. The weekend talking heads, including the last governor of Hong Kong Patten, were strong on feeling but short on workable responses. The net seems to be that everyone should band together, including the UK and US, to lean on China to fulfill its treaty obligations. At a guess, not feasible, not least because Trump doesn’t “band together” with anyone.

Then there is a certain holding of breath to see how unlocking the economy is going to turn out. Some jobs have been recovered as cities and states re-open, but unsafe shenanigans at places like Lake of the Ozarks and Florida beaches imply a new surge of coronavirus cases starting late this week and into next week. Las Vegas is re-opening casinos on Thursday, so count forward 10-14 days from there in expectation of a new surge in cases.

Adding to the risk aversion pile of woes is the protest in the US against white cops killing black people. We have been getting this issue since 1619. Foreigners don’t know how to judge it as a market event, and while American traders are likely to shrug it off, there is a big unknown in there—who, exactly, are the outsiders taking advantage of authentic protest to make a race war? Conspiracy theories are already exploding all over the place. If we apply the cui bono principle, the most likely suspects are white nationalists, a disgusting thought.

So we have four big reasons for the stock market to pull back and the dollar to gain as a safe haven, even as it’s the source of the anxiety.

Let’s add a fifth—negative interest rates. In the UK, the BoE waffles back and forth on whether it can or should go for it. Lengthy editorials abound. After plowing through a ton of this bumpf, it’s hard not to deduce that an air if experimentation might reside in London. Negative rates have not helped the BoJ or ECB, or not by much, but as long as other measures are calibrated to avoid driving banks into the red, negative rates send a powerful anti-deflation message. Something else coming up hard on the agenda is permanent bonds (“consols”) that have to principal repayment, just interest payments, forever.

We are in the same position as last week and the weeks before—risk aversion “should” be on the rise given the awful developments in world economies, but stock markets keep going up, regardless of valuations or any other sane factors. It seems to be because stock markets are the only game in town. If this persists, the commodity currencies can thrive, along with the emerging markets, while traders dump their big long dollar positions in favor of the euro. Even Brexit looming over the pound can be ignored. This is, of course, nuts. But the end is not in sight (until it jumps up and bites off our noses).

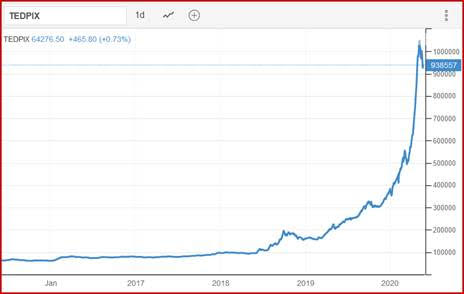

Tidbit: As in the US, in Iran people are buying stocks because there are no alternatives. Because of sanctions, they can’t invest abroad, and the rial is facing persistent devaluation from 30% inflation. The Economist says the wealthier can buy land or cars, but for the rest, the stock market (whose index is named Tedpix) is the only place to stash savings. The government pretends it’s a good thing (and is starting to offer its own ETFs). We’d bet there is plenty of gold being hoarded, too. See the chart from TradingEconomics.com. Look familiar?

Tidbit 2: The FT reports a Citibank investment bank division manager is downbeat: “We definitely feel that the markets are way ahead of reality. We really are telling every client to tap the market if they can because we think the pricing now couldn’t get any better. As the second quarter comes along and we start seeing the pain, and the collateral effects of that, we think this is going to be much tougher than it looks. Markets are pricing a V [shaped recovery], everyone’s coming back to work, and this is going to be fine. I don’t think it’s going to be that easy quite frankly.” A key worry is activist investors jumping in to push cost-cutting and other measures at the wrong time.

JP Morgan is pulling back from a deeply bullish outlook while Goldman Sachs is pulling back from its deeply negative one, according to Bloomberg.

Tidbit 3: Want to know why it took so long for the Minneapolis cop to get arrested for killing a black man? It’s more complicated than you think. Also more stupid. Reuters has a long story on the Supreme Court reasoning that has led so many cops to get off scot free after obvious misconduct. It’s something called “qualified immunity” and it rests on the concept that police are held accountable only if they violate rights clearly established in existing case law. Not the Constitution, case law. As the years roll on, fewer cases are heard from the abused, let alone decided in their favor. Therefore the case law already favors the murderous cops and anyone wanting to prosecute them has to tap-dance really skillfully. It’s a disgrace.

In the Minneapolis case, prosecutors have to prove the cop acted with a “depraved mind without regard for human life.” And the video is insufficient for reasons only the legal nit-pickers can understand. The fed’s separate case on violation of civil rights (4th Amendment or civil rights, take your pick) can take years. Don’t expect the ruckus to die down before the election.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat